Loading summary

Transcript128 lines

- [00:00]

Anoop Malani

Foreign.

- [00:05]

Santi Ruiz

Hi, I'm Santi Ruiz and you're listening to Statecraft. Today I'm joined by Anoop Malani. He's a professor of law at the University of Chicago, but he's currently on leave, serving as the first chief economist at the Centers for Medicare and Medicaid Services. What that means is he oversees economic analysis for the agency that manages $2 trillion in annual healthcare spending. That's 23%, more or less, of the entire federal budget. The Centers for Medicare and Medicaid Services, or CMS. Medicare for 70 million elderly Americans, runs Medicaid for low income families and the health insurance exchanges where millions buy coverage. I wanted to talk to Anoop about the transition from academia into the federal government and to hear about what the day to day at CMS looks like. But I also wanted him to teach me a little bit about American healthcare policy. It's a field of policy I just know less about than some other topics.

- [01:01]

That we cover here.

- [01:02]

We talked about a couple, maybe pretty basic questions. For instance, the US spends like 20% of our GDP on health care. Why is our life expectancy so bad compared to half of Europe? We also spent a lot of time talking about fraud, specifically Medicare fraud. How do you crack down on it without hurting patients who really need care? And how do you stop incentivizing private insurers to make patients look sicker than they really are? We also talk about some other stuff. Skiing, committing fraud, or matching ACL injuries.

- [01:32]

It's a good time.

- [01:33]

As always, you can find a carefully annotated transcript for this conversation and for many others at www.statecraft.pub. if you liked this episode, leave us a rating on your podcast platform of choice.

- [01:46]

Okay, here we go. Anoop Malani, thank you for joining Statecraft.

- [01:50]

Anoop Malani

Thank you for having me.

- [01:51]

Santi Ruiz

It's good to chat. I realized in preparation for this conversation, I think I owe you and my dad an apology because I'm a UChicago alum. You taught there and I mean, you teach there, you're on leave. But I never took an econ class in undergrad at UChicago, despite being at, you know, one of the famous economic institutions. So this is my public acknowledgment to my dad and to you actually taking your class.

- [02:19]

Anoop Malani

Well, can I share a fundamental criticism of an institution that I love that.

- [02:23]

Santi Ruiz

Yes, yes. That's what we do here.

- [02:25]

Anoop Malani

Great. And I now have two children going to University of Chicago.

- [02:29]

Santi Ruiz

Really?

- [02:29]

Anoop Malani

Yeah. 18 year old that's about to start in the fall and a 20 year old that's going to start junior year. And they love UChicago. They love the culture, they love the intensity. But I have one major criticism, which is you have to take a common set of classes, sometimes called the Common Core or the Core. And there are two things that are not included in that Common Core that are just shocking to me. The first is you don't have to take an economic class. You don't have to learn about markets. The second thing is you don't have to learn about evolution. You can take them optionally, but it's not required. And to me, you know, if you think about two mechanisms that govern life that generally have a great deal of support, super important to understand it's those two. And yet we don't teach that.

- [03:13]

Santi Ruiz

So, yeah, it is funny. And I would have benefited from certainly the econ class. I just always put it off. I was like, yeah, no, I'll do that next year. Fun courses this semester or this quarter, really, I'll tackle it next year. I just never got around to it. So I think I've realized in practice a lot of what statecraft is, is like me doing remedial, you know, econ education. We had Dean Carlin on. He was chief economist at usaid. You're the chief economist at cms. So in practice, I think it's working out. I'm getting my education in markets, but it's taking a little while.

- [03:48]

Anoop Malani

That's great. Yeah. And by the way, there's an important intuition for economics, but I suspect that there is an overlapping, but not completely overlapping intuition for statecraft. So for those of us that are consumers of your podcast, it's not just you learning economics, it's us learning about new intuitions from you. So. So that's great.

- [04:05]

Santi Ruiz

I would hope so. But that's good to hear from you. But let me ask you. So like I said, we talked to Dean Carlin, who was chief economist, same title, at a very different institution, usaid, doing global development. You've spent some time thinking about and researching global development, but your role as chief economist at CMS is a very different role, very different set of econ questions. Let's start there. What are you doing all day as chief economist?

- [04:30]

Anoop Malani

Before I begin, let me explain. This is the first time there's been a chief economist at cms. So the very first thing I did is try to survey what other chief economists and other institutions have done, both in the government, outside of government, to try to see what are the sorts of activities they engage in and how they can be most Useful to their organizations. Okay. Having done that, I break down my job into three parts. The first part is to provide advice on prospective decisions. Sometimes there's writing involved, sometimes there's just conversations involved. Either case, there's some research that involves going to the literature or doing some back of the envelope numbers to kind of advise on immediate and pressing decisions. Okay, so prospective decision making, that's item one. Item two is projects. They are typically discrete projects where instead of just providing advice to the decision maker, I'm making most of the decisions. And maybe there's a kind of updating process that goes on. Right. I tell the administrator what it is that I'm doing, just check in to see if he's got feedback. But roughly, I'm managing the project entirely by myself. And often it involves improving economic decision making in different parts of the organization. Cms. That's the second item. The third item is economic research on questions that are both retrospective and prospective in the sense that, for example, we may have done a regulation or there may be a statute and we need to figure out what the impact of that is, or we want to just do some research to understand a topic that might have a decision forthcoming, but there's no concrete decision forthcoming. So trying to understand how, for example, marketplaces work or how MA is functioning or things like that. So that's the third. So the third item is general economic analysis, but not just for decisions.

- [06:19]

Santi Ruiz

When you did your survey of chief economists and other kinds of institutions in the government outside, I'm curious, what were your top line takeaways? What did you, before you went into the role? What did you think? Okay, it's going to be really valuable if I do X and I really need to avoid Y.

