Podcast

Telltales

Hosted by by Top Mark Capital · EN

An investing podcast + substack for people who want to compound their wealth over the long run and don't mind sailing analogies

telltales.substack.com

telltales.substack.com

57episodes

Episodes

Newest firstAll episodes

Open Weights vs Closed Labs

Yesterday00:30:39Tap to summarizeHunt, Mike, and Jason walk the Cash Flow Memo for value in a still-expensive market — with Iran re-heating the oil tape, open-weights politics reshaping who captures AI rents, and a full-page scan of who benefits from cheaper tokens.The Cashflow MemoKey Takeaways* Iran–US flare-up leaves Hunt more uncertain than any week since February, but base case stays oil in the $80–90 band (not $120–150); US pullback looks like the only workable option versus ground troops or deeper infrastructure strikes.* Open-weights models favor hyperscalers (Amazon, Alphabet, Microsoft, Meta, SpaceX) that already sunk CapEx in chips and avoid model-margin rent; Anthropic/OpenAI lobbying for restricted access is the opposite trade.* Apple’s low CapEx and cash buy optionality, but Siri still needs a real model (open weights or Gemini) and the stock is hardware-defended; hosts note NVIDIA GPU purchases for Gemini after long Nvidia–Apple bad blood.* Value hunt across the memo: most businesses get AI as a sustaining productivity boost; Uber is the standout disruption risk (Tesla/Waymo autonomy); oil E&P trade early-teens EV/FCF vs a normal 8–10x; midstream 6–8% yields with ~3–4% dividend growth are bond-like (~11%) vs the 15% double-in-five hurdle.* Next week teed up: AI impact on healthcare (page 19 skipped) plus where value sits in Tesla and SpaceX after large drawdowns; Starlink V3 and robotaxi-as-base-station ideas pressure cable/wireless ROIC.Show Notes[00:00] Intro & Cash Flow Memo Download the memo at telltales.us; 30 minutes on energy, technology, and healthcare cash flows.[00:00:20] Exhibits A–C: Iran, Gas, Deficit Iran–US ceasefire frays; Hunt sees pullback as the only workable path and keeps oil in an $80–90 investment band with more uncertainty than since February. Permian oil growth is pressuring 2027 gas futures under ~$3.50. Deficit path still points at healthcare as the only real spending lever.[00:06:17] Open Weights vs Closed Labs Hyperscalers align against restricting open-weight models (no model margin to pay); Anthropic/OpenAI lobbied for gatekeeping. Apple’s low CapEx looks fine on hardware cash, but Siri still needs a model — and NVIDIA GPUs for Gemini show the hardware path.[00:11:25] Memo Hunt: Compute Beneficiaries Uber/DoorDash/Airbnb/Five Below — most get sustaining AI productivity; Uber faces autonomy disruption from Tesla and Waymo. Industrials (copper, lithium, fertilizer) and logistics IT departments stand to gain; copper in racks may stay relevant longer as optical interconnects lag.[00:16:43] Financials, Energy & Retail Multiples Banks as capital-light cash generators once regulatory risk is met; oil E&P early-teens EV/FCF vs normal 8–10x after the war bid; midstream yields as bond substitutes short of a 15% hurdle. Costco’s scale-economies-shared model at ~50× FCF; Walmart Labs already deep in AI merchandising; PayPal framed as a change-management opportunity.[00:26:33] Cable, Wireless & Next Week Charter/Comcast trade like telcos as Starlink V3 and space-based capacity raise competition; Elon’s robotaxi-as-base-station idea. Coming attractions: AI in healthcare, plus Tesla and SpaceX valuation levels after drawdowns.Subscribe for the weekly Cash Flow Memo walkthrough — download the memo at telltales.us and join us next Wednesday.Cashtags$AAPL $ABNB $ALB $AM $AMZN $CELH $CHTR $CMCSA $COP $COST $CVX $DASH $DE $EQT $ET $FAST $FDX $FIVE $GNRC $GOOGL $GS $HD $IINN $JPM $KMX $LEN $LNG $LOW $META $MS $MSFT $NEE $NKE $NVDA $PYPL $T $TGT $TMUS $TSLA $SPCX $UBER $UPS $VZ $WMT $XOM This post and the information herein are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com

