Podcast

Contrarian Investor Premium

Hosted by Contrarian Investor Media · EN

The daily podcast discusses the major market activity and economic data release schedule for the day ahead, with a contrarian bent. Also includes regular podcast episodes a day (or more) early and without ads or announcements.

contrarianpod.substack.com

contrarianpod.substack.com

20episodes

Episodes

Newest firstAll episodes

Earnings Speak to Economic Strength

Aug 600:17:21Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events likely to move markets. It is Wednesday, Aug. 6, 2025. Today’s Stocks On The Contrarian Radar©️ segment features ICHR and starts at the bottom of this page. Read how the Contrarian Investment Portfolio produced a positive return for the third straight month and how it is being positioned.State of PlayAfter a tumultuous last week, the first couple of trading days of this week have been relatively quiet. Last night saw disappointing earnings from AMD and SMCI but this morning’s results were more positive. As we eye or board of indicators for signs of direction at 0830 ET, a little bit of ‘risk on’ is emerging:* Stock index futures are up a bit. Nasdaq and S&P 500 +0.3% each;* Commodities are rebounding: * WTI crude oil +1.5% to trade around $66/barrel* Copper +0.7%* Gold and silver -0.5% each* Bonds are seeing a little bit of selling, consistent with ‘risk on’ as the 10-year yield is +3 basis points to 4.23% (yields move inversely to prices);* Cryptos are not going along with this, or not yet. Bitcoin -0.5% to trade around $114,200.Today’s Known EventsIt’s all about earnings. Already reporting this morning were:* Uber (UBER ) beat estimates and announced a share buyback but doesn’t appear to have impressed investors as the stock is down a bit in the pre-market;* Shopify (SHOP ) beat analyst estimates and that report is being treated much more enthusiastically as the stock is +16% this morning;* Oscar Health (OSCR ), briefly a meme stock, reported disappointing results and the stock is down by ~2%;* Disney (DIS ) results were mixed and the stock is dropping a bit;* McDonald’s (MCD ) beat estimates and is rising (+3%).After the close at 1600 we’ll hear from:* AppLovin (APP ), probably a pretty good reflection of the tech industry and also the gig economy;* Airbnb (ABNB ), a solid indicator of the travel sector;* DoorDash (DASH ), always a good gauge of discretionary spending (if people are willing to pay ridiculous fees to indulge their own laziness…)* Lyft (LYFT ), which according to the reaction to Uber earnings has quite a high bar…The Bottom LineEarnings this morning were mostly positive. Shopify was particularly encouraging as this speaks to continued growth from small retailers, which reflects positively on the economy. The fact that AI applications are helping its bottom line (or at least its outlook) is even better. We’ve said for some time that AI spending can lift many boats. If it is actually producing results then that’s even better. This should offset the earnings miss from AMD, but it’s worth pointing out that AMD actually raised guidance.Crucially, from a big-picture perspective there was nothing in this latest round of earnings that speak to weakness in the economy: McDonald’s is opening restaurants, Disney theme parks are booked solid, and even the New York Times (NYT ) is growing subscriptions revenue.Sure, there is the tariff overhang and ample unpredictability from the White House. Those were a major concern last week. Now, not so much. Just like you were reminded, these fears often fade away as quickly as they surface.Stocks On The Contrarian Radar©️The Contrarian has maintained a list, going back more than a year, of ‘undiscovered’ AI chip stocks. The ‘undiscovered’ in ‘air quotes’ because these are, of course, not really undiscovered at all — they just haven’t attracted much (or any) of the hype associated with the Nvidias of the world.Yesterday’s trading session saw the dramatic drop of one of these names, Ichor Holdings (ICHR ), which manufactures fluid delivery subsystems for the semiconductor industry. This sounds like a crucial part of the whole semiconductor supply chain even if it does not make ICHR a chip manufacturer itself. Well, the stock fell by 30% yesterday after reporting earnings that disappointed investors on a number of fronts.At issue was not so much earnings. EPS did fall short of analyst estimates but revenues surpassed what was anticipated. That’s not what caused the drop. The concerns were elsewhere:* Margins and revenue guidance came in at the lower end of expectations* The company is experiencing hiring pressures, limiting its ability to expand margins* Management’s tone on the call was at times quite conservative. The dreaded ‘plateauing’ phrase was used, referring to its crucial advanced packaging business* Finally, executive leadership is in transition with the company actively searching for a new CEOAdd it all up and investors took the opportunity to punish the stock, sending it to its lowest level in almost a decade:It’s interesting to hold this thing up against Nvidia (NVDA ), which is very much the bellwether for the AI chip industry. As you can see there has been a clear divergence since April:Shouldn’t ICHR track NVDA over time and therefore wouldn’t it revert to this pattern at some point, hopefully soon?That aside, the kind of selloff we witnessed yesterday is the type of thing that gets The Contrarian to take notice. It leaves ICHR trading at a compelling 0.9x forward sales, which is almost unheard of for a technology company especially one servicing the AI chip sector. The balance sheet appears healthy, with $92 million of cash versus total debt of $126m.There is undoubtedly some uncertainty facing this company. GAAP earnings-per-share was negative last quarter. Margin pressures are real. The customer base is concentrated with three OEMs — Applied Materials, Lam Research, and ASML Holding — making up 73% of sales. The leadership transition is also a very real concern.The OpportunityStill, one can’t help but think that this was a classic — and violent — overreaction. One figures ICHR’s products are crucial to semiconductor manufacturing and demand for semiconductors — as we have seen from tech earnings — is not going anywhere but up. The company’s issues are in large part due to not being able to keep up with this demand. That is not a bad problem to have.The turnaround may take some time. There’s no guarantee it will even happen. The notoriously cyclical semiconductor industry could turn before management is able to get its ducks in a row. These are all risks. But with risks come opportunity.The VerdictFor these reasons The Contrarian took a tiny starter position in ICHR yesterday, buying in at $14.25. He will look to add to this if it drops more.Housekeeping* PSA: The scheduling of this briefing is being reshuffled a bit due to the success of the live video. * This will air closer to the market open, typically between 0800 and 0900 ET. * Free subscribers can join live. The recording will be available to premium subscribers. * You should receive this briefing in your email and on the app — also Spotify — as previous. There are some reports that this is not happening consistently. Substack has been notified of this.* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks the portfolio’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →

Trump Policies Weigh on Markets, Again

Aug 400:15:41Tap to summarizeWelcome to the Daily Contrarian, our morning evening look at events likely to move markets. It is Sunday, Aug. 3 and we are posting this unprecedented early briefing due to your host’s travel schedule.Hot off the press: Read how the Contrarian Investment Portfolio produced a positive return for the third straight month and how (and why) it is being positioned a bit more defensively...State of PlayStocks dropped precipitously on Friday, capping a volatile week and starting the month off on a sudden risk-averse setting. New tariffs were to blame along with President Trump firing the Bureau of Labor Statistics commissioner, apparently for rigging non-farm payrolls.As we eye or board of indicators for signs of direction at 2015 ET:* Cryptos are moving higher, shrugging off reports that China is (again) banning digital currencies. Bitcoin +1%. Ethereum +3%. XRP +6%* Stock index futures are not moving at all. S&P, Nasdaq, and Russell are all hogging the break-even point;* Not much to report in commodities land yet either. WTI crude oil is down 0.5% to trade around $67/barrel. No movement elsewhere;* Bonds are seeing a few bids at the short end of the curve. The 2-year yield, the most sensitive to Fed interest rates, is down 4 basis points to 3.68% (yields move inversely to prices).Today’s briefing is free. To receive this briefings regularly, subscribe here:Known EventsEarnings are the main story of the week, ex-tariffs and anything else that comes out of the White House of course.First up tomorrow morning:* Furniture supplier Wayfair (W ) * Tyson Foods (TSN ), a substantial portfolio holding* Semiconductor manufacturer onsemi (ON ) After the close at 1600 we will hear from:* Palantir Technologies (PLTR )* Hims & Hers Health (HIMS )* MercadoLibre (MELI ) Other highlights this week include AMD (AMD ) on Tuesday, Shopify (SHOP ) on Wednesday, and D-Wave Quantum (QBTS ) on Thursday. * We’ll also get a look into the US travel sector with Marriott (MAR ), Wynn (WYNN ), Hilton (H ), and TripAdvisor (TRIP ). * Uber (UBER ) and Lyft (LYFT ) report Wednesday* Fast-food chains McDonald’s (MCD ), Burger King owner QSR (QSR ) and Wendy’s (WEN ) are scattered through the weekSo much for the look ahead. These events might move markets a bit but investors’ concerns now are clearly elsewhere…The Bottom LineWe got a stark reminder last week that President Trump can still upend the prevailing mood on Wall Street. Some of the tariff announcements, like the 30% levy on Switzerland, seemed to come completely out of left field. Investors by now are used to some unpredictability from the White House when it comes to tariffs, but not when the moves are this nonsensical.Then there was the jobs report. As discussed Friday, the headline numbers were not terrible but along with downward revisions to previous months bad enough to increase the likelihood of interest rate cuts. That “happy medium” would normally be a good thing. Except then the reaction from the White House was anything but normal. According to the Wall Street Journal editorial board, the move to fire the BLS head means “Trump seems to understand that the jobs report signals trouble.” That may not even be true. It may be more due to Trump’s impetuous nature than real concerns about the labor market. But it doesn’t matter because the impression that Trump and the White House are suddenly concerned about the labor market — rather than crowing about its achievements — is now absolutely real. Judging by Friday’s market activity, it’s not just the WSJ editorial board drawing this conclusion.Silver Lining?One thing we’ve learned about Trump is he can reverse course on crazier policies as quickly as he decides on them — especially if the market sends him a clear signal that it doesn’t like the policy. According to that pattern, we may be a day or two (tops) away from saner messaging from the White House.The fact that previous months of non-farm data was revised lower (and that quite dramatically) does speak to a slowing labor market. This has yet to affect jobless claims however as these have actually been dropping in recent weeks. Job openings are mostly holding up, according to the latest JOLTS report.Retail sales data continues to show growth despite higher prices. And let’s not forget that earnings have been pretty stellar across the board — including cruise line companies that capture discretionary spending by middle class consumers. None of the ‘big three’ public cruise lines — RCL , CCL , NCLH — lowered guidance in their latest quarterly earnings.In ConclusionThere are indications that hiring is slowing, but there is also data to support continued growth in the labor market, Importantly, there is little indication that layoffs are increasing.Countering that is strong retail data and healthy outlook for discretionary spending, judging by what the cruise lines have been telling us at least.Finally, perhaps as a tie-breaker, we point you to the M&A market. Corporate dealmaking is suddenly quite hot. That actually says a lot about two very important risk metrics: corporate risk appetite and capital markets. The first speaks to the underlying demand for expansion and investment. The second to the financing that makes the whole thing possible. When both are healthy, as they are now, it is hard to see how public equity markets will remain down for very long. That, at least has been the pattern.It’s true that the underlying setup for markets just doesn’t feel very good right now. But we have seen — just a few months ago — how misguided these feelings can be. That’s not to say the whole thing will turn around right away. Indeed, we may need to see a little more selling before investors pile back in for the next leg of the bull market. Ultimately, however, the long-term picture remains constructive.Housekeeping* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks the portfolio’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →

Earnings, Fed, Payrolls: Massive Week Ahead

Jul 2800:12:34Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events likely to move markets. It is Monday, July 28, 2025. Today‘s Stocks On The Contrarian Radar©️segment features WHR and starts at the bottom of this page. State of PlayLast night saw the announcement of a trade deal between the US and Europe. That is not having much of an impact as we eye or board of indicators for signs of direction at 0745 ET:* Stock index futures are pointing a bit higher, led by tech. The Nasdaq is +0.4% with S&P 500 +0.2%;* Cryptos are gaining a bit of ground with Bitcoin +0.5% to trade around $118,700;* Commodities aren’t doing much. WTI crude oil is +1.3% to trade around $66/barrel. Copper is unchanged. Gold and silver also unchanged;* Bonds aren’t doing anything. The 10-year yields 4.40%.Known EventsIt’s a massive week of earnings, Fed, and economic data but most of that doesn’t come until later in the week. For today, there isn’t much going on. A couple of earnings after the close is about it:Waste Management (WM ), Whirlpool (WHR ) and Tilray (TLRY ) are the main names there. Tomorrow the earnings party gets started for real, with UnitedHealth (UNH ), SoFi (SOFI ), PayPal (PYPL ), Boeing (BA ), Spotify (SPOT ), UPS (UPS ), Procter & Gamble (PG ), Royal Caribbean (RCL ) and JetBlue (JBLU ) — and that’s all before the open!Other earnings highlights this week include Meta (META ) and Microsoft (MSFT ) after Wednesday’s close and Apple (AAPL ) and Amazon (AMZN ) on Thursday evening.The Fed concludes its interest rate meeting on Wednesday. The Fed is not expected to move its key policy rate from its 4.25-4.5% target. Friday brings non-farm payrolls. The Bottom LineThe trade deal with Europe is nice and should provide a boost to risk assets today. But upside may be limited just because of all the data we’re getting later in the week. Those figures will need to play along with the bullish mantra for this to be sustainable. Payrolls on Friday are obviously the big one but earnings and the Fed also have the potential to upend things.When it comes to the Fed, investors will be looking for indications that there will be interest rate cuts at the next meeting on Sept. 17. Right now Fed fund futures are pricing in a 60% chance of a cut. We’ll discuss the Fed more in Wednesday’s episode.Anything companies say in their earnings that speaks to slowing consumer spending in the US would surely also trip up all the good cheer. On that note…Stocks On The Contrarian Radar©️You may want to keep an eye on Whirlpool (WHR ) earnings this afternoon. This company makes not just jacuzzis but washers, dryers, kitchen appliances, and more. For many families, washers and dryers are the biggest purchase they will make outside of cars and houses. So what management says about the outlook for these big-ticket items is well worth paying attention to.Where WHR’s performance is concerned, that has been quite ugly. The stock has kind of gone nowhere in years, trailing the S&P 500 by substantial margins:Given the company’s products it is no surprise that it is treated — perhaps correctly —as a proxy for the housing market. This leaves it trading at compelling valuations:* 13x forward earnings* 0.8x EV/forward sales* 0.4x forward sales* 7x forward cash flowsEarnings excepted, those are pretty compelling multiples, all well below the median for the industry.Unfortunately, the balance sheet tells a very different story:* $8 billion in net debt versus a market cap of just $5.6 billion* Unsold inventory accounts for $2.4b of its $5.4b current assets. Offsetting that is $3.5b of accounts payable* Almost $6b of its $16b of total assets are goodwill and other intangibles versus $13.7b of total liabilities* Almost $5b of the total debt is long term, meaning it carries a higher interest rate.Ugly, dawg.The verdictSometimes things are cheap for a reason. WHR’s balance sheet should alarm any potential investor. This will explain — and fully justify — the stock’s depressed valuations. Sure, once interest rates move lower and the housing market recovers it will greatly help WHR’s fortunes. But when might that be? More importantly, the company needs to continue to service its debt in the interim. It is also sitting on (literally) billions of dollars of unsold inventory.WHR does have a sizable dividend of $7/share, corresponding to almost 7% at current prices. That should probably be cut, if not eliminated outright. It would cause the stock to drop more in the short term but would make it a lot more appealing. To management’s credit, long-term liabilities have dropped over the last year, from $6.7b to their current level of $4.8b. Maybe the ugliest days of the balance sheet are in the past. But a lot of work still needs to be done for this thing to be investable.Maybe if today’s earnings show continued improvement to the balance sheet and a sizable cut to the dividend payout the stock will become more appealing. But those prospects appear to be remote at this point…Housekeeping* PSA: The scheduling of this briefing is being reshuffled a bit due to the success of the live video. * This will air closer to the market open, typically between 0800 and 0900 ET. * Free subscribers can join live. The recording will be available to premium subscribers. * You should receive this briefing in your email and on the app — also Spotify — as previous. There are some reports that this is not happening consistently. Substack has been notified of this.* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks The Contrarian’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →

Google Earnings

Jul 2300:08:43Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events likely to move markets. It Wednesday, July 23, 2025.State of PlayPresident Trump announced a ‘massive’ trade deal with Japan last night. This caused stocks in Japan to rally as the Nikkei gained 3.5% on the day. As we eye or board of indicators for signs of direction at 0815, these are mostly positive:* Stock index futures are pointing to gains, led by small caps, usually a good sign. The Russell 2000 is up 0.9%. S&P 500 futures are 0.3% to the good. Nasdaq futures are flat. The Nasdaq actually dropped a bit yesterday;* Copper is rallying, up 1.6%, close to fresh record highs. WTI crude oil is down 0.6% to trade around $65/barrel;* Cryptos appear to be taking a bit of a breather. Bitcoin is down 0.5% to trade around $118,500;* Bonds are down a bit. The 10-year yield is up 3 basis points to 4.36% (yields move inversely to prices).Today’s Known EventsEarnings season is underway. We got some fresh reports already this morning:* AT&T (T ) beat earnings earnings estimates and appears to have raised guidance but something in the report didn’t please investors as the stock is dropping in the pre-market, down 3% at the time of this writing;* Hilton Worldwide (HLT ) also beat estimates but here too the stock is down -1.8%;* Thermo Fisher Scientific (TMO ) beat estimates and that stock is rising in the pre-market, +2.5%;* Hasbro (HAS ) trounced estimates and raised guidance and that stock is up 5%.Of course the big names report after the close at 1600 ET: Google (GOOG )/(GOOGL ) and Tesla (TSLA ). One economic data release to tell you about. Existing home sales are out at 1000. Economists who were surveyed expect 4.01 million sales, about the same as last month’s 4.03 million.Finally, a 20-year bond auction is at 1300. No analyst estimate but last one of these resulted in a yield of 4.942%.The Bottom LineTrade deals are nice but we aren’t really seeing much of a reaction from US stocks. Maybe that’s because most of the scuttle around Japan negotiations have been positive so the market figured this was coming. But then copper prices certainly speak of increased risk appetite ahead.The tech rally appears to be on pause, presumably until we get Google earnings tonight. While Google itself has actually been moving higher (+4% over the last week) what management says about AI spending in particular could be what is leading investors to sit on their hands a bit. It may also be simple profit taking from tech, which has been on quite a tear since the April lows (+33%).The Contrarian, who (full disclosure) is long Google, will be watching the company’s AI datacenter investments that are reported in the form of capital expenditures (the datacenter piece may not be broken out explicitly, but we all know that’s what most of the capex is). Presumably analysts will also be watching because is a direct correlation to AI chipmakers, and therefore most of the tech sector these days. The expectation is for $18 billion in capex, up a bit over the $17 billion reported last quarter. Beyond that we also have tariffs and trade-related news. The Aug. 1 deadline is still out there.Housekeeping* PSA: The scheduling of this briefing is being reshuffled a bit due to the success of the live video. * This will air closer to the market open, typically between 0800 and 0900 ET. * Free subscribers can join live. The recording will be available to premium subscribers. * You should receive this briefing in your email and on the app — also Spotify — as previous. There are some reports that this is not happening consistently. Substack has been notified of this.* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks The Contrarian’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →

Earnings Good, Tariff Rumblings Not

Jul 21, 202500:10:01Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events likely to move markets. It is Monday, July 21, 2025. Your host returns after a long illness-induced absence. Apologies for any inconveniences caused by this outage.State of PlayStocks find themselves at record highs after moving higher last week. As we eye or board of indicators for signs of direction at 0915 ET:* Stock index futures are unchanged with the exception of small caps, which are pointing higher. The Russell 2000 is up 0.5%;* Cryptos are not really doing much after rising to records last week. Bitcoin is unchanged, trading around $118,000;* Bonds are seeing some bids, interestingly enough. The 10-year yield is down 6 basis points to 4.37% (yields move inversely to prices);* All is quiet in commoditiesland. WTI crude oil is unchanged trading around $66/barrel. Copper is up 0.5%. Silver is on the move a bit, up 1%. Gold +0.5%.Known EventsIt’s a massive week for earnings with the heavy hitters checking in at midweek. Tesla (TSLA ) and Google (GOOG /GOOGL ) are probably the biggest names we’ll hear from this week, both after Wednesday’s close. So far today Domino’s Pizza (DPZ ), Verizon Communications (VZ ) and Ryanair (RYAAY ) all posted positive results. After the close the highlight is chipmaker NXP Semiconductors (NXPI ) The Bottom LineGood news from earnings so far, then. But again, the big names don’t report until midweek. We’ve still got tariffs hanging around, with the Aug. 1 deadline looming. Can expect to hear a lot more about that as the deadline approaches.Even ahead of that there are some rumblings that tariffs could be less benign than initially anticipated. Automaker Stellantis (STLA ), the subject of a contrarian take this March, is warning of tariff-induced losses. There was also a recent Wells Fargo report, that noted a decline in discretionary spending on services and the ‘false narrative’ that tariffs were having a benign impact. We’ve also got student loan bills increasing for some borrowers, though a lot of those reports are fear-mongering clickbait.Still: with stocks at record highs, this is not the environment for a Contrarian to allocate risk. Sure, there could be happy AI news from Google and chipmakers this week and Tesla could pull another rabbit out of its hat. But valuations are stretched and the rumblings under the surface are not a great sign.Housekeeping* PSA: The scheduling of this briefing is being reshuffled a bit due to the success of the live video. * This will air closer to the market open, typically between 0800 and 0900 ET. * Free subscribers can join live. The recording will be available to premium subscribers. * You should receive this briefing in your email and on the app — also Spotify — as previous. There are some reports that this is not happening consistently. Substack has been notified of this.* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks The Contrarian’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →

Fed Meeting Minutes, New Tariff Threats

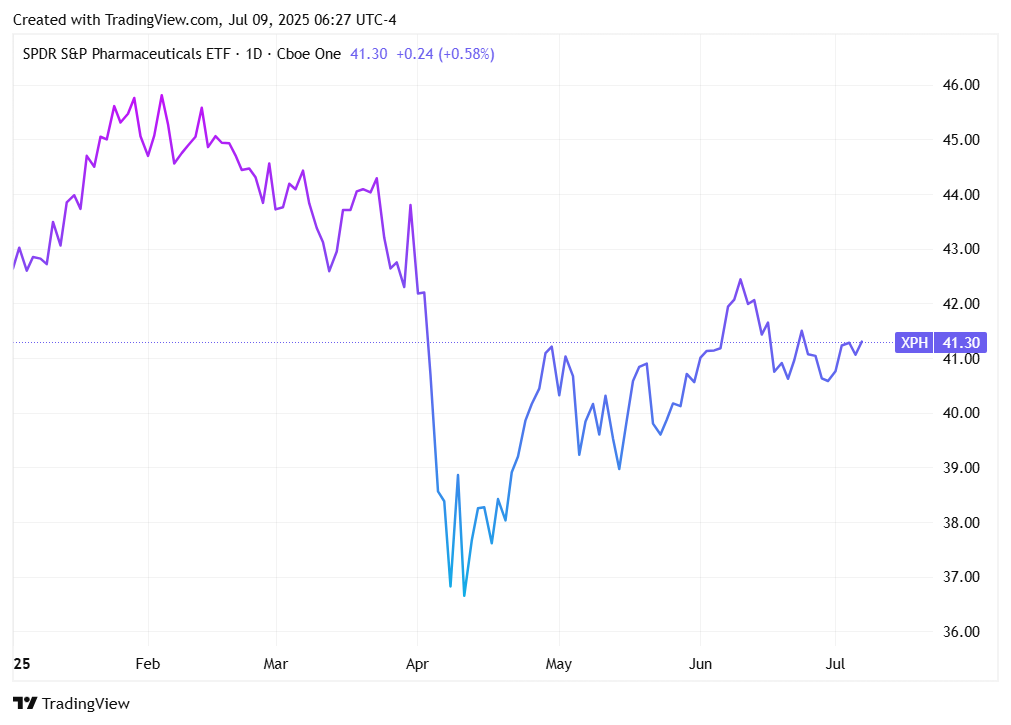

Jul 9, 202500:16:02Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events likely to move markets. It is Wednesday, July 9, 2025. Today’s Stocks On The Contrarian Radar©️ segment features pharmaceuticals, specifically MRK , and can be read at the bottom of this page.State of PlayStocks have meandered this week due to lack of catalysts, just as was anticipated. As we eye or board of indicators for signs of direction at 0715 ET things are pretty quiet:* Stock index futures are unchanged with no major US index moving more than 0.2% from the break-even point;* The big move in commodities is in copper, which is consolidating after jumping to record highs earlier. This was caused by, you guessed it, tariffs or the threat thereof as President Trump said he would slap a 50% import tariff on the industrial metal. WTI crude oil is unchanged at $68.50/barrel. Gold and silver not doing much either;* Cryptos aren’t moving much. Bitcoin unchanged trading around $108,80;* Bonds are flat. The 10-year yields 4.40%.Known EventsMinutes from the Federal Reserve’s last monetary policy meeting are out at 1400 ET. This is closely watched by investors even though it captures a moment in time from several weeks ago, in this case the June 17-18 meeting. The Fed held rates unchanged at that meeting but signaled there would be two rate cuts this year. The minutes will provide some insights into the discussions that were held. This isn’t binding because a) presumably meeting participants could just agree to stop transcribing at various points and b) the Fed is data dependent and new data can and will impact FOMC voting members’ views as it becomes available. Indeed there has been new data since that meeting already, in the form of the PCE Deflator and non-farm payrolls, among others. This is one reason The Contrarian doesn’t understand all the fuss around FOMC meeting minutes, but the market does move on this.Tomorrow (Thursday) morning, second-quarter earnings season kicks off with traditional curtain-raiser Delta Air Lines (DAL ). Conagra Brands (CAG ) reports at that time as well. After the close we’ll get Levi Strauss (LEVI ) and WD-40 (WDFC ), among others. The Bottom LineAny Fed talk of inflation concerns in the minutes could put a damper on risk-taking as it will indicate higher-for-longer interest rates. If the discussions are more concrete around rate cuts, it should lead to a market rally. You’re going to want to watch Fed fund futures, currently pricing in just a 4% chance of a rate cut at the next meeting, on July 30. A rate cut at that meeting is off the table in all likelihood but futures are pricing in a 60% likelihood of a cut at the subsequent meeting, which isn’t until Sept. 17.Fed-obsessing watching aside, the focus will otherwise be on tariffs. It’s not just copper that was caught in Trump’s latest comments on this matter but also pharmaceuticals…Stocks On The Contrarian Radar©️Trump’s comments have led to a drop in pharma stocks overnight, as evidenced by the SPDR S&P Pharmaceuticals ETF (XPH ), which is down 2% at the time of this writing. This drops the XPH to ~$40.50/share:That latest move is not captured in the above chart, which doesn’t reflect pre-market activity. It moves the ETF toward the lower end of its five-year Bollinger Band range:Technically that makes XPH cheap but not yet a bargain as it was in the middle of last year, for example. So the move in pharma stocks is not particularly dramatic here. It seems the market is getting wise to Trump’s tariff threats, treating these more as bombast than a clear reason to dump risk.Perhaps more importantly, major pharma companies like Merck (MRK ), Johnson & Johnson (JNJ ), Eli Lilly (LLY ), and Novartis (NVS ) have already announced plans to expand US manufacturing as a direct result of previous tariff threats. All of these stocks factor prominently in XPH’s holdings.If you add Pfizer (PFE ), a Contrarian Portfolio holding, into this mix to create a ‘Big 5’ of pharma stocks, you can observe a mixed bag of performance over the last year: Merck, Eli Lilly, and Pfizer are the clear losers here with MRK having lost more than a third of its value! This leaves MRK trading at prices not seen since 2022 and at just 10x forward earnings versus an industry average of 17x. On a cashflow basis, MRK is even cheaper, trading at 8x forward cashflows versus an industry average of 14x.Does this make Merck a buying opportunity? Maybe, though other valuation metrics (price/sales notably) are much more in line with the industry average. The balance sheet appears to be in good shape with $35 billion of total debt versus a market cap of more than $200 billion. But here too more scrutiny is needed, as $36 billion of the company’s $115 billion assets are ‘goodwill’ and ‘other intangibles.’ Let’s also not forget that the balance sheet will take a hit from Merck’s $10 billion buyout of Verona Pharma (VRNA ), though that may be priced in already. What that deal does tell us is that M&A in the pharma industry is alive and well. That speaks to an industry very much in expansion mode.The VerdictSome pharma companies are cheap by historical standards and Merck may be the cheapest pharma major at present. That makes a potentially compelling investment opportunity. MRK also has a nice dividend, to the tune of 4% at current prices. That makes it a better candidate for tax-advantaged portfolios like IRAs than vanilla brokerage accounts (for US taxpayers at least).Pharmas are also compelling because they are mostly divorced from economic realities. The assumption is that individuals need certain drugs and insurance plans, whether provided by the state or private enterprise (or employers), will make these purchases on their behalf. That isn’t 100% true of course as people lose their jobs and insurance plans, for whatever reason, make the purchase of brand name treatments more expensive. Generic drugs of course can also replace the successful brand treatments. Some pharma majors have generics divisions. Merck, at least in the US, does not.The challenge with pharmaceuticals is gauging the valuation. Much of the stock price depends on the likelihood of success of future drugs more than anything else. That is not something The Contrarian, who barely passed ninth grade biology (when he took it in 10th grade), is educated to assess. He could read up on it, sure. Maybe some day he will. But as a major holder of Pfizer already he is loath to add another pharma major to his portfolio. At that point it really makes more sense to just buy the ETF.For these reasons The Contrarian is sitting this opportunity out, at least for now. Should MRK or pharma ETFs become a lot cheaper than he will need to revisit this stance however.Not investment advice. Do your own research. Make your own decisions.Housekeeping* PSA: The scheduling of this briefing is being reshuffled a bit due to the success of the live video. * This will air closer to the market open, typically between 0800 and 0900 ET. * Free subscribers can join live. The recording will be available to premium subscribers. * You should receive this briefing in your email and on the app — also Spotify — as previous. There are some reports that this is not happening consistently. Substack has been notified of this.* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks The Contrarian’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit <a href="https://contrarianpod.substack.com?utm_medium=podc...