- [06:35]

Anoop Malani

So the main takeaway I got from talking to folks was that it's one of these jobs where there's no clear definition, so you have to make the job. And part of that is a conversation with the people that you're working with. Both the person that you report to, but also the people that you work in laterally with that are your colleagues. Try to understand what it is they do, how you can fit in, how you can be constructive. You want to add value without being disruptive. Okay, so that's the main takeaway that I got. The thing to try to do is to become a trusted advisor to the person that you, you report to. They hire you because of your qualifications, but that doesn't necessarily mean that you have trust on day one. Trust is something that you build up by doing a good job by getting the answers roughly right. But you're building up that trust capital, and you really need to do that. Because if you want your work to have import, it's got to be that the decision makers who take it as an input actually value it. Right. That it has leverage. The thing to avoid is to impose your own preferences. It's really important to understand that you bring in a set of tools. For me, it's economic analysis and understanding how healthcare markets work or how healthcare financing programs work. That doesn't give me the authority to displace people's preferences. They have different policy goals and I need to understand those goals and see how I can kind of apply this analysis to those goals. And part of that is also when you provide advice, if people don't follow your advice, and they will sometimes not follow your advice, you can't get angry about it because if you get angry about it, they'll stop asking. So the way to think about it is that you provide input when they ask and you let them make the decision. And that's kind of the best you can do unless they give you the decision making power.

- [08:28]

Santi Ruiz

Right. I'm curious for you, how has it been to go from an environment in academia where there's decisions being made all the time, but they're not these kinds of as weighty political decisions, decisions about reimbursement of healthcare insurance, of who is covered under what, to go from an academic environment to an environment where major decisions are being made and have to be made all the time under uncertainty. How has that changed doing economic analysis?

- [08:59]

Anoop Malani

Yeah, so you're exactly right. The main difference between academia and here is speed and the weight of decisions. Almost every day there's a decision that's important, that's being made. And in any given week or month, any decision that's being made is important, more important than almost any decision you'll ever make in academia. And of course, I'm speaking from CMS's perspective where almost all items, when you quantify them, end with a B for billions and not hundreds or thousands or even millions. Even when there are millions, there are three, usually three digits involved. So I think that that's really what's going on now. What does that mean for analysis? When you're an academic, especially if you're an academic economist, you do two things. You pick your questions and then you take your time to answer them to a certain standard of quality, usually whatever the bar is for getting into a very good journal. And in fact you will discard questions when you don't think you can answer them to that level of quality. That's not a privilege you have when you're working in a business or in the government. There you have to make the decision. And given that your goal is to say, what is the best analysis I can do in the time period allotted to make that decision? But you have to do the analysis. So that means sometimes you're going to do back of the envelope calculations, sometimes you're just gonna have to rely on theory. And so the broader point that I would make is you spend a lot more time, more than I anticipated, thinking about theory and letting theory guide you. So basic Econ 101 theory, to some extent, I would call it price theory because I'm from Chicago. And then you learn to do, you know, treat problems as Fermi problems. You just do back the envelope calculations as fast as you can. You pray that the literature's already answered the question. If not, you just gotta get what numbers you can quickly and answer the question before the decision has to be made.

- [10:47]

Santi Ruiz

And real quick, define CRM problems for me. I'm not familiar with that term.

- [10:51]

Anoop Malani

Fermi problems are problems where you don't have all the data that's available. You just need to get an approximate solution. And it's the art of coming up with solutions to questions.

- [11:00]

Santi Ruiz

Got it. What do economists who study healthcare get wrong? Or what do they do that's unhelpful for decision makers in policymaking on healthcare? Like, now that you're on this side of the aisle, what do you see about the academic side of the profession that you think could be improved?

- [11:20]

Anoop Malani

Yeah, I think you touched on a very important point, which is that there's a disconnect between health economics research and, let's call it American health economics research. I don't want to comment on different countries, but at least the health economics research that I engaged in, that my colleagues and good friends engage in, and the decisions that have to be made at cms. And the main difference is not understanding the constraints that decision makers face here. And there's a myriad of them. That's the first realization I had here. Beyond the complexity of the program. I realized that you can't just toggle switches on and off. You're really constrained. So let me give you a few examples. When you want to change a regulation, there's obviously a whole legal process set up by the Administrative Procedures act, notice and comment, things like that. But even outside that, when you want to make a change, you have internal clearances that you have to go through that add time on top of that, there's prudential concerns about making sure that you send the signal to the private sector so that they can prepare. You can't just pass a regulation and expect compliance right away. There's a lot of work on the private side to be able to comply, and you want to make sure that happens. And so today, if we want to make a decision, and we made the decision today, it might be two years, 18 months to two years before you can actually see the effectuation of that decision. So you got to make decisions way in advance, and that slows down a lot of things. A second issue that really comes up is just there are political constraints. Now, this is not unique to this administration, but you can't just make great policy decisions. You have to think about the coalition that is going to support your decision making and how your decision affects them because you exist in that coalition. That's a second one. A third one is just the resources for implementing things. I think economists, we just think, oh, let's change the premium schedule this way, or provide this little mechanism to provide incentive. And we don't think about, how do you implement that, how many humans do you need, what it do you need, what services do you need to have in place, what kind of education do you have to provide to the regulated party to understand exactly how to comply? That process is complicated and itself either may not exist or takes time to construct. And so I would say those are the three, at least. I can probably list more. But those are the top three categories of things that we have to think about. So you don't have a blank slate on which to rewrite. And I think that's the big constraint. And this, I imagine this affects regardless of which administration you work for, when people come in and they say, like, okay, oh, you should just change things to meet this particular, oh my gosh, you have to understand those constraints and you have to understand when an agency's inability to take an action is due to constraints versus not being proactive, something like that.