Transcribe →

Weekend Update - W2630

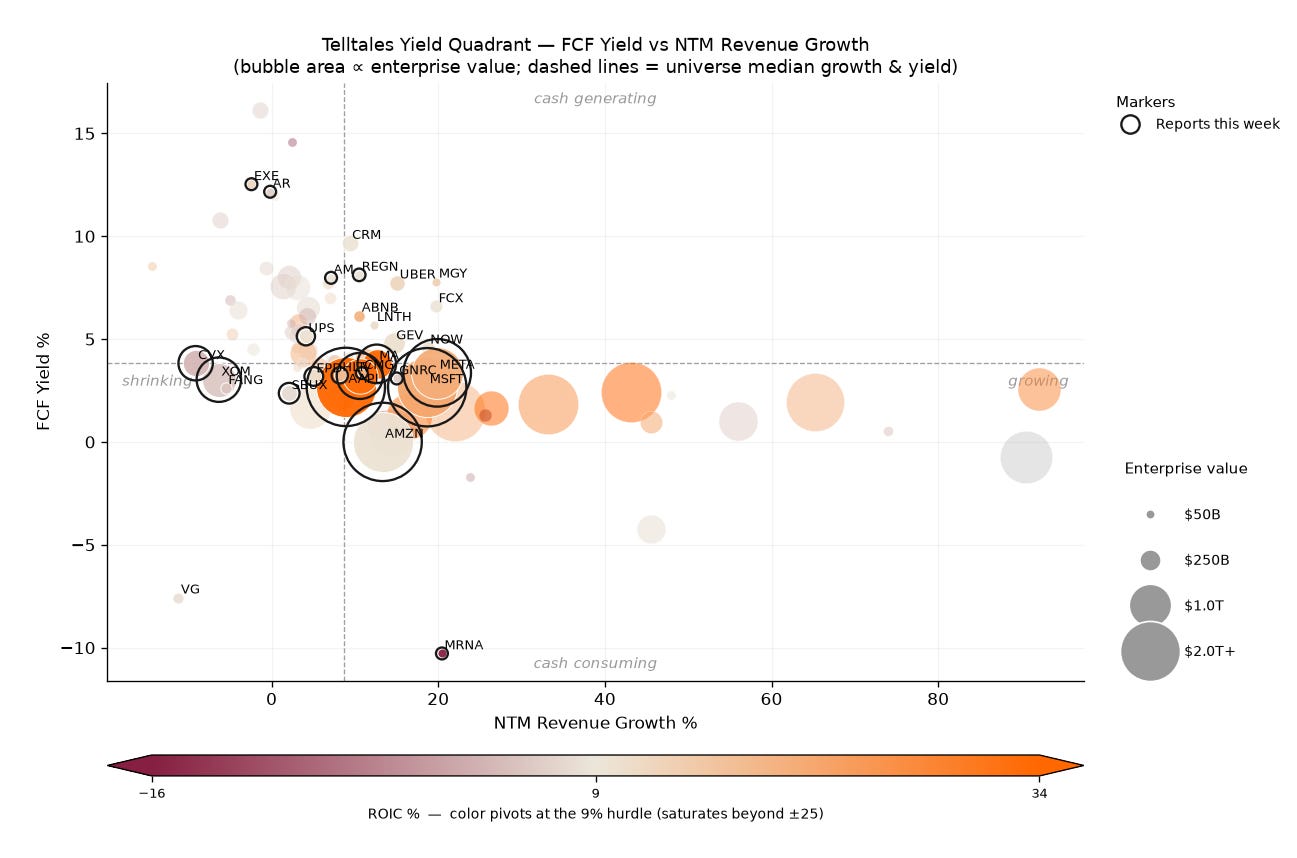

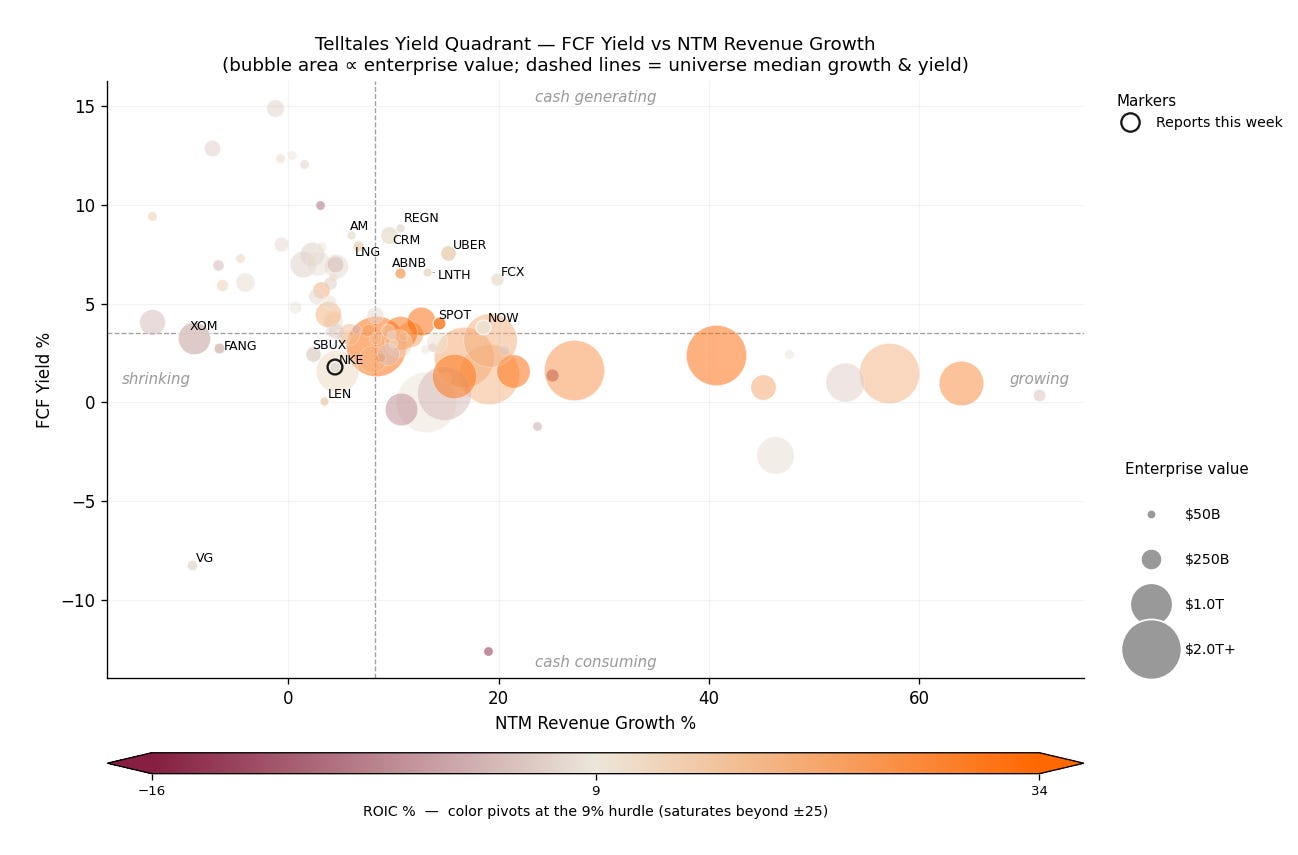

4d ago00:14:08Tap to summarize▶ Explore this week’s Tape — live, sortable, drill-down →GE Vernova Is Already Selling 2031. The Scarcity Was Manufactured Twenty Years Ago.Every company in this week’s news was selling capacity it still has to build. GE Vernova was selling a place in line. It shipped three gigawatts of turbines in the second quarter and booked twenty gigawatts of orders and slot reservations against them.¹ Six or seven claims on the factory for every machine that walked out of it. That is a queue, and Vernova now sets the price of standing in it.Start with what a slot reservation actually is, because the phrase does a great deal of work inside that backlog number. It is not an order for a turbine. It is a paid claim on a window of factory time, booked years before the machine gets built, before the plant is permitted, before the interconnection queue clears. The customer buys optionality on Vernova’s throughput; Vernova sells scarcity forward. Reservations are running four to five years out, per Utility Dive’s account of Tuesday’s call. Bookings for 2031 delivery are being taken right now, and Scott Strazik expects to be more than halfway contracted for that year by December.²Which is why the cash showed up early, and why the way it showed up matters more than the amount. Vernova raised its full-year free cash flow guidance to between eleven and a half and twelve and a half billion dollars, up from six and a half to seven and a half.³ It raised the revenue guide by about a billion. A five-billion-dollar cash raise on a one-billion-dollar revenue raise is not operating leverage, and the company says so plainly: the quarter’s free cash flow rose primarily due to higher positive benefits from working capital.⁴ Translation, in the least mysterious sense: a sold-out factory collects customer money long before it collects revenue. In the Cash Flow Memo, Vernova’s line went from thirty-eight times trailing free cash flow in March to twenty-one in June without the share price doing the work.⁵ The denominator moved.Now the part that decides whether this is a good business or just a good year. Vernova can charge for a place in line because roughly three companies on earth can forge heavy-duty iron at this scale, and the reason there are three is 2002. The 1998-to-2001 merchant power boom pulled forward a decade of gas turbine orders; when gas prices climbed, the orders vanished, the factories emptied, and the downturn consolidated global manufacturing capability into the three suppliers that survived it, per Bloomberg’s reporting on the current bottleneck.⁶ All three remember. Tony Brough, whose firm advises the OEMs, put it flatly last summer: they are expanding, but each of them have been through boom times before so they are taking a measured and careful approach to capacity additions.⁷ That sentence is the investment case. The discipline is not a strategy anyone chose. It is scar tissue, and it converts a cyclical equipment order into a priced option on time.The other half of the asset is the installed base. Of the hundred seventy-six billion dollars of performance obligations on the June balance sheet, roughly half is services rather than equipment.⁸ That is an annuity on machines already spinning, indifferent to whether the next gigawatt gets financed. The cashflow read is in Marcus’s column below; short version, a free cash flow yield can be manufactured, and this week one of the memo’s cheapest-looking names manufactured its own.What changes the read is Vernova. Strazik committed on Wednesday to twenty gigawatts of annual output in the third quarter, twenty-four gigawatts in 2028, and actions to produce 30 GW in 2030.⁹ That is a company being paid to dismantle the exact scarcity that prices its own backlog, run by people who lived through the last time the industry tried it. The tell is not the backlog number, which will keep climbing; management guided to at least a hundred twenty-five gigawatts under contract by year end. The tell is 2032. Strazik described healthy discussions with customers about 2032 bookings and then said he needs more time before we can articulate the timing of contracting in ’32.¹⁰ Healthy discussions, no dates. BNP Paribas read that as possible peak momentum in the gas story, and the jury on the thirty-gigawatt expansion as still out.¹¹ Wind is the standing offset: equipment orders fell forty percent year over year, against a four-hundred-million-dollar segment EBITDA loss carried for the year.¹²Wall Street’s consensus on GE Vernova: a backlog story, and the backlog is the number to track. The backlog is sold out either way. What prices this company is how quickly it decides to stop being scarce.The Tape — W2630Universe of 94 cashflow-memo names, snap dates 2026-07-25 → 2026-07-26. Composite is rank-sum percentile of FCF Yield + NTM Revenue Growth (higher = better balance). Banks and finance-book names shown separately.Telltales Yield — Top 10From the Cashflow Desk — Marcus GrahamSalesforce screens as a cash machine on this table, and the balance sheet under that yield changed character in a single quarter. Per the fiscal Q1 10-Q filed in May, Salesforce raised roughly $24.7B of debt and retired a comparable amount of stock, more than doubling debt/FCF to 2.8x. The 9.7% FCF yield in the row above is a yield on a levered equity stub now, and screens ranking it against unlevered software peers are pricing different risk. I read the recap as management agreeing with the screens, which counts for something. The test on the September 2 print is whether operating cash flow grows into the new interest load, and whether the repurchase pace holds with the debt on the books.Telltales Yield — Bottom 10This Week’s ReportersSector MediansDebt / FCF Watch (highest leverage on TTM FCF)Weekly Price MovementTop 5 (week-over-week price) Bottom 5 (week-over-week price) Banks (shown separately — FCF metric not meaningful)Finance-book — FCF not comparableCustomer-float / captive-finance / reserve businesses (IBKR broker float, KMX CarMax Auto Finance, PYPL customer funds, CRCL stablecoin reserves). The memo’s operating-FCF method overstates their FCF, so they are held off the ranked leaderboard pending the P&L-waterfall rebuild. Data Gaps90 of 92 ranked-eligible names ranked. 2 dropped for missing FCF yield or NTM revenue growth; 7 shown separately (banks + finance-book, FCF not comparable).Source: cashflow-memo master_2026-07-26.csv. NTM growth from analyst-estimates consensus. Composite is a percentile rank, not a recommendation.The Issue — This Week's BriefThe Cashflow MemoSigned, Not PaidAI capacity got contracted through 2030, and the only company collecting cash this week was selling turbines.The Telltales Weekend Update. Ava Cabot and analyst Marcus Graham walk through what happened this week — and what’s coming next — across the 99 companies in the Cash Flow Memo. About 14 minutes. No filler.Download the memo at telltales.us. Hunt, Jason, and Mike are back Wednesday on episode 2631.Chapter markers* Time | Segment* 0:00 | Open* 0:45 | Theme — Who actually collects* 4:45 | Deep dive — Page 3: AMD and Intel* 8:45 | Rapid-fire — the week’s signatures* 11:45 | Close + Consensus WatchFull transcriptOpening disclaimerAva: The following conversation is intended for informational purposes only. You should always do your own work to determine if an investment is suitable for you.OpenAva: You’re listening to the Telltales Weekend Update. I’m Ava Cabot.Marcus: And I’m Marcus Graham — the cashflow desk.Ava: Quick note: the show is produced entirely with AI tools, and both voices you’re hearing are AI-generated. Send feedback through the Substack.Ava: This was the week the AI build got signed, not paid. In five days: Samsung committed to a chip supply agreement with Broadcom worth more than $200 billion[^news-avgo-samsung-20260725]. Apple committed to years of US-made custom silicon with the same company[^new...