Transcribe →

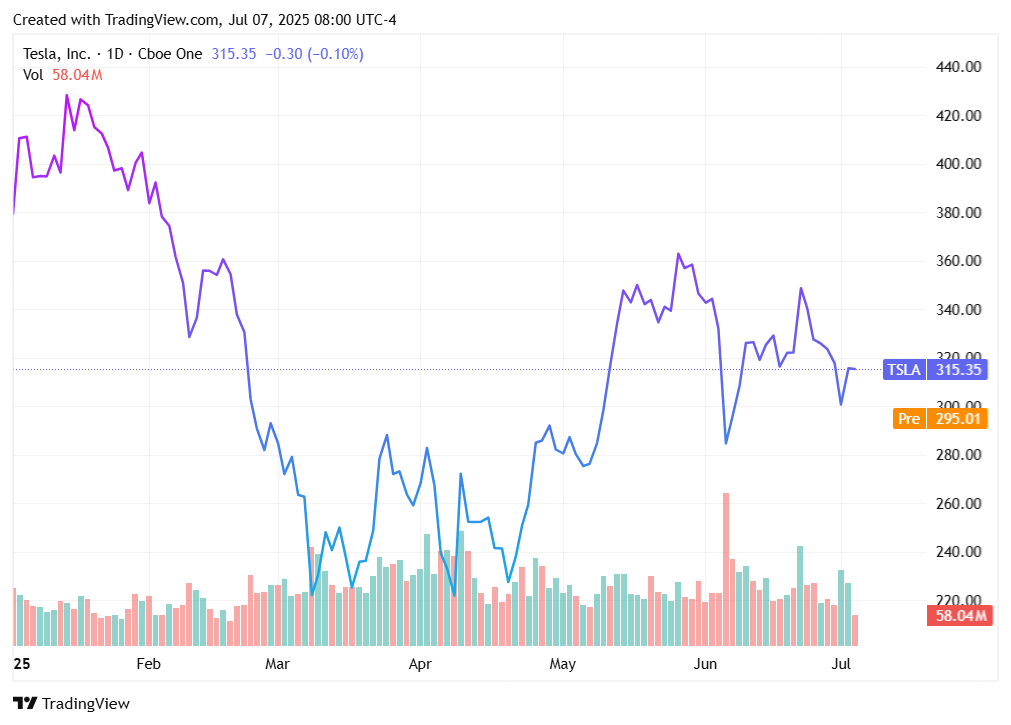

Tariff Concerns, Tesla Drops on Musk Political Aspirations

Jul 7, 202500:14:03Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events likely to move markets. It is Monday, July 7, 2025. Today’s Stock On The Contrarian Radar features Tesla (TSLA ) and can be read at the bottom of this page. State of PlayB, with President Trump threatening new tariffs on countries that side with policies by BRICS nations. That is weighing on things as we eye or board of indicators for signs of direction at 0830 ET:* Stock index futures are down but off of the lows. Small caps are seeing the worst of it with the Russell 2000 down 0.5%. S&P 500 and Nasdaq are down about 0.3% each;* Bonds are seeing a bit of selling as well. The 10-year yield is up 4 basis points to 4.36% (yields move inversely to prices);* Commodities are mixed. WTI crude oil is up 0.7% to trade around $67/barrel but copper is down 0.5%. Gold and silver are dropping as well, perhaps an indication the market isn’t taking this latest tariff stuff very seriously. Both are down 1-1.5%;* Cryptos are unchanged. Bitcoin is up 0.5% to trade around $108,600.Known EventsIt’s a pretty slow day. Make that a slow week. Nothing of note on the calendar today. Tomorrow brings consumer credit. Wednesday a 10-year note auction and FOMC minutes from the last meeting. Thursday a few earnings and a couple of Fed speakers. Friday the WASDE Report. So yeah, slow weekThe Bottom LineWith nothing else going on the focus will be on tariffs. So far this is mostly noise, as evidenced by futures though it is enough to chill some of the good cheer we got with non-farm payrolls on Thursday.This leaves us with a cautious start to the week. We may be in a holding pattern until FOMC meeting minutes on Wednesday, unless of course there is fresh tariff news to drop.On the topic of the Fed, investors don’t seem concerned with all the noise Trump is making about removing Jerome Powell and replacing him with somebody who will cut interest rates. The questions this raises about the Fed’s independence are obvious. Perhaps investors figure nothing will happen until Powell’s term expires next May and when it does the Fed will already be on a rate-cutting course. And that Trump will leave offices some 20 months after that. Either way, it’s not something that seems to factor into risk calculations very much.Stock On The Contrarian Radar©️Tesla (TSLA ) is down 6% in the pre-market at the time of this writing after Elon Musk, who has apparently never hear of Ross Perot, said he is launching a political party. Buying opportunity for Tesla? This morning’s move drops the stock below $300 again:As you can see, this is still a ways off of the lows of the year. TSLA is a crazy stock due to wild swings resulting from any number of factors. Ultimately the stock is priced for its potential in all things electric vehicles, self-driving cars, and more. For this reason it is the rare example where fundamentals really don’t apply. But other things do.A lot of these have to do with Elon Musk himself. Investors clearly want Musk to not only be part of Tesla, but make it his primary focus. If he is starting a political party that obviously means less time spent on Tesla. And that is why the stock is dropping so dramatically this morning.An interesting exercise is to hold TSLA up against the S&P 500 (SPY ): Over the last two years or so, Tesla has kind of tracked the SPY albeit with much more volatility. Worth noting the period in late 2024 when TSLA trounced the SPY, presumably due to Musk’s involvement with the Trump administration and the benefits this was believed to bring for the stock. If you remove that outlier, the traction is much more solid.In the past two years it has paid to buy TSLA when it dipped below the S&P’s return dating to the early 2023 start date. This was most