- [14:17]

Santi Ruiz

Right. That makes a lot of sense. And we spend a lot of time on this podcast talking about the challenges of implementation. So I'm always glad to hear another guest ding the bell. Things are hard to do in the real world.

- [14:30]

Anoop Malani

So there are two things that flow from this. Okay. For academic economists, including health economists, the first thing that flows from this is thinking about the questions that CMS needs answered or corporations need answered as opposed to what is economically interesting in the abstract. Okay. I think that would give research Much more leverage, much more impact on the world. It would increase the social impact of that research. The second is, and this is not confined to health economists, I think a lot more should focus on the what you would call statecraft or I would call implementation. We need to think about the economics of implementation. What is the value added by the apa? You know, how do we think about decision making in the context of political coalition? How do we think about what Eddie Lazear would call personnel economics in the context of policy decision making? I think there's a lot of work to be done there and one of the goals, I don't know if I'll achieve it. One of the goals is to try to bring health economists through CMS so they can see that firsthand. And then my hope is that will then inform their research when they are back in academia.

- [15:37]

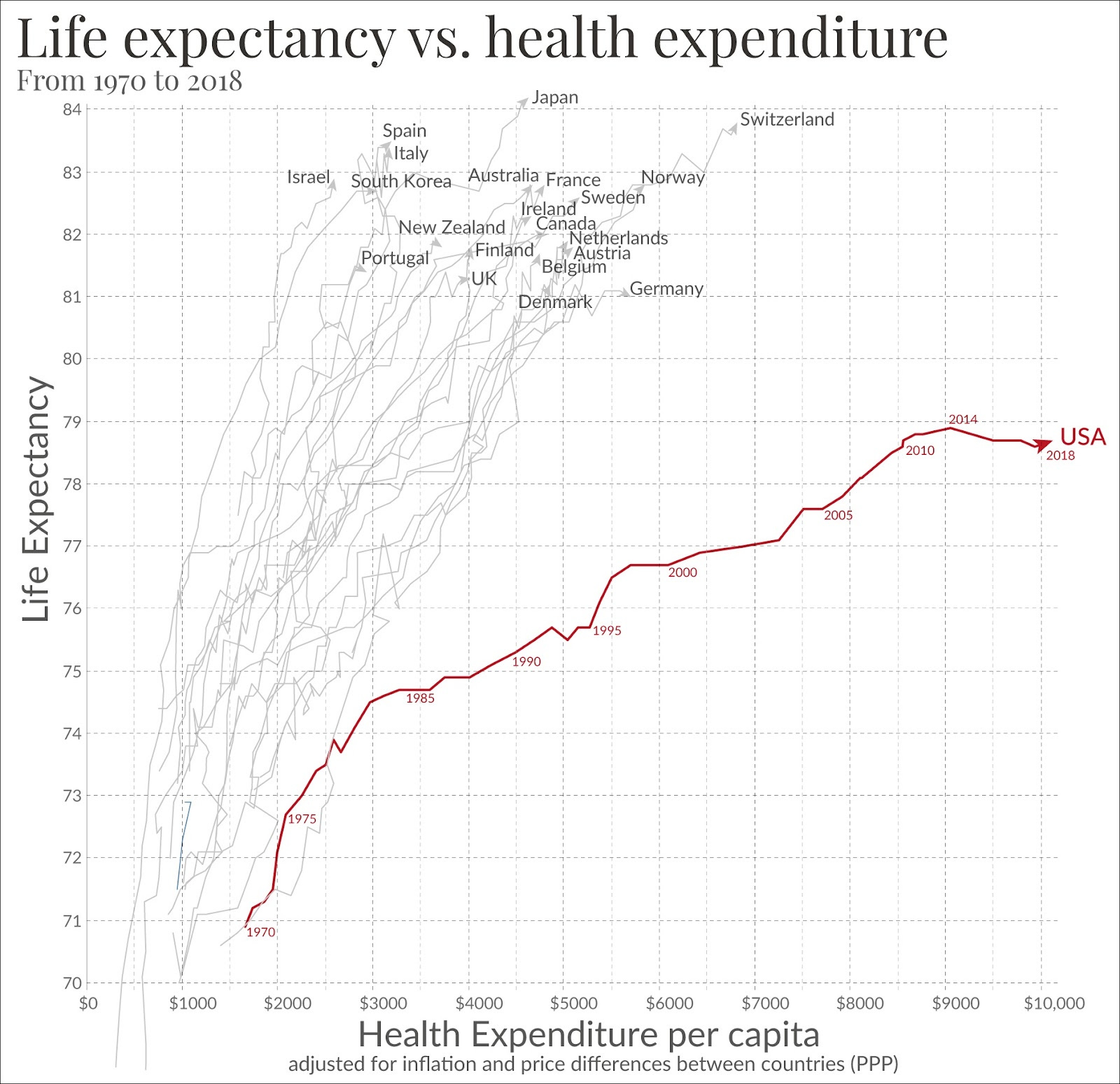

Santi Ruiz

That seems like it would be very valuable. Let me zoom out and ask you a very basic question that I think will be familiar to a lot of listeners. The US spends a lot of money on healthcare, quite a bit of money compared to many other developed countries. And we have worse life expectancy outcomes than that big bucket of other developed countries. They spend less money now. Some of their systems are socialized, some of them are not. As far as I understand, there's not one obvious thing that they're all doing that we're not that would lead to those discrepancies in life expectancy. So at a very high level, what's going on here that we spend more and die sooner?