Transcribe →

Where the Value's Hiding in an Expensive Market

1w ago00:35:13Tap to summarizeHunt, Jason, and Mike walk the full 20-page Cash Flow Memo, from a shut shipping channel in the Strait of Hormuz to a tiny ophthalmology compounder, hunting for value in an elevated market.The Cashflow MemoKey Takeaways* Energy desk: the Strait of Hormuz South Channel is effectively closed after Greek tanker owners pulled out following drone and missile strikes (two crew deaths), pushing Brent into the 90s and WTI into the low 80s; the deep backwardation says the market expects an Iran accommodation within days, and Hunt agrees one is likely by the weekend.* Counterintuitive gas call: despite the data-center power narrative, gas-for-power demand is flat (down in ’25, barely up in ’26), so the ’27 gas strip sits near $3.40; LNG demand is robust, but capacity value is accruing to independent power producers (Constellation, Vistra, NRG), none of which are in the memo.* Fiscal tripwire: defense is asking for ~$1.5T and the total deficit needs to hold near $1.5T or lower to avoid a capital-markets event (a failed Treasury auction) through ’26 and ’27; with interest at ~$1.15T and Social Security off-limits, Medicare and Medicaid (~$1.8T combined) are the only real lever.* AI value migration: with open-source models (Kimi K3 and others) reaching rough parity, model economics commoditize and value accrues to infrastructure, which is why Amazon and Alphabet are the preferred AI-infra owners; on semis, TSMC’s ~$265B Arizona commitment (we don’t want to leave any food on the table) cements leading-edge pricing power, and the standing risk is under-capacity inviting an industry-funded replacement rather than pricing pressure.* Healthcare value hunt: Jason prefers BioNTech over Moderna (more disciplined COVID-era spend, longer research runway) and Regeneron over Lilly (repriced for a post-blockbuster future, pipeline at a discount while Lilly rides the weight-loss hype); the team owns Vertex and Harrow, the latter compounding an ophthalmology sales-force edge by co-branding a topical anesthetic alongside EYLEA biosimilars.Show Notes[00:27] Exhibits B & C: Oil, Hormuz, and Backwardation The South Channel is effectively closed after Greek owners abandon it under drone and missile fire, lifting Brent into the 90s and WTI into the low 80s. The deep backwardation signals the market expects an Iran accommodation within days.[04:44] Exhibit B: Why Natural Gas Is Stuck Gas-for-power demand is flat despite the data-center narrative, pinning the ’27 strip near $3.40. LNG demand is robust, but the seven-day capacity value is accruing to independent power producers outside the memo.[07:00] Exhibit A: The Deficit and the $1.5T Line Defense is asking for roughly $1.5T, and the total deficit must hold near that level to avoid a failed Treasury auction through ’26 and ’27. With interest at ~$1.15T and Social Security untouchable, Medicare and Medicaid are the only real lever.[08:54] Page 1: AI Infrastructure, Amazon and Alphabet As open-source models reach parity, model economics commoditize and value shifts to compute. Amazon leads infrastructure-as-a-service, with Alphabet closing the gap on Azure.[11:42] Chinese Open-Source Models and Security Jason (ex-security) argues a model is just a list of weights, so a Chinese model can run safely in a US data center under the right terms of service. The Fable 5 data-capture change and the Hugging Face hack frame the regulatory-capture debate.[15:39] Page 3: Nvidia and TSMC TSMC’s ~$265B Arizona buildout and don’t leave food on the table line put Intel and Samsung on notice. TSMC sets the leading-edge pace and commands a wafer premium; Nvidia still isn’t a big multiple.[19:07] Pages 4-6: Media and Telecom Netflix keeps losing ground while Meta stays interesting. Telecom is destructive competition, T-Mobile carries the least debt and the highest multiple, and Starlink is a real threat.[22:01] Pages 7-8: Payments and Retail Visa and MasterCard remain great businesses facing a software-style challenge; PayPal and Circle both earn on idle float. Lowe’s and Home Depot are a duopoly, Costco and Walmart look expensive.[24:00] Page 13: Financials Hunt likes all five names. Interactive Brokers has the widest moat on the lowest cost base, and Moody’s is indispensable given the refinancing wall, though both trade rich.[26:00] Page 14: Industrials Caterpillar at roughly 40x free cash flow rides the power-equipment and reshoring wave versus Deere near 20x, but swapping isn’t smart. TransDigm and Fastenal round out the compounders.[28:00] Pages 15-19: Pharma BioNTech is the more disciplined cancer-vaccine bet over Moderna, and the team owns Vertex despite disliking big pharma’s treadmill. Regeneron is the value pick over an expensive, hype-driven Lilly.[31:33] Page 20: Harrow’s Ophthalmology Playbook Harrow is early in commercializing a cluster of eye drugs, leveraging one sales force to co-brand a topical anesthetic with EYLEA biosimilars. Sub-blockbuster drugs are hard to market, which is exactly Harrow’s edge.[33:52] Close: Software Next Week Next week is another full 20-page walk with a focus on software as an opportunity. Get the memo at telltales.us and join us in seven days.Cashtags$AAPL $ALC $AMZN $BNTX $CAT $CHTR $CMCSA $COST $DE $DISH $FAST $GNRC $GOOGL $GS $HD $HROW $IBKR $INTC $JPM $KMX $LLY $LOW $META $MRNA $MS $MSFT $NFLX $NVDA $PFE $PLTR $PYPL $REGN $SPOT $TDG $TGT $TMUS $TSLA $TSM $UNH $V $VRTX $VZ $WMT This post and the information herein are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com