recently in May. As the above chart indicates, TSLA is now close to the S&P but not close enough where it has (historically) presented a buying opportunity.The VerdictFor this reason The Contrarian is not buying this dip in Tesla though he is monitoring the situation closely. If TSLA dips to the $250/share range it may make sense for The Contrarian to buy a few shares.Full disclosure: The Contrarian has never owned TSLA outright though it is obviously included in several indexes he owns in retirement accounts.Not investment advice! Do your own research, make your own decisions.Housekeeping* PSA: The scheduling of this briefing is being reshuffled a bit due to the success of the live video. This will air closer to the market open, typically between 0800 and 0900 ET. Free subscribers can join live. The recording will be available to premium subscribers.* Read this month’s portfolio update letter here. The Substack chat tracks The Contrarian’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →

Non-Farm Payrolls Add Fuel to Market Rally

Jul 3, 202500:08:56Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events moving markets. It is Thursday, July 3. Jobs Day. Read this month’s update on the Contrarian Portfolio here.State of PlayNon-farm payrolls, which we’ve been waiting for all week, just came in better than anticipated. As we eye or board of indicators for signs of direction at 0845 ET, risk on is the story:* Stock index futures are moving higher after that jobs number, led by small caps (usually a good sign). The Russell 2000 is up 1%. S&P 500 and Nasdaq ~0.3% to the good;* Cryptos are moving higher. Bitcoin is up 2% to trade around $109,400;* Bonds are seeing a few bids. The 10-year yield is down 3 basis points to 4.26% (yields move inversely to prices);* Commodities are quiet after a broad rally yesterday. Nothing to report there.Today’s Known EventsNon-farm payrolls were obviously the big one. To go through the numbers:* 147,000 new jobs versus 111k anticipated and 144k previous (revised upward from 139k)* That drops the unemployment rate to 4.1% (4.3% anticipated/4.2% previous)* Private payrolls were a miss however, printing at 74k (105k/137k)* Average hourly earnings of 0.2% month-over-month (0.3%/0.4%)* Average hourly earnings of 3.7% year-over year (3.9%/3.8%)There are others worth keeping an eye on as well, however:* We just had initial jobless claims come in at 233 versus 240k anticipated and 236k last week. The four-week average is 245k.* US trade deficit was $71.5 billion ($69.9b/$61.6b)* At 0945 we’ll get the final June figures for PMIs, but these will likely just confirm what was in the flash report.* Factory orders are at 1000. The expectation here is for an increase of 8.1% MoM in MayThe Bottom LineHappy days are here again! The market is moving further into fresh record highs after this jobs report. Investors don’t seem worried about a high-for-longer Fed in all of this. Or at least not yet. For whatever reason that appears to be on the back burner.Friendly reminder that fresh record highs are historically not a good time to put money into risk assets. One could go as far as to say that is a sucker’s move.Having said that, it’s hard to see how we’ll go anywhere but up in today’s shortened trading session. Maybe beyond that as there is little on the calendar for next week.Markets close early today, at 1300 ET and are closed all day tomorrow for July 4. We’ll be back on Monday to preview next week’s action.Housekeeping* PSA: The scheduling of this briefing is being reshuffled a bit due to the success of the live video. This will air closer to the market open, typically between 0800 and 0900 ET. Free subscribers can join live. The recording will be available to premium subscribers.* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks The Contrarian’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →

Tesla Delivery Relief, Concern For Payrolls

Jul 2, 202500:10:04Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events likely to move markets. It is Wednesday, July 2. Hot off the press: Read this month’s update on the Contrarian Portfolio here.State of PlayTesla (TSLA ) just reported second quarter deliveries. These fell short of estimates but apparently not enough to scare investors as the stock is moving higher in the pre-market. As we eye or board of indicators for signs of direction at 0915 ET:* Stock index futures aren’t doing anything. No major US index is moving more than 0.2% from the break-even point;* Commodities are moving higher. WTI crude oil is up 1.2% to trade around $66/barrel. Copper +2%. Gold is unchanged. Silver +1%;* Cryptos also up a bit. Bitcoin +1% to $107,500;* Bonds are selling off a bit. The 10-year yield is up 3 basis points to 4.29% (yields move inversely to prices).Today’s Known EventsTesla sales were the big one. Global sales dropped more than anticipated but not by much. There was good news on the autonomous vehicle front, which helps sentiment.Rivian (RIVN ) for its part also reported a drop in Q2 deliveries. Maybe this is an indication consumers are starting to scale back big-sticker item purchases? It’s worth asking the question…ADP Nonfarm Payrolls declined by 33,000 versus an expectation of +99k. Last month was revised downward to also become negative. This is a big miss. It should have no bearing on the government’s non-farm payrolls figure, which will be out tomorrow. For this reason this will likely be ignored by the market. But there is no reason the ADP data is any less valuable and bears keeping an eye on for this reason. Over the long term, you figure the ADP and government figures will track each other.The Bottom LineAre investors being too sanguine about Tesla deliveries? Quarterly sales dropped year-over-year for the second straight period. But the number (384k) was close enough to analyst estimates (389k) to be considered a wash. Plus the autonomous vehicle stuff and it’s enough for investors to throw caution to the wind and bid up the stock.The ADP figure, ignored by the market, could be a cause for concern. As we said in our monthly portfolio update, jobs growth has so far held up. This could be a sign that this is starting to turn. Or it could be an outlier. Either way, the market don’t care. If tomorrow’s non-farm payrolls number reinforces this trend, there will certainly be a sell-off, if only a short term one. But then, the ADP figure is not a leading indicator for non-farms.Add it up and today’s data really wasn’t great. Investors seem to be ignoring a lot of potentially bad news. That may be because they have good reason to look past all of it, at least until tomorrow. Or it could be a sign of tougher days ahead….Coming Up…Tomorrow’s briefing will follow non-farm payrolls at 0830. It will be the last briefing before July 7 as markets are closed this Friday for the July 4 holiday. Housekeeping* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks The Contrarian’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →

Focus Turns From Middle East to Fed

Jun 16, 202500:06:10Tap to summarizeGood morning contrarians! Welcome to the Daily Contrarian, our morning look at events likely to move markets. It is Monday, June 16, 2025.State of PlayA return to normalcy appears to be on deck, judging by or board of indicators. As of 0755 ET these are pointing to risk-on:* Stock index futures are rising, led by small caps. The Russell 2000 is up 1.1% with S&P 500 and Nasdaq both 0.6% to the good;* Commodities have returned to earth. WTI crude oil is down 1% to trade around $70.50/barrel. Copper is effectively unchanged. Gold and silver down just 0.5%;* Cryptos are rallying. Bitcoin is up * Bonds are unchanged. The 10-year yields 4.44%.Known Events to WatchThe New York Empire State Manufacturing Index, at 0830 ET, is the only economic data release of note and it’s by no means a major indicator. There is an economist survey, which is for a decline of 5.9. That’s actually an improvement over the -9.2 recorded last month.Tomorrow we get retail sales and industrial production. Wednesday is Fed Day, with the Fed widely expected to hold rates steady. Markets are closed Thursday for Juneteenth. Friday brings earnings from Kroger (KR ), Accenture (ACN ), Darden Restaurants (DRI ), and CarMax (KMX ) The Bottom LineWe told you on Friday that markets were already poised to brush off the Iran-Israel stuff, with oil the only real mover. And here we are, with stocks and cryptos recovering and oil dropping to below where it was before the Israeli air strikes.There could be another shoe to drop in the Middle East of course, but that’s not how investors are playing this right now. This means the catalyst for the week will likely be the Fed on Wednesday. Investors will be looking for an indication, any indication, that the Fed is willing to cut rates. If we get that then markets should rally. If not, then it may not matter much in the whole scheme of things judging by how willing investors are to shrug off unwelcome news.Things should otherwise be quiet. Summer is effectively here, even if the calendar doesn’t officially turn for a few more days. That means lower trading volumes. With that in mind, The Contrarian will likely not return until Wednesday, to preview the Fed. Unless something unexpected happens of course.Housekeeping* PSA: The scheduling of this briefing is being reshuffled a bit due to the success of the live video. This will air closer to the market open, typically between 0800 and 0900 ET. Free subscribers can join live. The recording will be available to premium subscribers.* Obviously this is not investment advice (duh). Do your own research, make your own decisions.* Read this month’s portfolio update letter here. The Substack chat tracks The Contrarian’s trades in (almost) real time.* If this daily thing is drowning your inbox and/or you CBF to bother with it and prefer to just get the guest feature or actionable highlights — you can control these settings on your account page.* Finally, if you enjoy this and want others to experience it, please gift a subscription to your friends (or even your enemies). This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit contrarianpod.substack.com

Transcribe →