- [16:15]

Anoop Malani

I'm going to put my academic hat on for a second before I talk. As chief economist at cms, I think I want to be a little bit careful about making those assertions. Although I probably share your view that we could be much more efficient about the delivery. That is to see do much better by both consumer and taxpayer in the delivery of healthcare. So let's revisit some of those things. The United states roughly spends 20% of GDP on healthcare. And I think for a long time we used to worry about that 20%. The exact number is going to be something like 18 or 19%. So I'm just going to round numbers to make it a little bit easier for listeners. Do they spend 20%? But an interesting puzzle for the last 10 years is that we've been stuck at 20%. And that's really remarkable because there are all these warnings back in the 1990s. We're increasing as a percentage of GDP our spending on health care and it's going to become unsustainable but then for a decade we plateaued and we're still trying to figure out why it is that we plateaued. And so I want to be a little bit careful about just that assertion. But on top of that, it's important to remember that there is no natural percentage of GDP that you'd spend on health care from a purely economic perspective.

- [17:23]

Santi Ruiz

Sure.

- [17:24]

Anoop Malani

Just depends on the degree to which health care is a normal good. And so if we think that it's a normal good, and by normal good, I mean that as you earn more, you spend a higher percentage of your income on that, and that's a, that's a normal good, or you spend more on that good. Now healthcare just might be a good where you, as you increase income, you just spend a higher percentage. It could be more valuable to higher income individuals for a variety of reasons. So I don't think that there should be a statement that this is too much.

- [17:53]

Santi Ruiz

Okay, well, let me, let me amend, because that's a useful correction. But acknowledging that we are a lot wealthier than, you know, we're wealthier than the uk we're wealthier than South Korea. These countries spend less on health care.

- [18:06]

Anoop Malani

Right.

- [18:07]

Santi Ruiz

This makes sense to me as a layman that we spend more on healthcare because we can, and my marginal dollar maybe should go to additional health care spending. But map that with the life expectancy point that we die a lot sooner, like several years sooner than the South Koreans or the Italians or the Swiss or the Germans.

- [18:26]

Anoop Malani

Yeah. So first, let me caveat what I said before. Just because there's no natural answer to whether or not you should spend 20% of your income on healthcare doesn't mean that that 20% isn't too much. It just means that just saying 20% is a lot doesn't prove anything. You have to give an additional reason why it might be too much or even too little.

- [18:47]

Santi Ruiz

Sure.

- [18:48]

Anoop Malani

Your second question is why do we get so little? And I would argue that that too is too quick a statement. Not that it's wrong, but it's too quick a statement when put that succinctly. And the reason why is twofold. The first is you have to understand the inputs into health in the United States versus other places. And if the inputs into health, meaning the underlying health, human capital of the population, is lower to start with, then, you know, it might not be that we're getting a bad result. It could just be that we're doing pretty good with a worse base. And if you don't mind a quick detour, I'M going to talk about a really nice paper that I think kind of addresses this. Sure. To me, kind of. This is my usual response when I talk to folks, when they say, hey, why, why does the US do so poorly on longevity measures? So this is a paper by Alice Chen, Heidi Williams and Emily Oster, my colleague Heidi Williams. Yeah, they're fantastic. And this is one of my favorite papers. It's actually kind of a descriptive paper, but super insightful. So what they look at, I'm going to try to be as precise as possible, but succinct. They look at why one year child mortality is higher in the US than in Europe. And it is higher, it's higher in the US than it is in Europe. And when they do their breakdown, a really important result that comes out is that the gaps that emerge in mortality rates don't emerge in the first month, they emerge in months two through 12. Why is that important? If you think about when the healthcare system where we're spending our money, when you think about where it's going to have the biggest impact, you think the first month and the first month, you don't see the differences. The differences show up when the healthcare system is not operating. It's in months two through 12. It's what's going on in the community back at home. And what that tells you is again, we may be starting with different baselines that our population might not have the same longevity in the abstract or they may engage in other behaviors that lead to outcomes being worse, longevity being worse. And so I think we want to take that into account. That's great paper. You should read the paper also. All three are great researchers, always fun to read. But that's an important takeaway is that health is not the same thing as healthcare. And when we want to figure out if our healthcare is doing a bad job, we need to actually look at places where healthcare is having an impact and not necessarily where just the community or families or activity differs.

- [21:10]

Santi Ruiz

Sure.

- [21:11]

Anoop Malani

The second point I would make that's really important here is I value health. I'm shocked there's a selection on what you do in life. But I understand that people make health health trade offs. So, you know, for a lot of my life I skied and skiing is a, it's not just a health health trade off, it's a health other happiness trade off. And we often trade our health for other things and we need to account for that. We can't just tell people you should always prioritize health. That kind of lecture doesn't Always work. We need to sometimes take people where they're standing.

- [21:45]

Santi Ruiz

Well, I don't want to pull you away from your core expertise and make you psychoanalyze the American public, but I guess I am curious. What's your reading then, if healthcare costs are not the only determinant of why. You know, just because we spend more on healthcare doesn't necessarily mean we should expect to live longer because we might start from a lower base. But what's your understanding of why Americans are starting from that lower base? Are we more risk tolerant, less risk averse than our friends in Europe and East Asia? We're skiing too much?

- [22:18]

Anoop Malani

No. You know, an earlier version of myself would say, never skiing enough.

- [22:22]

Santi Ruiz

You should always be more. I don't think I've hit that limit yet.

- [22:25]

Anoop Malani

That's a hard question, and honestly I don't know the answer. But we do have different populations. We have a different population mix. We have populations that are substantially transplanted. We are also geographically meaningfully different. We're much more spread out, we drive a lot more. Our production technologies are a little bit different than they are in Europe. And I think all those things are inputs into our morbidity and mortality doesn't necessarily make us worse off or better off. To get to those, you need to ask things like, what is your income? What is your consumption? I like consumption better than income. You ask about happiness, things like that. Whatever your flavor is, whatever preferred methodology you have. But I don't think I can understand that. But I would say the following. My input into health is not just medication. It's a whole range of things. And I just want to point out that this is what the secretary of HHS is talking about when he talks about make America healthy again. It's just that there are other inputs other than medicine and hospital care that affect your health. And we have to think about that as well. And I think that's probably true now. Can I define it? I'm not an expert in understanding how lifestyle specifically maps to health. That's not an area of research. There are people that do a great deal of research there, but I don't think anybody denies that there is an important relationship there.