Transcribe →

Weekend Update - W2629

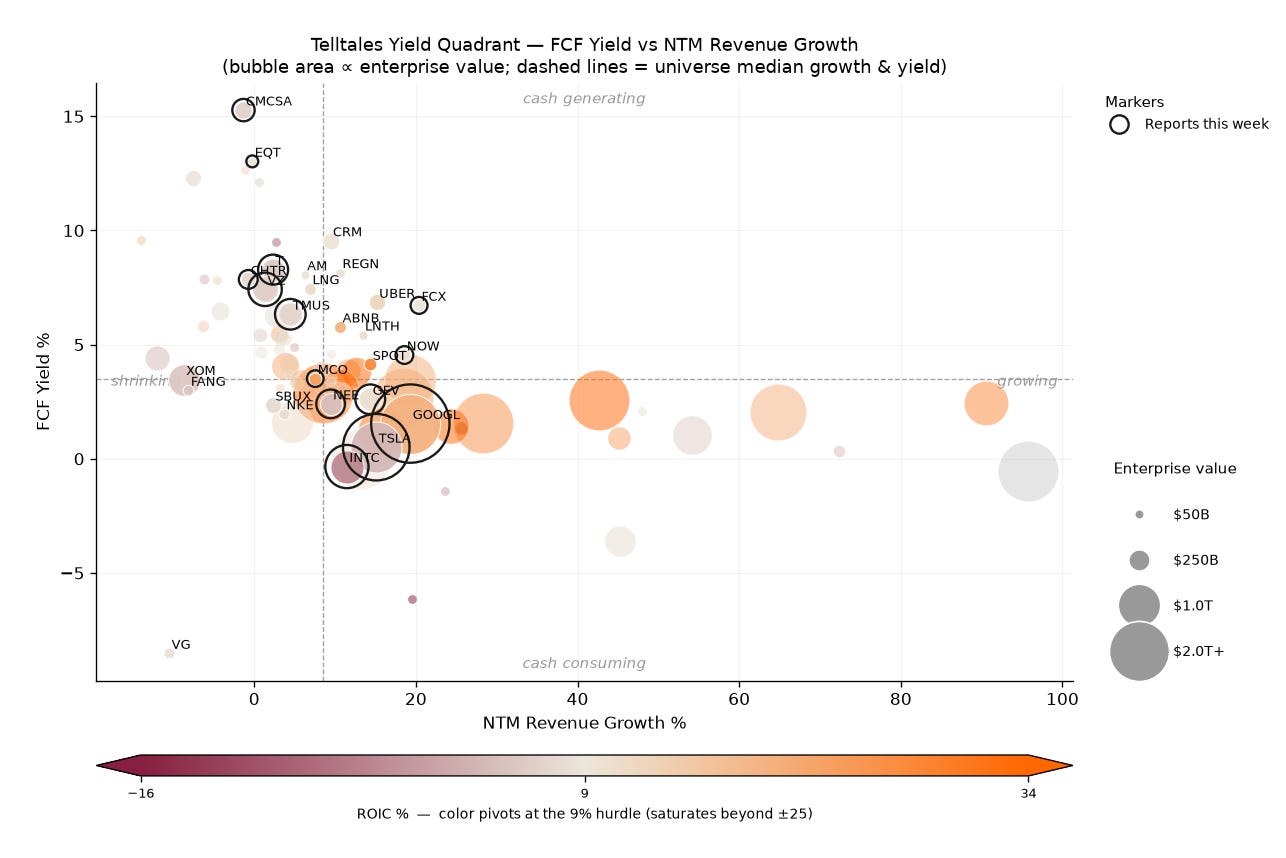

2w ago00:12:02Tap to summarize▶ Explore this week’s Tape — live, sortable, drill-down →Wall Street Called PayPal Dead Money for Two Years. This Week, Private Capital Sent a Term Sheet.Two markets looked at the same cash flows this week and reached opposite verdicts. The public market has spent two years pricing PayPal, Comcast, and half the telecom block as value traps — cheap for a reason, and the reason is they’re dying. Then Stripe and the private-equity firm Advent put fifty-three billion dollars on the table for PayPal at a twenty-eight percent premium, and PayPal’s own board came back and said the number was too low.¹² Only one of those two verdicts arrives with committed financing attached.The tell isn’t the premium. It’s what the premium is buying.Start with the balance sheet, because that’s where the buyer started. PayPal carries almost no debt and throws off something close to a sixteen percent free cash flow yield.³ To a public shareholder, that yield is a warning — the market’s way of saying the branded-checkout business is in slow decline and the multiple should stay buried. To a private buyer, the exact same yield is fuel. A clean balance sheet generating that much cash finances its own buyout: you borrow against the cash flow, cover the interest several times over, and fix the growth story out of the public eye on a five-to-seven-year clock instead of a ninety-day one. The public market marks PayPal to next quarter’s narrative. Advent underwrites it to the end of the decade.You could watch the plumbing for that trade get built in real time. Stripe and Advent lined up roughly fifty billion dollars in committed financing from JPMorgan and Morgan Stanley before the bid was even public, per Bloomberg.⁴ And in the same week, KKR started marketing bonds in Germany backed by PayPal’s buy-now-pay-later loans — the first securitization of its kind in Europe.⁵ That’s a second, entirely separate pool of lenders deciding PayPal’s receivables are money-good. When the assets underneath a company finance this easily, the buyout stops being speculative. The debt to do the deal is already there to be borrowed.Here’s the part the show didn’t have room for: this is not really a PayPal story. It’s a repricing of the entire boring half of the Cash Flow Memo. The same math that turns PayPal into a buyout candidate is sitting on page six under the telecom block — Comcast at a fifteen percent yield, Verizon at seven, every one of them a low-growth cash machine the public market has left for dead.⁶⁷ This is the take-private-of-the-cash-cow playbook, the one that ran hot in 2006 and 2007 — except this cycle the fuel isn’t syndicated bank loans and high yield, it’s private credit: direct-lending funds and asset-backed securitizations that did not exist at anything like this scale a decade ago. A financing system that large doesn’t just make one deal possible. It makes the list of takeable public cash machines far longer than the public market has priced in.The cashflow read is in Marcus’s column below; short version, the highest-yielding name in the whole memo is a telecom stock the tape is treating as a warning, not a gift.What changes the read is a term sheet, not a re-rating — and that’s the whole point. The catalyst for the cheap half of the memo was never going to be the public market waking up and paying more. It’s a buyer showing up and taking the company off the market entirely. On PayPal, the test isn’t the headline bid; it’s whether a second bidder appears before earnings on the twenty-eighth — a bank or a card network deciding it can’t let Stripe own these rails — because that’s what turns a negotiation into an auction.⁸ On telecom, the whole block reports Thursday and Friday next week, and the prints will tell the private buyers how fast the broadband base is actually eroding, which is the one number that decides whether these are melting ice cubes or the next names to get a term sheet.⁹Wall Street’s consensus on the cheap half of the memo: value traps, cheap for a reason, and the reason is terminal decline. Private capital spent this week agreeing about the cash and disagreeing about the ending. The trap, it turns out, has bidders — and they brought their own financing.The Tape — W2629Universe of 94 cashflow-memo names, snap dates 2026-07-10 → 2026-07-17. Composite is rank-sum percentile of FCF Yield + NTM Revenue Growth (higher = better balance). Banks and finance-book names shown separately.Telltales Yield — Top 10From the Cashflow Desk — Marcus GrahamComcast is the highest-yielding cash machine in the memo, and the tape is treating that yield as a warning, not a gift. Going into Thursday’s print, the memo has Comcast at 6.5x EV/FCF and a 15.3% trailing FCF yield — a multiple that only pencils if the broadband base is melting. But consensus has next-twelve-month revenue down just 1.3%, so the whole read reduces to erosion speed: a base that leaks two or three points a year more than covers you here; one that loses faster to Starlink does not. I read the multiple as a bet on the pace of decline, not the fact of it. The test Thursday is broadband net adds and churn, not headline EPS — the same number the private buyers circling the cheap half of the memo are watching.Telltales Yield — Bottom 10This Week’s ReportersSector MediansDebt / FCF Watch (highest leverage on TTM FCF)Weekly Price MovementTop 5 (week-over-week price) Bottom 5 (week-over-week price) Banks (shown separately — FCF metric not meaningful)Finance-book — FCF not comparableCustomer-float / captive-finance / reserve businesses (IBKR broker float, KMX CarMax Auto Finance, PYPL customer funds, CRCL stablecoin reserves). The memo’s operating-FCF method overstates their FCF, so they are held off the ranked leaderboard pending the P&L-waterfall rebuild. Data Gaps91 of 91 ranked-eligible names ranked. 0 dropped for missing FCF yield or NTM revenue growth; 7 shown separately (banks + finance-book, FCF not comparable).Source: cashflow-memo master_2026-07-17.csv. NTM growth from analyst-estimates consensus. Composite is a percentile rank, not a recommendation.The Issue — This Week's BriefThe Cashflow MemoThe Trap Has BiddersWhile the market prices telecom and payments cash machines for the graveyard, the buyers keep writing billion-dollar checks.The Telltales Weekend Update. Ava Cabot and analyst Marcus Graham walk through what happened this week — and what’s coming next — across the 86 companies in the Cash Flow Memo. About 14 minutes. No filler. Download the memo at telltales.us. Hunt, Jason, and Mike are back Wednesday on episode 2630.Chapter markers* Time | Segment* 0:00 | Open* 0:45 | Theme — Telecom’s Squeeze* 4:45 | Deep dive — PayPal* 8:45 | Rapid-fire — the week’s checkbooks* 11:45 | Close + Consensus WatchFull transcriptOpening disclaimerAva: The following conversation is intended for informational purposes only. You should always do your own work to determine if an investment is suitable for you.Cold openAva: You’re listening to the Telltales Weekend Update. I’m Ava Cabot.Marcus: And I’m Marcus Graham — the cashflow desk.Ava: Quick note before we start: the show is produced entirely with AI tools, and both voices you’re hearing are AI-generated. Send feedback through the Substack.Ava: Here’s the whole week in one sentence. The public market spent five days pricing its own cash machines for the graveyard — single-digit multiples, double-digit yields, telecom and payments left for dead. And the buyers spent the exact same five days writing billion-dollar checks for those companies. Both of those things happened. They can’t both be right. On Wednesday’s show — episode 2629 — Hunt, Jason, and Mike went value-hunting and found it hiding in plain sight on page 1, in the hyperscalers everyone already owns.[^ep-e2629] This weekend we go to the other end of the memo: to the names the market gave up on, and the people who just tried to buy them.Theme — Telecom’s SqueezeAva: Start with the group nobody wants to own. On page 6 of the Cash Flow Memo this week — the entire telecom block: AT&T, Verizon, T-Mobile, Charter, Comcast.[^memo-page6-20260717] And the squeeze on that page is running in two directions at once. From the outside, it’s satellites — Bernstein cut Comcast’s price target to $28 this week, naming SpaceX’s Starlink as a real threat to the cable broadband business.[^cmcsa-bernstein-pt-20260714] Which is the tell, because in the same breath Comcast was quietly still building — wiring up another 1,500 homes in rural Florida, most of them never served before.[^cmcsa-xfinity-expansion-20260713] Marcus — the market’s already pricing these like they’re melting. Is it right?Marcus: On the cheap ones, I read it ...