- [23:44]

Santi Ruiz

Of course. Well, let me get back to an area of your core expertise, which is the econ problems of our healthcare delivery system. You and I have chatted before this call, and one of the things you brought up in those conversations was the fiscal constraints on the American healthcare system that exist just because of basic demographic change. I found that really informative when we chatted with love you to basically explain that again to me. What is the constraint broadly, demographically that the American healthcare system faces?

- [24:16]

Anoop Malani

Yeah, so I think most simply stated is that because our fertility rate is below replacement, it's currently at 1.6. Immigration helps sustain the population, but even immigrant fertility rates are declining and converging to the kind of long residing Americans fertility rate. You know, you get various estimates of when US population will peak. If you ask the un, it's going to be around when the world population peaks in 2080. But if you ask the CBO, you might get numbers that are as early as the2030s.

- [24:47]

Santi Ruiz

I tend to, just as a sidebar, I tend to believe the more pessimistic numbers. So we might, we might do a state graph on this in the future. You might know what's his name? Jesus Fernandez Gilverde, the demographer who thinks that, you know, has made a very cogent argument the UN numbers, you know, projections are way too optimistic. And I think I believe that.

- [25:05]

Anoop Malani

First, I agree with you. Second, I'm very excited to listen to that podcast. I think Jesus is fantastic. He and I don't have all the same views but are substantially aligned. I have some slightly heterodox views on where we're headed.

- [25:18]

Santi Ruiz

Let me put a pin in that and we'll have that conversation offline. But I would love to hear it.

- [25:22]

Anoop Malani

Yeah, that'd be great. I agree with you that the pessimistic numbers are probably correct. But let's think about how that cashes out. So what that means that our population, if your fertility rate is low, that means your population begins to age. And our population's already begun to age, but aging accelerates. And that has two impacts. The first impact is especially when you have a program like Medicare, you are going to have a greater demand for federal spending on healthcare. Healthcare for the elderly, because there's more elderly, there are more elderly. But the other problem is that at the same time there's greater demand for federal healthcare spending, there's also less supply of that healthcare spending because as your population ages, your working population declines and it's your working population that largely supplies tax revenue across a range of sources. And so that's our basic problem is an affordability problem. And the reason why this places general tension on this issue, even if we had stable finances, you would still face an issue between spend medical spending today and medical spending in the future. But now with demographic change, it's even more acute. And the way that you respond to that, you know, one approach which I Think is not the approach. That is, you know, something the American voter wants is just, hey, let's cut spending. That's one approach, cut benefit. But a second approach is to say, hey, before we think about any of that, can we make American healthcare more productive for each dollar spent? Can we give patients more value for every dollar that we spend? And if we can do that, we can make this program a little bit more sustainable despite that pressure.

- [27:02]

Santi Ruiz

Well, let's talk about that. And I should just flag again for listeners. CMS is, I mean, how to put this. It's like one of the huge cost centers in the federal government for good reason. It's the hub for most of, not all, but most of the government spending on healthcare. So almost 70 million people are enrolled in Medicare, about a trillion dollars a year, give or take or spent in that program. So that's like 14, 15% of total federal spending from last year. My understanding is like a little bit smaller percentage is spent on Medicaid per year. But taken together you've got like a third roughly of the federal spend runs in one way or another through cms. Is that, do I have that ballpark right before we move on?

- [27:50]

Anoop Malani

Yeah, I would say about 20, 23% of federal spend goes through Medicare, Medicaid or the exchanges. It is probably the, if you combine the three. So Medicare for the elderly, Medicaid for the poor. I'm simplifying. There's obviously disabled population, some crossover with duals, but Medicare for the elderly, Medicaid for the poor, and exchanges for the near poor. If you combine those three programs, you're talking about $2 trillion worth of spending. That's the biggest single ticket item that the federal government spends on. And that doesn't even include the 300 to 500 that the states spend. And it doesn't even include employer sponsored insurance where we directly, we don't directly fund it, but we provide tax expenditures by giving employers a tax break for providing that benefit and workers that a tax break for providing that service. And we don't control that. But health is super important and CMS is the largest expenditure. Yeah.

- [28:42]

Santi Ruiz

So right.

- [28:43]

Anoop Malani

Critical entity for understanding total federal spend.

- [28:47]

Santi Ruiz

Right. And by that same token, like you said, if you could improve the productivity of those marginal dollars, you get huge gains because there's just a huge amount of marginal dollars. There's one thing that we talked a lot about on this podcast over the last six or eight months has been doge and the doge push to cut waste, fraud and abuse. And I think there was a Lot of criticism of the kind of public messaging of DOGE in the early part of this year for spending a lot of time on things that were not finding ways to make healthcare spending more productive and less wasteful. Whatever listeners or whatever you think of the DOGE project itself, we don't have to get into that. But I think it's obvious the work that you guys are doing at CMS has a lot more to do with improving the productivity and efficiency of the government than almost anything else that one could be working on to reform in the federal government. So I'm just gonna. I'm not gonna make you respond to that, but I just wanna put a pin there. What levers does CMS have to tackle this problem? Just thinking institutionally, what tools could CMS have to try and improve the productivity of American healthcare?

- [29:59]

Anoop Malani

Okay, that is a very complicated question. And I think it's helpful to break it down by type of program. And really you need to think about three programs. Medicaid, Medicare and exchanges. Sure. And each of them have their own distinct challenges. And then there's going to be some challenges that are common across all. So if we think about Medicaid, one of the problems with Medicaid is that it's a program with peculiar incentives. The federal government pays for a majority of Medicaid, but states control how Medicaid is operated. Okay. And one implication of that is that states don't fully internalize the costs of their decisions. It's like going to a dinner and, you know, your friend tells you they're going to pay 60% of the check. You might order a little bit more than you need to. Right. Or you might not be careful in making sure that you're getting the best deal when you're choosing the restaurant. Right. So I think some of those issues arise just by the structural features of Medicaid. And Medicaid's an important program, don't get me wrong. But I think we could do a little bit better in making sure that there aren't efforts to either increase the federal share or to engage in inefficient payments, like state directed payments. So that's one way. And I think that has to do with the structural program. I'm going to turn to Medicare and then I'll do exchanges, because Medicare and Medicaid are the big ticket items, close to a trillion dollars of spending each year on each of those. So in Medicare, the real challenge is that Medicare is actually two programs that are combined. There's something called traditional Medicare where the government is the insurer, and they cover hospital care and they cover physician care. And after 2006, drugs, you get through Medicare Part D plans. But still, that's traditional Medicare. And then there's something called Medicare Advantage, which, you know, if you're old like I am, you'd call that Part C, but the young kids call it Medicare Advantage. And this is where the government is not the insurer. Instead, the government pays premiums to insurers, private insurers, who then provide, you know, hospital and physician and drug benefits, among other benefits. Okay, so it's really two programs. It's a public insurance program and a. You know, the government provides premiums for private insurance, and people can choose which of those to go into. And they're run differently. Meaning in traditional Medicare, where the government is the insurer, we just kind of set a whole range of prices, and it's fee for service, so providers just decide what to provide. And the history of traditional Medicare has been the government realizing that leads to too much expenditure. And so we try to pull back. So we go from cost plus pricing to prospective pay pricing to more recently, you have, under the Affordable Care act, you have something called Accountable Care organizations. And the first one was, we just pay whatever your costs are, plus. Then we say, oh, my gosh, that's too much. Are you charging too much? So we're going to pay per sickness, roughly, and we'll pay you a certain amount for sickness, and then you've got to manage. And that was still not controlling costs as well as we'd like. So then we switched to something called Accountable Care organizations. And there we said, the federal government's going to shift the risk associated with extra costs from the government to providers. Okay, Kind of like capitation, but not exactly. If you remember back in the 1990s, for those listeners that follow health insurance, that'll make sense. That'll have resonance. So that's, that's the issue there. The government as insurers trying to get the providers to behave efficiently in there. You know, you could imagine that the biggest gains that we could engage in are expanding accountable Care organizations and trying to get providers to be a little bit more careful with their spending. And there, that's the margin for improving cost or efficiency. I would say providing better care for customers without overcharging the government or without charging government for things that. That is not necessary or not a high return, but doing in a way that empowers the physicians. Right. Like, you also have to think about making sure that people participate in the program, but that's the balance that we're trying to do. Okay. Now, Medicare Advantage, which is the private plan thing there, we're not dealing with the providers directly, we're dealing with the plans, private insurance companies. And we have to incentivize them both to take on patients that are costly, but then to treat them well. Okay, Right. And there we want to make sure that we're getting a good assessment of how costly different patients are to make sure beneficiaries, I should say, to make sure that the insurance companies take them on. And there we're doing risk adjustment with the insurance. We're setting insurance prices and determining risk, which is different than what we're doing with the providers. So we can do better with risk adjustment in that regard and to keep down costs, again, without harming patients, in fact, maybe even making the patients better off, because we try to make those insurance companies a little better aligned with what the patients actually want, what the beneficiaries actually want. Exchanges look a lot like Medicare Advantage. We're paying a premium support. It's slightly different than in Medicare Advantage, but we're paying for people to get insurance through a private insurance company. And again, we want the insurance company to take on even high risk patients. And so we have to think about exactly how we do risk adjustment. Okay, Right. So those are the big issues. But then you can step back and say, okay, but is there anything that's common across all of these? Now, one thing that's common across all these is fraud, waste and abuse. Let's just look at the fraud component of that. That's the easiest when you charge for something that you shouldn't have charged for. Legally, that can happen in all these programs and we just need to be a little bit more proactive about it. You know, traditionally, I apologize for the wrong answer, but we've been thinking about this retrospectively. Usually what happens is, you know, Dr. Smith, not to pick on Dr. Smith in particular, but Dr. Smith, sorry, Dr. Smith builds for something that he or she didn't do, and that's fraud. Right. And we, what we do is if those billings became big enough that we'd notice, we then start a suit. You know, False Claims act suit, prosecuted by DOJ would take a few years. Maybe there'd be a settlement, maybe there'd be a payment, and maybe Dr. Smith be kicked out of the program. But that's a slow process. It doesn't capture everything. And importantly, the dollars already went up. Okay. And what we want to do is we want to switch to a program where we're doing it ex hand look at the data, we see patterns that suggest fraud. And before the dollars go out the door, we try to capture some of that and just ask, hey, Dr. Smith, did you actually do this? Things like that?

- [36:24]

Santi Ruiz

Terrible moment for Dr. Smith. Just really awful to get caught.

- [36:28]

Anoop Malani

Exactly. And so we want to, we want to try to engage. So our center for Program Integrity is working on projects like that to kind of do it a little bit earlier so the dollars aren't out the door. It we can cover more population in terms of protecting them against fraud and we have a better sense of exactly what we're doing. So beyond fraud, waste and abuse, there is also a, you know, going back to this idea that health is more than just healthcare, that your behavior and your lifestyle can affect what your health is. You know, at the secretary level, we're strongly thinking about how do we encourage people to engage in more healthy practices, whether it's exercise, better eating, those sorts of choices that are also inputs into health. But again, that don't directly involve federal spending right away. I think those are cross cutting across all the different programs. Sure.