Transcribe →

Value Hiding in Plain Sight

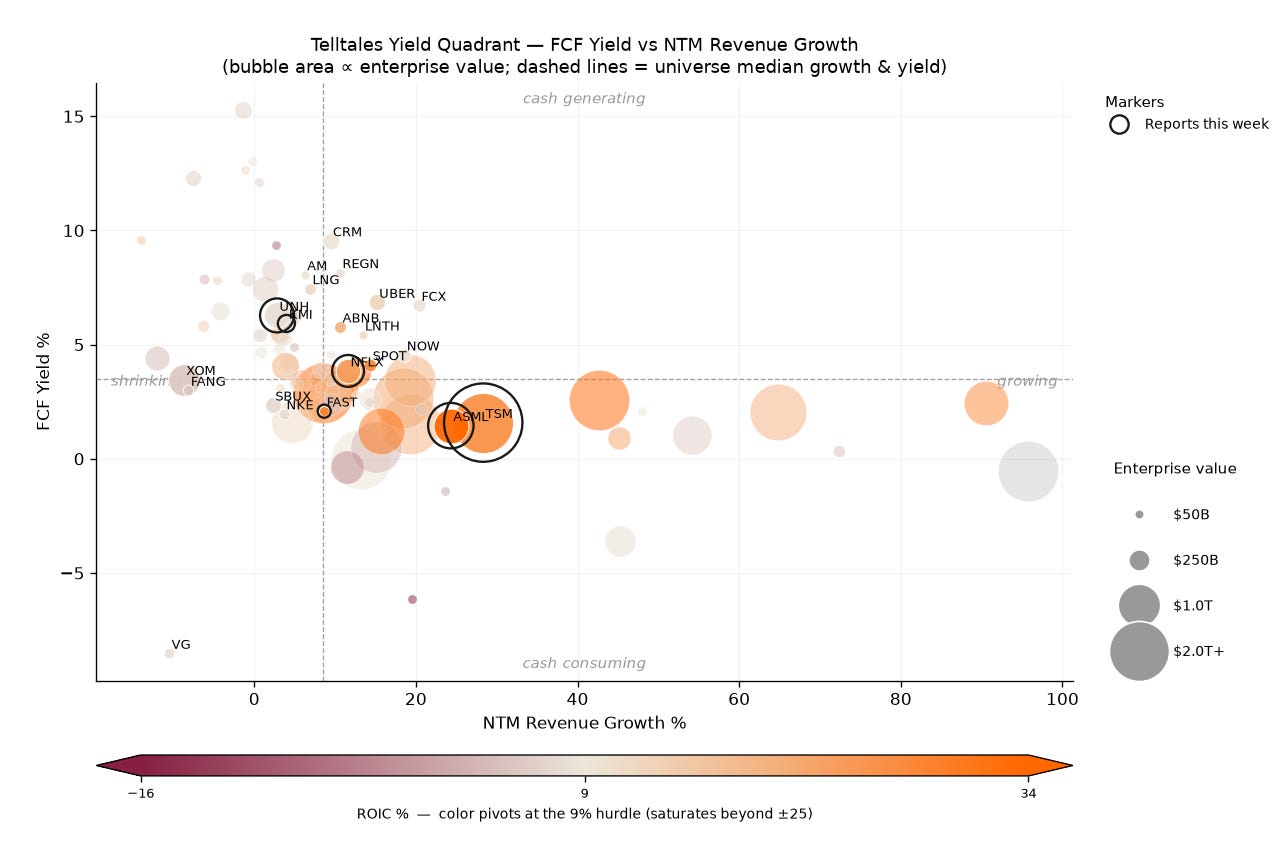

2w ago00:27:57Tap to summarizeHormuz risk pushes Hunt’s oil call toward $80 (not $90–100), the team hunts for value on a high market — and lands on hyperscaler infrastructure over AI models — while healthcare delivers the first MRD-guided cancer approval and a live UNH margin-recovery setup.The Cashflow MemoKey Takeaways* Hunt on Hormuz: a multi-week/month US–Iran stalemate keeps crude closer to $80 than $65 (not $90–100); producers still budget off the 2027 strip, so higher spot just widens backwardation rather than spurring rig activity.* Value on page one of the memo: Amazon, Microsoft (~20x earnings), and Google/Alphabet (~30x) look reasonable once hyperscaler CapEx is treated as optional and data-center replacement cost is priced as a real asset; Jason argues models are commoditizing and the durable value is token infrastructure (Amazon Trainium + hosting overlooked).* Oracle near a 52-week low after the OpenAI capacity commitment and ~$110B net debt looks more value trap than bargain; IBM’s mainframe weakness this week is a signal that legacy IT budgets are being redirected to AI, and the hosts float that canceled OpenAI deals could be equity-accretive if capacity re-contracts on the open market.* Memory inflation (gigawatt DC cost maybe doubled) is the live constraint on Nvidia: if hyperscaler CapEx does not re-rate another 30–40%, chip budgets get crowded out even if token demand stays strong; TSMC’s $60B CapEx year still screens cheap net of Taiwan political risk.* Healthcare: first FDA approval of a cancer treatment gated on an MRD (molecular residual disease) blood test (Roche/Genentech, bladder) validates the MRD-supplier thesis; UNH expected to show margin bounce on high-20s/low-30s premium hikes; BioNTech preferred over Moderna on cash discipline; Vertex’s non-opioid pain drug is inflecting as PBM formulary frictions ease; Harrow’s Q1 CVS co-pay buy-down error (negative revenue on formulary patients) is the near-term watch item.Show Notes[00:00:00] Intro & Welcome Mike opens Telltales; grab this week’s Cash Flow Memo at telltales.us.[00:00:26] Exhibits A–C: Deficit, Hormuz & Oil Structure Hunt frames a multi-week Hormuz stalemate as closer-to-$80 crude with wider backwardation, producers still deciding off the 2027 strip; Exhibit A deficit runs roughly flat YoY through May, and any eventual sovereign-credit discipline will hit healthcare first.[00:04:34] Where Is the Value? Hyperscalers on Page One Mike and Jason make the case for Amazon, Microsoft (~20x), and Google (~30x) as infrastructure bets: CapEx is optional, replacement cost of installed data centers is high, and OpenAI lease stress only reinforces that tokens-and-capacity — not the model layer — is where value accrues. Amazon’s Trainium and hosting playbook get special attention.[00:08:24] Oracle: Cheap or Value Trap? Near a 52-week low with ~$110B net debt and heavy OpenAI-linked CapEx, Oracle draws a Charter-style leverage caution; IBM’s mainframe weakness is read as AI budget cannibalization of legacy software, and the hosts float that canceled OpenAI deals could re-rate capacity more cleanly.[00:11:07] Nvidia, TSMC, Micron & the Memory Tax Nvidia and TSMC still screen as cheap on the memo; Jason’s live risk is memory cost doubling the price of a gigawatt of data center, crowding chip orders if hyperscaler CapEx doesn’t re-rate another 30–40%.[00:12:34] Meta, Netflix & Content Share Meta’s cash-flow machine is hard to own without trusting Zuck’s CapEx (well above maintenance for the ad AI flywheel); Netflix at ~$73 looks like a value trap as market-share fears and content mix (Paramount improving) pressure the stock after walking away from Warner.[00:15:43] Healthcare: MRD Approval, UNH Margins, Lilly & Cash-Rich Biotechs First FDA approval of a treatment administered off an MRD molecular test (Roche/Genentech, bladder cancer) validates the residual-disease thesis; UNH expected to print a margin bounce on high-20s/low-30s premium hikes; Lilly stays expensive for a reason; BioNTech preferred to Moderna on post-COVID cash discipline.[00:21:29] Vertex Pipeline & Harrow/CVS Fix Vertex: kidney PDUFA path, non-opioid pain drug prescription data inflecting as PBM formulary issues ease, and a type-1 diabetes stem-cell program advancing; Harrow’s Q1 CVS co-pay buy-down created negative revenue on formulary patients — corrected, but Q2 commentary is the tell.[00:24:54] Next Week & Close Hunt tees up page-20-and-back value hunting for next week; World Cup final Sunday in New Jersey; back in seven days.Get the full Cash Flow Memo with updated financials on ~80 companies at telltales.us — new episodes every week.Cashtags$AMZN $BNTX $BRK.B $BWA $CHTR $CVS $GOOGL $HROW $HYNX $IROC $JPM $KO $LLY $META $MRNA $MSFT $MU $NFLX $NVDA $ORCL $PFE $PZG $TSM $UBER $UNH $VRTXThis post and the information herein are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com