- [37:17]

Santi Ruiz

Let me ask you to teach me a little bit more about this fraud question. I'm in the Medicare Advantage program. I come in to see you Dr. Smith, and Dr. Smith says, yeah, we think you have this set of conditions and it's maybe easy if I really do, it's hard to really tell, but I'm classified as a higher risk, sicker patient than maybe the facts would really firmly suggest. And Dr. Smith gets reimbursed at a higher rate. This has been a problem going back decades, as I understand. It's not, not necessarily a partisan coded issue. Medicare Advantage is a massive program. You could save a lot of money. You crack it on upcoating. And Dr. Oz, your boss in his confirmation hearings said there's a new sheriff in town, quote, on medical upcoding. And he firmly understands this is an issue and wants to crack down on it. How do you actually go about doing that without costing the patient?

- [38:14]

Anoop Malani

Okay, so let me address that in two parts. First is let me give you a simple definition of fraud. And then the second thing I'm going to do is talk about concrete changes you can make and address both fraud, but at the same time, keep in mind patient outcomes because you don't want to cut necessary care. So let's think about that definition. You know, one of the challenges with fraud is it's a whole litany of both federal and state rules, so statutes that govern fraud. It's very hard to teach because the rules do different things. And so to understand fraud, I think it'd be helpful to have a simpler definition that captures what all the different statutes are trying to do. And Jetson leader Louise and I have this paper that we wrote just before I started this job where we try to provide that. And here, here's our attempt at providing a simple definition. So fraud can be simply defined as when the following three items do not match. That is what the provider should have done for the patient given the contract with the payer, second, what the provider did for the patient, and third, what the provider told the payer the provider did. When any of those three things differ from the other two, that's fraud. Sure. So let me give you three simple or very common categories of fraud. Take upcoding. Upcoding is simply, you may have done the right thing for the patient according to contract, but you told the insurance company you did a little bit more. Okay, that's upcoding. Let's take the second most common class of fraud, which is medically unnecessary care. That's a situation where you told the payer that you were going to do what was appropriate, but you actually provided more care than is required and billed for that extra care, so you did too much. The third is the opposite of that, which is substandard care, where you're supposed to provide a certain high quality of care, and you did less than that, even though the contract required to provide the higher quality care, and you still billed for higher care even though you provided less care. And very often that happens when, you know, a doctor has somebody that's not qualified or a nurse or just a tech do the procedure that a doctor. That would be a classic example. And that's how you define fraud. Okay. And I think that that really helps when you use those three categories, because that captures almost everything. The only exception is something called kickbacks, which we can talk about if you'd like. Now, the second part of your question was, you know, what's going to be different? And I already kind of answered that question to some extent. Again, in the past, in general, we've been doing fraud enforcement after the. After it's occurred, after the money's out the door, and we usually use litigation tools to go after it. I think that an important thing that we are doing now is we're shifting towards a little bit more ex ante. Let's use the data that we get in the claims data to identify patterns that suggest fraud. For example, if there's a procedure that is supposed to take 30 minutes. And a doctor or a hospital or a specific provider is billing for that. And the billing practice suggests that the person worked 5,000 hours in a year, probably fraud. We should at least investigate that.

- [41:21]

Santi Ruiz

I'm having to do the math real quick in my head to think, how many hours do I work in a year? 5,000 is more than I do, right?

- [41:27]

Anoop Malani

Yeah, 100%. So typical full time is 2000.

- [41:29]

Santi Ruiz

Thank you. Good to know. Okay.

- [41:31]

Anoop Malani

And also, I'm not, I'm not sure I'd want a physician that's working two and a half full time jobs to do my procedure.

- [41:37]

Santi Ruiz

Surely not.

- [41:37]

Anoop Malani

And the thing is, that's a very simple example I gave you. But there are many other examples of situations where we'd agree probably this is not occurring, services are not being provided, or at least not provided to the level of quality we want. And so that gets back to the last part of the question. How do we make sure that when we cut spending we're not hurting the patient? Well, the first thing you can do is just try to figure out, is this provider actually possibly providing these services? Because if we really are inferring that he or she is not, then in fact the patient is not better off by that spending and in some case might be worse off if the person is like taking a 30 minute procedure and trying to do it in 10. The second thing that we can do is to set a high threshold. I mean, there's plenty of work to be done on the fraud side. And so if we say, look, if you bill for 5,000 hours in a year, you know, we're gonna, we're gonna go after you. But if you're billing for like 4,000 or 3,500, at least we'll look a little bit more before we decide that this is fraud. And so you can have a high threshold and graduate both, you know, the high threshold and the amount of scrutiny you get to make sure that the thing that doesn't happen is that the patient doesn't get care that he or she needs.

- [42:45]

Santi Ruiz

Sure. Let me ask you a more specific version of this. By revenue. UnitedHealth is the fourth largest company in the country.

- [42:52]

Anoop Malani

It's after Apple.

- [42:53]

Santi Ruiz

It's huge. About one in ten doctors work for it or are affiliated with it in some capacity. There's like a huge organization. There's been some good reporting, I believe, from Stat News about the practices that UnitedHealth engages in through bonuses and performance reviews that basically encourage clinicians to identify more health problems in patients, even if Those conditions are marginal or seem dubious. It's not totally clear. When in doubt, UnitedHealth has a set of incentives for clinicians to say this patient is a higher risk patient. What tools does CMS have at its disposal to crack down on it? Should it just ban that kind of incentive structure internally so that you don't get an extra bonus as a doctor for identifying more health problems in your patients? How should I think about this from the outside?

- [43:42]

Anoop Malani

Okay, two things real quick before I answer. The first one is I don't want to pick on United in particular. I'm not saying United is good or bad. That's not my job to do. And so I want to be a little bit careful that the answer I'm going to give you is unrelated to United States. That in any particular instance you'd actually want to see talk to someone who might be involved in a case or is actually an investigation.