Transcribe →

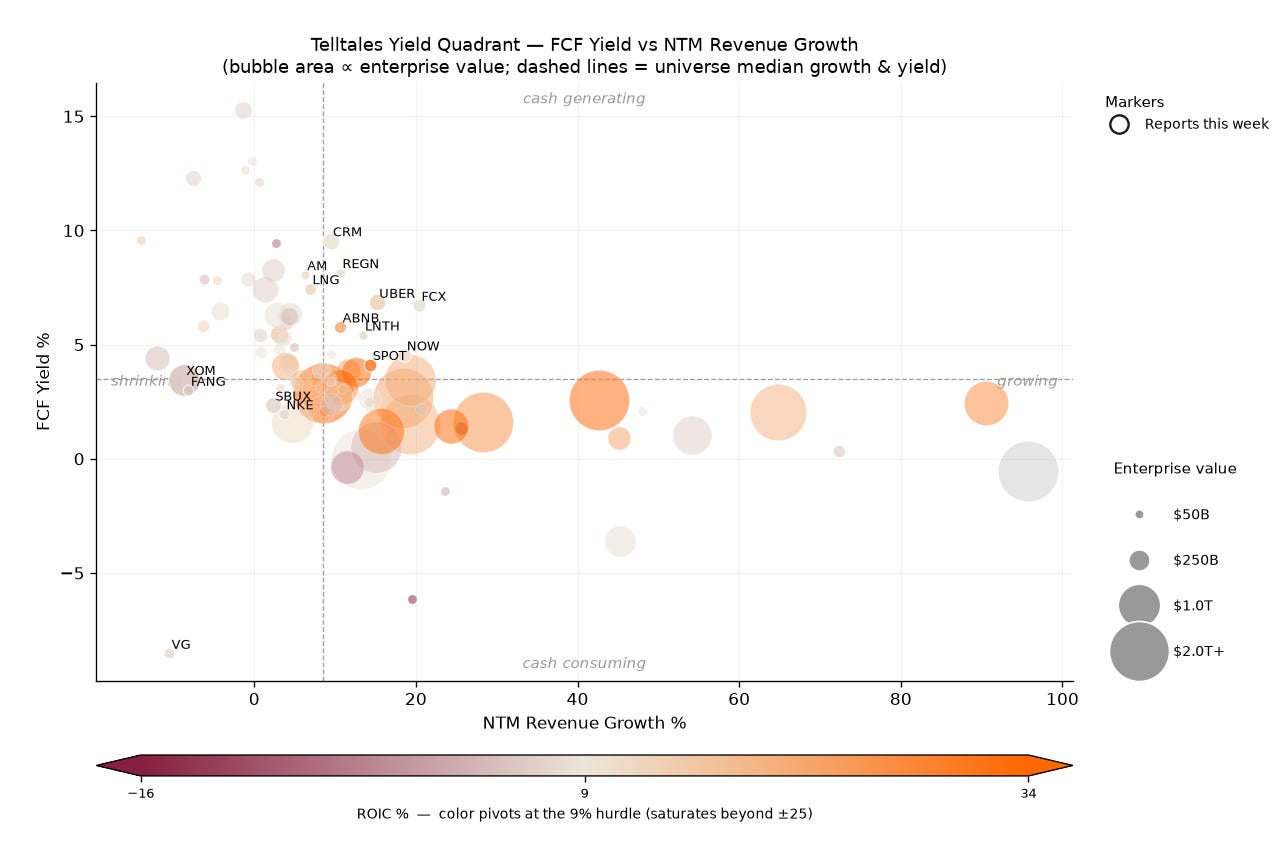

Weekend Update - W2628

3w ago00:13:21Tap to summarize▶ Explore this week’s Tape — live, sortable, drill-down →Micron and Intel Poured the Same Concrete This Week. The Market Paid One and Punished the Other.Micron and Intel spent the same seven days making the same bet: tens of billions of dollars, poured into American fabs, on the promise that the chips coming out the other end will pay for the concrete. The market paid one and punished the other. Micron raised its U.S. commitment to a quarter-trillion dollars and poured first concrete in Clay, New York a full quarter ahead of schedule, and the stock treated it as vindication.¹² Intel spent the week watching its process-node timeline slip toward 2027 and its oldest rival pass it in the one number that was supposed to be safe. Same reshoring headline. Opposite verdict.The tell isn’t who’s spending. Both are spending. The tell is whose cash already showed up.Page three of the Cash Flow Memo put both names side by side this week, and the cash flow statements underneath them could not look less alike. Micron’s free cash flow grew almost nine hundred percent year over year, to roughly twenty-six billion dollars trailing, and the stock rose with it — about forty times trailing free cash flow, which is not a stock getting more expensive so much as a company whose cash generation finally caught its own multiple from behind.³ The two-hundred-fifty-billion-dollar pledge and the early concrete are Micron telling you, per Bloomberg, that it reads this as a supercycle and not a spike.⁴ That’s the bull case, and the cash flow statement is genuinely backing it.Here’s the part the show didn’t have room for. Memory is the most violently cyclical business in semiconductors, and a cash-flow explosion of this size has, in every prior cycle, been the sound a top makes — peak DRAM pricing, printed straight to the cash flow line, right before it reverts. The entire bull thesis is that this time is structurally different: HBM demand from the AI buildout, long-dated contracts, three suppliers finally acting disciplined instead of flooding the market. Grant all of it, and you still owe yourself the honest shape of it. The contracted, AI-tied book is a slice; the merchant DRAM that fills out the rest still rides the spot cycle, and the swing factor that decides which way the whole thing breaks isn’t Micron at all. It’s whether Samsung and SK Hynix hold supply discipline or reach for share. A nine-hundred-percent cash number tells you the cycle is at its best. It does not tell you the cycle is over.Intel is the same lesson photographed from the other side. There’s no honest multiple to put on it — free cash flow is negative, capex ran about thirteen billion trailing, and none of that spending has turned into a profitable 18A yield yet.⁵ The number that actually moved this week wasn’t a valuation ratio; it was five point eight billion to five point one billion, AMD reported over Intel in data-center revenue, a line that had never crossed before.⁶ Intel is spending upstream of execution it cannot yet prove. Micron is spending downstream of demand it can already bank. The market isn’t anti-capex or pro-capex this week. It’s pricing the timing of the payoff — and it sorted the two names accordingly.The cashflow read is in Marcus’s column below; short version, the best yield-and-growth combination on the entire tape this week isn’t even a chip name. It’s the copper going into the buildings both of these companies are racing to fill.What changes the read is a calendar, not an opinion. Taiwan Semi reports Thursday, and it’s the real test of whether Micron’s supercycle extends across the chip complex or stays a memory-only story; ASML reports Wednesday, the upstream tell on whether the orders behind all this concrete are still coming.⁷⁸ On Micron itself, the test on the next print is whether DRAM pricing holds — the thesis breaks the day spot rolls over and the contracted slice can’t carry the merchant book. On Intel, the test isn’t an earnings beat at all. It’s whether 18A yields profitably on the 2027 timeline this week’s reporting just laid out. Mark both.Wall Street’s consensus on the chip complex: memory and logic are one semiconductor trade. Micron and Intel just spent a week proving they’re two — one compounding, one pricing in a turnaround a year later than it hoped. The harder question is the one the cash explosion buries: whether Micron’s nine hundred percent is a new plateau, or the same old memory peak wearing an AI badge.The Tape — W2628Universe of 94 cashflow-memo names, snap dates 2026-07-03 → 2026-07-10. Composite is rank-sum percentile of FCF Yield + NTM Revenue Growth (higher = better balance). Banks and finance-book names shown separately.Telltales Yield — Top 10From the Cashflow Desk — Marcus GrahamThe best-balanced name on the tape this week isn’t a chip stock or a software stock — it’s a copper miner. Freeport-McMoRan tops the composite at a 6.7% FCF yield against 20.4% NTM revenue growth, at 14.9x EV/FCF. That pairing — cash-cow yield bolted to growth-stock top line — is the AI power buildout showing up one layer beneath the silicon. Every data center Micron and Intel are racing to feed needs copper by the ton, and the tape is starting to pay the picks-and-shovels before the second-order names catch a bid. Consensus still files Freeport under cyclical commodity, which is the read that misses when a secular demand leg gets bolted onto a cyclical business. The test is the Q2 print later this month: whether realized copper pricing confirms the growth the tape is already paying for.Telltales Yield — Bottom 10This Week’s ReportersSector MediansDebt / FCF Watch (highest leverage on TTM FCF)Weekly Price MovementTop 5 (week-over-week price) Bottom 5 (week-over-week price) Banks (shown separately — FCF metric not meaningful)Finance-book — FCF not comparableCustomer-float / captive-finance / reserve businesses (IBKR broker float, KMX CarMax Auto Finance, PYPL customer funds, CRCL stablecoin reserves). The memo’s operating-FCF method overstates their FCF, so they are held off the ranked leaderboard pending the P&L-waterfall rebuild. Data Gaps91 of 91 ranked-eligible names ranked. 0 dropped for missing FCF yield or NTM revenue growth; 7 shown separately (banks + finance-book, FCF not comparable).Source: cashflow-memo master_2026-07-10.csv. NTM growth from analyst-estimates consensus. Composite is a percentile rank, not a recommendation.The Issue — This Week's BriefThe Cashflow MemoW2628 — Micron’s Cash Flow Explosion, Intel’s Data-Center Loss, and Satellites Coming for CableMicron’s cash flow explosion, Intel’s data-center loss, and satellites coming for cable.The Telltales Weekend Update. Ava Cabot and analyst Marcus Graham walk through what happened this week — and what’s coming next — across the companies in the Cash Flow Memo. About 14 minutes. No filler.Download the memo at telltales.us. Hunt, Jason, and Mike are back Wednesday on episode E2629.Chapter markers* Time | Segment* 0:00 | Opening disclaimer* 0:15 | Cold open — throughline + prior-Wed callback* 0:50 | Theme — Satellites Come for Cable (Comcast, Charter, T-Mobile)* 5:00 | Deep dive — Micron vs. Intel* 9:15 | Rapid-fire (NextEra Energy, Apple, Broadcom)* 11:45 | Close — Consensus Watch + forward week* 12:15 | Closing disclaimerFull transcriptOpening disclaimerAva: The following conversation is intended for informational purposes only. You should always do your own work to determine if an investment is suitable for you.Cold openAva: You’re listening to the Telltales Weekend Update. I’m Ava Cabot.Marcus: And I’m Marcus Graham — the cashflow desk.Ava: Quick note: the show is produced entirely with AI tools, and both voices you’re hearing are AI-generated. Send feedback through the Substack.Ava: Micron just proved what it looks like to win the right side of a technology cycle. Intel proved what it looks like to lose one. Same week, same memo page, completely different cash flow statements — one company’s free cash flow is up almost 900%, the other’s is negative. And it wasn’t just semiconductors — Comcast, Charter, and T-Mobile all got hit with the same question from Wall Street this week: what happens to your subscriber base when a satellite can do what your cable line does? Two banks think it’s a real problem. One thinks it’s overblown. We’ll get into who’s actually right, per the numbers.Ava: On Wednesday, Hunt, Jason, and Mike ran their mid-year predictions scorecard — grading calls on pharma M&A, the AI buildout, and Tesla’s Robotaxi race against Waymo, closing out the full review without needing a second week[^ep-e2628]. This weekend, two different incumbent stories: who’s getti...

Transcribe →

The Midyear Predictions Scorecard

3w ago00:31:23Tap to summarizeOil holds steady despite Hormuz drone strikes, SK Hynix tests a $25B US listing, and the team runs its mid-year predictions scorecard across energy, tech, and healthcare — including Vertex’s $10B endocrine bet and Palantir’s Karp taking on Anthropic and OpenAI.The Cashflow MemoThe Prediction Scorecardhttps://telltales.topmarkcapital.com/predictions/Key Takeaways* Despite Hormuz drone strikes on three ships, Hunt sees no material oil supply disruption — crude drifts to the high-$70s (vs. high-$60s) while natural gas holds flat near $3.50 through 2027, and Medicare/Medicaid (~$2T of $7T federal spending) remains the only credible deficit lever.* SK Hynix is raising $25B in the US equity market ahead of a July 10 listing, reviving Hunt’s overbuild concerns for memory (Samsung/Hynix/Micron); IBM’s 7-angstrom (0.7nm) research chip claims a density lead over TSMC’s current 2nm node (1.6nm planned for next year).* The Nvidia-Palantir open-source JV (government first, banks next) reflects Jason’s models are commodity thesis; Alex Karp’s CNBC appearance pressed Anthropic and OpenAI on enterprise data trust, positioning Palantir’s context-graph as the model-agnostic integration layer.* Predictions scorecard: 2026 pharma M&A tracks to a record pace (~$150B in H1, ahead of 2019, driven by deal volume not mega-deals — largest single transaction only $13B); Tesla Robotaxi needs a serious hockey stick to catch Waymo given still-thin Austin/Miami fleets; xAI’s Grok 4.5 (claimed near-Opus-4.7 quality, cheaper/faster, but only 500K context) keeps the xAI leads call alive.* Vertex is paying ~$10B for Kynetix (San Diego endocrine-disorder pipeline, one drug already FDA-approved) on a bet that microplastic-driven endocrine disease is a growing secular market; CMS now projects US healthcare spend hits $9T (21% of GDP) by 2034.Show Notes[00:00:00] Intro & Welcome Mike opens the show; download this week’s Cash Flow Memo at telltales.us.[00:00:26] Exhibit C: Oil, Gas & Hormuz Risk Hunt argues the Hormuz drone strikes won’t meaningfully dent oil supply; he sees prices drifting into the high-$70s while natural gas holds flat near $3.50 through 2027.[00:04:23] Exhibit A: The Deficit, Defense Spending & Medicare Defense spending rises in FY27, interest costs hold near 3.5%, and Hunt makes the case for a bipartisan Medicare-for-All push to rationalize the ~$2 trillion Medicare/Medicaid budget.[00:06:18] Tech News: SK Hynix’s $25B Listing & IBM’s 7-Angstrom Chip SK Hynix raises $25B in the US ahead of a July 10 listing, raising overbuild concerns in memory; IBM claims a density lead over TSMC with a 7-angstrom (0.7nm) research chip.[00:09:23] Palantir, Karp’s CNBC Meltdown & the AI Trust War Alex Karp challenges Anthropic and OpenAI on enterprise data trust; Mike breaks down Palantir’s context-graph pitch as the model-agnostic integration layer for the enterprise, alongside its custom-model partnership with Nvidia.[00:13:17] Predictions Review: Energy & Nuclear US gas supply prediction hits 108 bcf/d; TerraPower’s Wyoming construction permit keeps the Gen IV nuclear call on track, while $4.50-5 natural gas and China oil demand growth both stall out.[00:16:21] Predictions Review: Tech, Robotaxis & Quantum Risk to Bitcoin Tesla Robotaxi needs a serious hockey stick to catch Waymo’s ride volume; new Google research shrinks the qubit count needed to crack Bitcoin encryption, pulling forward the threat timeline.[00:21:43] Predictions Review: Healthcare, Pharma M&A & GLP-1s 2026 pharma M&A tracks to a record ~$150B first half; Vertex pays ~$10B for endocrine-disorder specialist Kynetix, and a new Medicare GLP-1 bridge program offers $50/month prescriptions through year-end.[00:30:06] Wrap-Up Hunt and the team close out the predictions review largely unscathed.Get the full Cash Flow Memo with updated financials on ~80 companies at telltales.us — new episodes every week. Track how our calls are actually playing out at our predictions scorecard.Cashtags$AAPL $AMZN $GOOGL $LLY $MSFT $MU $NVDA $PLTR $TSLA $TSM $VRTX This post and the information herein are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com

Transcribe →

Weekend Update - W2627

4w ago00:13:05Tap to summarize▶ Explore this week’s Tape — live, sortable, drill-down →Microsoft Is Funding the Next AI Layer With the Last OneEnterprise AI stopped being a story about models this week and became a story about invoices. On July second, Microsoft — page one of the Cash Flow Memo — stood up a unit called Frontier Co.: two and a half billion dollars, six thousand people, one job, which is to take AI products the last mile into enterprise deployment.¹ Two days later it moved to cut up to five thousand roles from sales, consulting, and Xbox.² The new layer is being paid for with the headcount of the old one. That is not a hiring plan. It is a company rebuilding itself around the part of AI that actually sends a bill.The model layer got three years of narrative. The deployment layer — the boring work of installing the thing, retraining the seat, wiring it into the workflow — is where the money changes hands, and the market has not repriced for that yet. Microsoft just showed you how the transition lands in a real profit-and-loss statement before it lands in a revenue line: deployment headcount up, legacy headcount down, net headcount roughly flat, and the revenue you are supposedly buying still not visible. The screens know how to price a growth story. They do not know how to price a margin-mix reallocation that hasn’t reached the top line.We have watched Microsoft run this exact play once before. The last decade’s version was the move from packaged software to subscription — the company retooled its sales motion and its cost base around the cloud years ahead of the recurring revenue, wore an ex-growth multiple through the gap, and re-rated hard only once the ARR became legible. Frontier Co. is the same bet, one rung up the stack. The reorg comes first. The revenue is the lagging indicator. The interval between them is exactly where a name gets mispriced.The pricing tells landed the same week, on both ends of the stack. Microsoft made the Copilot Business seat a permanent product at twenty-one dollars a month³ — the output price, now fixed. And AWS, per a Yahoo Finance report, raised GPU instance prices about twenty percent on July first⁴ — the input price, moving up. Read those two together and you are watching enterprise-AI unit economics get discovered in real time: the cost of compute rising, the price of the seat set. The names that compound from here are the ones that can lift the output price faster than the input cost climbs. Microsoft, sitting on the seat, can. Most of the memo, buying the compute, cannot.One honest caveat on the input side, because it is doing a lot of work: the AWS move is one vendor’s list price on specific instances. Azure and Google have not publicly matched, and a list price is not what a committed customer actually pays. Whether it holds through the next wave of capacity — the sixty-five-to-seventy-five-billion-dollars-per-gigawatt data-center builds Hunt, Jason, and Mike walked through on Wednesday⁵ — is the tell for whether this is structural scarcity or a headline. Don’t let one instance-price line stand in for the whole compute market.The cashflow read is in Marcus’s column below — short version, Microsoft is paying about thirty-eight times trailing free cash flow⁶ for a deployment curve that isn’t in the numbers yet, on capex already running close to a hundred billion a year.⁷ Palantir, the pure-play version of the same government-and-enterprise bet, asks a hundred and eight.⁸What changes the read is retention, not growth. The test on the next print, due late this month, is whether Copilot seat retention and attach start to show up inside Microsoft Cloud growth before the capex compounds past them. If deployment headcount grows and the seats don’t stick, that is the tell that enterprises are buying the org, not the outcome — and the whole bet inverts. Watch the AWS price too: if Azure and Google haven’t matched within a quarter, the twenty-percent move was a one-vendor list-price event, not the scarcity signal it read as. Mark the calendar for both.Wall Street’s consensus on enterprise AI: show us the revenue, then we’ll pay for it. But the org charts and the price tags moved this week, and the revenue line always arrives last. The last time Microsoft reorganized ahead of its own revenue, the people who waited for the number paid up for the wait.The Tape — W2627Universe of 94 cashflow-memo names, snap dates 2026-07-02 → 2026-07-03. Composite is rank-sum percentile of FCF Yield + NTM Revenue Growth (higher = better balance). Banks and finance-book names shown separately.Telltales Yield — Top 10From the Cashflow Desk — Marcus GrahamThe enterprise-AI trade got expensive this week, and the cheapest way to own it is sitting at number four on the board. Salesforce already licenses a seat inside nearly every enterprise now buying AI deployment — and the memo has it at 10.5x trailing free cash flow, a 9.5% FCF yield, against single-digit NTM growth. Palantir asks ~108x for a version of the same government-and-enterprise AI story. That gap is either the market correctly pricing Salesforce as ex-growth, or an unpriced option on Agentforce turning installed seats into AI attach. The table can’t tell you which. The test on the next print is whether agent adoption shows up in current RPO and net seat expansion — or whether single-digit growth is the new ceiling.Telltales Yield — Bottom 10This Week’s ReportersNo universe names reporting in the coming 7 days.Sector MediansDebt / FCF Watch (highest leverage on TTM FCF)Weekly Price MovementTop 5 (week-over-week price) Bottom 5 (week-over-week price) Banks (shown separately — FCF metric not meaningful)Finance-book — FCF not comparableCustomer-float / captive-finance / reserve businesses (IBKR broker float, KMX CarMax Auto Finance, PYPL customer funds, CRCL stablecoin reserves). The memo’s operating-FCF method overstates their FCF, so they are held off the ranked leaderboard pending the P&L-waterfall rebuild. Data Gaps91 of 91 ranked-eligible names ranked. 0 dropped for missing FCF yield or NTM revenue growth; 7 shown separately (banks + finance-book, FCF not comparable).Source: cashflow-memo master_2026-07-03.csv. NTM growth from analyst-estimates consensus. Composite is a percentile rank, not a recommendation.The Issue — This Week's BriefThe Cashflow MemoW2627 — Tesla Blew Past Delivery Estimates, Comcast Split Itself into Cash, and Enterprise AI Started Setting PricesTesla blew past delivery estimates, Comcast split itself into cash, and enterprise AI started setting prices.The Telltales Weekend Update. Ava Cabot and analyst Marcus Graham walk through what happened this week — and what’s coming next — across the companies in the Cash Flow Memo. About 14 minutes. No filler.Download the memo at telltales.us. Hunt, Jason, and Mike are back Wednesday on episode E2628.Chapter markers* Time | Segment* 0:00 | Opening disclaimer* 0:15 | Cold open — throughline + prior-Wed callback* 0:45 | Theme — AI Goes to Work (Microsoft, Palantir)* 4:45 | Deep dive — Two Multiples (Tesla, Comcast)* 8:45 | Rapid-fire (Walmart, Harrow, Eli Lilly)* 11:45 | Close — Consensus Watch + earnings season preview* 12:30 | Closing disclaimerFull transcriptOpening disclaimerAva: The following conversation is intended for informational purposes only. You should always do your own work to determine if an investment is suitable for you.Cold openAva: You’re listening to the Telltales Weekend Update. I’m Ava Cabot.Marcus: And I’m Marcus Graham — the cashflow desk.Ava: Quick note: the show is produced entirely with AI tools, and both voices you’re hearing are AI-generated. Send feedback through the Substack.Ava: Enterprise AI went from story to price action this week. Microsoft committed $2.5 billion and 6,000 employees to a dedicated AI implementation unit — and simultaneously flagged cuts to up to 5,000 more in legacy functions. Palantir won the U.S. Army’s data backbone contract for its highest-priority modernization program. And AWS quietly raised GPU instance prices 20% on July 1[^amzn-gpu-pricing-20260701] — the first open, on-record pricing signal that compute scarcity is structural, not cyclic. Meanwhile, two companies at opposite ends of the Cash Flow Memo’s valuation spectrum each delivered exactly what they promised. And the market’s reaction told you what it’s currently willing to pay for.Ava: On Wednesday, Hunt, Jason, and Mike worked through the cost of building the AI infrastructure itself — data center builds now running $65–75 billion per gigawatt, memory running at 30–40% of the total buildout cost[^ep-e2627]. This weekend, we pick up on the demand side: who is deploying that infrastructure, at what scale, and wha...

Transcribe →

Regulatory Capture Comes for the Labs

4w ago00:31:39Tap to summarizeMike, Hunt, and Jason run the exhibits fast, then dig into the AI buildout math that keeps getting worse, Oracle’s brutal week, and a healthcare block anchored by Lilly’s 340B fight. As always, download the Cashflow Memo at telltales.us.The Cashflow MemoKey Takeaways* Oil has settled into a ~$70 floor with backwardation nearly gone (~$3 now vs. the $90 near-month / $75 twelve-month spread at the Iran peak), and Hunt reads the Strait of Hormuz drone tit-for-tat as an indefinite status quo gated by cargo insurance, not Iranian intent, while Northeast heat firms nat gas as power prices spike toward 15c/kWh.* The White House is clearing Anthropic’s Fable-05 (announced today) while still restricting OpenAI’s latest, a few-weeks delay the hosts dismiss as trivial and as the regulatory capture the labs originally lobbied for, with no real risk of Chinese models leapfrogging on the pause.* AI data center cost has jumped to $65–75B per gigawatt (up from $30–50B earlier this year) with memory alone now 30–40% of the build per Gavin Baker, and a structural memory shortage (Micron plus the two Koreans running low capex) plus rumored TSMC price hikes leave no one immune and make the space-based data center thesis incrementally more compelling.* Oracle logged its worst week since 2001 on a bloated risk section and dependence on OpenAI’s questionable funding, but the bull case is replacement cost: contracted capacity is worth more than Oracle spent, so the levered buildout bet holds as long as a customer exists, not necessarily OpenAI.* Eli Lilly is pressing the 340B program (now 16% of US drug sales) by demanding hospitals prove need, with Bill Cassidy legislation this week codifying the fight, while Lantheus’s FDA setback was manufacturer-controls-only (not efficacy) and dovetails with the FDA’s new PreCheck pre-clearance pilot, and Vertex’s non-opioid painkiller is climbing a flatter S-curve than hoped.Show Notes[00:00] Welcome & The Cashflow Memo Mike opens with the week’s format across energy, technology, and healthcare.[00:25] Oil at $70: Hormuz & Collapsed Backwardation Hunt on the Strait of Hormuz status quo, backwardation collapsing to ~$3, and why cargo insurance sets the real ceiling on tanker traffic.[02:26] Gas, Heat & Power Prices The Northeast heat wave firming nat gas as stressed power markets spike toward 15c/kWh.[07:23] Russia-Ukraine Stalemate & Venezuela Refinery drone strikes and fuel shortages with muted oil impact, plus Venezuela’s earthquake and the Gulf Coast’s fit for heavy crude.[11:56] Washington Clears Anthropic’s Fable-05 The White House allows Fable-05 while restricting OpenAI; regulatory capture and why the delay barely matters.[14:22] Chinese Models, Sonnet 5 & Tiered Pricing Distillation, token efficiency, and Sonnet 5 as a two-generation-old model upgraded — tiered effort as a pricing strategy.[16:04] The $75B Gigawatt & the Memory Shortage Data center cost doubling to $65–75B/GW, memory at 30–40% of the build, and a shortage that capex can’t quickly fix.[16:50] Oracle’s Worst Week Since 2001 The oversized risk section, OpenAI dependence, and the replacement-cost bull case.[18:18] Data Centers in Space Why orbit starts to pencil out when labor and time are the only knobs left to turn.[21:15] Healthcare: Pfizer, Lantheus & FDA PreCheck Pfizer’s patent-cliff cheapness, Lantheus’s manufacturer-only FDA rejection, and the FDA’s new pre-clearance pilot.[23:53] BioNTech, Moderna & Vertex’s Slow S-Curve Cash positions, pipeline burn, and a flatter-than-hoped non-opioid painkiller adoption curve.[25:07] Eli Lilly and the 340B Fight 16% of US drug sales flow through 340B; Lilly demands proof of need as Cassidy legislation codifies the battle.[27:37] Harrow Litigation & Mid-Year Predictions Preview A December 7th jury trial over a compounded product, and a predictions scorecard coming next week.Subscribe for weekly cashflow-driven investing across energy, technology, and healthcare, and grab the memo at telltales.us.Cashtags$AMZN $BNTX $GOOGL $LLY $LNTH $MRNA $MU $ORCL $PFE $TSM $VRTX This post and the information herein are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit telltales.substack.com

Transcribe →

Weekend Update - W2626

Jun 2800:12:02Tap to summarize▶ Explore this week’s Tape — live, sortable, drill-down →The Week Memory Stopped Being a CommodityFor forty years, memory was the worst business in technology. Brutally cyclical, structurally commoditized, a graveyard of balance sheets that overbuilt into every upcycle and got buried in the glut that followed. You did not own memory. You rented it, for one cycle, and you got out before the supply caught up. This week Micron told you that business is over — and the people still pricing it as a cycle are fighting the last war.Start with the number that actually matters, and it is not the print. Yes, Micron guided next quarter to fifty billion dollars against a Street modeling forty-three, and yes, the market cap crossed a trillion.¹ Spikes like that are exactly what the cyclical bears are built to fade. The thing that should stop you is buried below the headline: sixteen legally binding take-or-pay contracts, locking in roughly a fifth of Micron’s DRAM capacity through the end of the decade.² Take-or-pay is the language of pipelines and LNG terminals, not chips. It is what a supplier signs when the buyer is more afraid of not having the product than of overpaying for it. That sentence has never been true about memory before.This is a capital-cycle story, and the cleanest analog is crude. The oil majors spent decades destroying their own returns by spending every dollar of cash flow drilling into the next price spike. Then, somewhere after 2015, the survivors consolidated and discovered discipline — capex restraint, returns over volume, supply that no longer rushed to kill every upcycle. The multiples did not re-rate because demand exploded. They re-rated because the industry stopped overbuilding. Memory now has three players who matter, AI demand that arrives on multi-year contracts instead of a consumer whim, and customers signing away their option to walk. That is not a cycle turning. That is a commodity becoming a toll road.And you can read the toll on everyone downstream. Apple raised prices on fourteen products this week and took its worst single day in over a year, with Tim Cook calling the memory spike a hundred-year flood unlike anything in his forty years.³ A company that prints a hundred-thirty billion in trailing free cash flow does not pass costs to the customer over a blip — it eats them. It passes them when the input is structural, and the same week it is quietly lobbying Washington to buy from a blacklisted Chinese supplier just to get the parts.⁴ Oracle is funding its AI cloud with a twenty-four-billion-dollar free-cash-flow deficit and forty billion more in planned debt, the whole build premised on memory it has to secure years out.⁵ Broadcom and OpenAI unveiled a chip designed to cut inference cost in half — which is what you do when the underlying components got expensive enough to engineer around. Every one of those moves is a payment, in a different currency, to the same toll booth.The cashflow read is in Marcus’s column below — short version: the Cash Flow Memo had Micron going into the print at a hundred-plus times trailing free cash flow, and it was the wrong frame, because the contracts changed what the denominator will look like.What changes the read is the supply side, and the calendar is short. The test is whether Samsung and SK Hynix hold the same discipline or break ranks and flood capacity into these prices — the move that has ended every prior memory upcycle. Watch the fiscal-2027 capex commitments from all three, and watch whether more take-or-pay contracts get signed or this stays a sixteen-deal anomaly. The thesis breaks the moment one of the three decides that share matters more than price. It always has before.Wall Street’s consensus on memory: enjoy the spike, the cycle always rolls over, it always has. Sixteen take-or-pay contracts running to 2030 say the cartel finally learned what the oil majors learned — that the most valuable thing you can do with a commodity is refuse to make too much of it.The Tape — W2626Universe of 94 cashflow-memo names, snap dates 2026-06-19 → 2026-06-27. Composite is rank-sum percentile of FCF Yield + NTM Revenue Growth (higher = better balance). Banks and finance-book names shown separately.Telltales Yield — Top 10From the Cashflow Desk — Marcus GrahamMicron isn’t in this table, and that’s the point — the print is too fresh and the fiscal-year filing hasn’t landed, so the memo number is already stale. Going into the quarter the memo had it at 102x trailing FCF, which was the wrong frame even then. The reframe is the contract book: 16 take-or-pay deals locking roughly a fifth of DRAM capacity through 2030. Take-or-pay converts a commodity denominator into something closer to contracted revenue, and the screens won’t reprice that until the filings show it. The test is the next fiscal-year filing — and whether Samsung and SK Hynix sign the same paper or break ranks on price.Telltales Yield — Bottom 10This Week’s ReportersSector MediansDebt / FCF Watch (highest leverage on TTM FCF)Weekly Price MovementTop 5 (week-over-week price) Bottom 5 (week-over-week price) Banks (shown separately — FCF metric not meaningful)Finance-book — FCF not comparableCustomer-float / captive-finance / reserve businesses (IBKR broker float, KMX CarMax Auto Finance, PYPL customer funds, CRCL stablecoin reserves). The memo’s operating-FCF method overstates their FCF, so they are held off the ranked leaderboard pending the P&L-waterfall rebuild. Data Gaps90 of 90 ranked-eligible names ranked. 0 dropped for missing FCF yield or NTM revenue growth; 7 shown separately (banks + finance-book, FCF not comparable).Source: cashflow-memo master_2026-06-27.csv. NTM growth from analyst-estimates consensus. Composite is a percentile rank, not a recommendation.The Issue — This Week's BriefThe Cashflow MemoMemory Hits Escape VelocityThe week the memory shortage stopped looking like a cycle, and everything downstream paid the bill.The Telltales Weekend Update. Ava Cabot and analyst Marcus Graham walk through what happened this week — and what’s coming next — across the 90-plus companies in the Cash Flow Memo. About 13 minutes. No filler. Download the memo at telltales.us. Hunt, Jason, and Mike are back Wednesday on episode E2627.Chapter markers* Time | Segment* 0:15 | Cold open — memory’s escape velocity* 0:45 | Theme — memory’s downstream: Apple and Oracle* 4:45 | Deep dive — Micron and Broadcom* 9:00 | Rapid-fire — Nike, pharma, Meta, Tesla* 12:15 | Close — Consensus Watch + forward weekFull transcriptCold openAva: You’re listening to the Telltales Weekend Update. I’m Ava Cabot.Marcus: And I’m Marcus Graham — the cashflow desk.Ava: Quick note: the show is produced entirely with AI tools, and both voices you’re hearing are AI-generated. Send feedback through the Substack. We’re still in pilot, so tell us what’s working and what isn’t.Ava: Here’s the one thing to take from this week. Memory hit escape velocity. And everything downstream — Apple’s price tags, Oracle’s balance sheet, the chips hyperscalers are now designing just to get out from under the cost — is a consequence of that one fact. On Wednesday’s show, episode 2626, Hunt, Jason, and Mike flagged the memory squeeze forcing Apple to raise prices.[^ep-e2626] Then Micron reported. And the squeeze stopped looking like a cycle and started looking like a supercycle.Theme — memory’s downstreamAva: Start where it hits you at the checkout. Apple just told you the memory shortage has reached the price tag. The company raised prices on 14 products this week — MacBooks up $200, the iPad up to $449, Vision Pro now $3,699.[^aapl-price-hikes-20260625] The stock had its worst day in over a year, down about 6%, roughly $265 billion of market value gone in a session.[^aapl-stock-decline-20260625] And Tim Cook didn’t hedge it. He told the Wall Street Journal memory and storage prices have quadrupled in three quarters, and called it, quote, a hundred-year flood, unlike anything he’s seen in over 40 years.[^aapl-cook-quote-20260625]Ava: And then the quiet part. The same week Apple raised your prices, it was lobbying the Trump administration for permission to buy memory from ChangXin — a Chinese maker that sits on the Pentagon’s blacklist.[^aapl-cxmt-lobby-20260627] That’s how short memory is. And the talent is chasing the same scarcity — Apple’s head of Vision Pro and smart-glasses engineering left this week for OpenAI’s hardware unit, after seven years on the project.[^aapl-meade-openai-20260626] Marcus — Apple can afford to eat this. Why is it passing it on?Marcus:...

Transcribe →