- [44:02]

Santi Ruiz

But that's not me, of course. I'm just mentioning it as one who's been publicly reported. There's like a body of work. But I'm imagining this is a problem beyond any one individual insurance company.

- [44:11]

Anoop Malani

Yeah. So I'm going to answer the spirit of the question rather than that specific company, is what I'm saying. The second thing I want to say is I want to be a little bit careful and I think you, by the way, hit with this question on important topic, which is United as an insurance company, and it's not necessarily, although it has some vertically integrated segments that includes providers. So sometimes it's contracting with providers arm's length and sometimes it's actually employer of the providers. And obviously when it's an employer, it can actually tell, maybe has a little bit more power to tell the provider exactly what to do. An ARM select contract, it has to do indirect incentives, things like that. But what you want to ask all the time is why United or a company like United, okay, so let's just call it. An insurance company might have an incentive to get a doctor to report more or less. Right. If the insurance company is acting on its own, at least in hindsight, within a plan year, it doesn't necessarily want the provider to exaggerate exactly what the claims are because it affects the bottom line. But if the insurer is being paid by the government, let's say the federal government, to provide insurance either through premium supports or an ma, the Medicare Advantage, the premium itself, it might, but the reason is because that premium might itself depend on how much care the individual is getting. So now we have to go Back and discuss risk adjustment and then think about how we answer that, how we make risk adjustment better. What is risk adjustment? Risk adjustment says, if you decided in Medicare the federal government was going to pay the exact same premium for every individual that chose to participate in Medicare Advantage. Insurance companies would have an incentive to try to find individuals who are low cost and healthy and cover those guys, but not cover those individuals who are high cost and not healthy. Especially if they couldn't charge any more than what the government was paying in premiums. That's called cream skimming.

- [46:03]

Santi Ruiz

Sorry, Cream skimming? Cream skimming, as in the really healthy guys and girls, we're gonna. We're gonna insure them.

- [46:11]

Anoop Malani

Exactly right. And the idea is, back in the day when we used to think that cream was good, we would skim the cream off. And that's the best part.

- [46:18]

Santi Ruiz

Some of us still do.

- [46:19]

Anoop Malani

Well, you know, for a lot of the rest of us, we're like, okay, we're gonna go with the skim milk, which has the cream taken out of it. But yes. So that's called cream skimming. You take the very best patients and you kind of keep them in your pool, and you try to avoid high risk patients. That way you can be more profitable. Now, we anticipate that the government does. And so what we do is we engage in risk adjustment. We try to estimate how much each individual will cost the insurance company and then pay the insurance company a premium that's proportional to that cost. And this should encourage insurance companies, in theory, to take on high cost patients and not just low cost patient, to eliminate creams. Now, devil's in the details. It depends on how well you do risk adjustment. If you do risk adjustment poorly, you might not solve the cream skimmer. However, sometimes you can make another error, and that is that you use a formula for determining risk that is manipulable by the insurance company.

- [47:19]

Santi Ruiz

Help me understand that. What would that look like?

- [47:21]

Anoop Malani

Okay, so let me give you an example from Medicare Advantage. So say I calculate your premiums or your risk based upon your past claims. So what claims did Santi file, that is to say, the insurance company file on behalf of Santi in previous years.

- [47:37]

Santi Ruiz

Okay, let's make it specific. I had a big ACL and meniscus surgery in the past year, and otherwise I've been very healthy. Let me give you that.

- [47:45]

Anoop Malani

Great. You and I are actually. We overlap in ailments or afflictions. I had an ACL reconstruction earlier this year.

- [47:52]

Santi Ruiz

Too much skiing?

- [47:53]

Anoop Malani

Too much? Uh, no, this was squash. My new current alternative. To skiing.

- [47:57]

Santi Ruiz

Okay.

- [47:58]

Anoop Malani

Um, but anyway, we take a look at your past knee surgery experience and all surgery experience, and we'd say, okay, well, that tells us, like, you know, if you've had this surgery, you're a more active person, but you're more likely to have this surgery again or have other afflictions with your knee. So you're higher risk. Okay, sure. Now, that's fine if that was the truth. But if an insurance company is likely to have you for multiple years, which is often the case for older patients who don't switch as much, and your older patients, you have a lot of afflictions that they can kind of attribute to you, where we would say, oh, yeah, that's probably likely to be the case.

- [48:31]

Santi Ruiz

Sure.

- [48:31]

Anoop Malani

What they could do is that this year, they could mark up your claims and say you claim for more than you actually did, or they might have you go through some diagnostic tests that even if they result in no positive proof of affliction, at least shows that there's a concern. So we can increase our claims this year. The insurance company can. And knowing that while they're on the hook this year, in future years, they'll get a higher premium from the federal government in ma Premium because they now view Santi as a more risky person. That's interesting. Right.

- [49:04]

Santi Ruiz

So just to get a little bit more color here, they might just push more diagnostics on me, even if I'm broadly healthy, because tell me if I'm getting this right, I'm generally healthy for an older guy. But there's these little risk signals. And if you do enough diagnostic tests, you'll find something that looks like a risk signal, and you can throw that in the mix.

- [49:24]

Anoop Malani

So the way to think about it is that your risk score is a function of your past claims. Okay. Or at least a bunch of different factors, including your past claims. And the insurance company that gets the benefit of a higher risk score, which is a higher premium, they might be able to manipulate the inputs into the risk score calculation. Okay, sure. So the challenge with risk adjustment is to do two things. One is to eliminate factors in calculation of risk that the insurance company can manipulate, or two, to increase the cost of manipulation for each of those factors. So the two kind of approaches that you can take. Now, the challenge is this is a game. This is a back and forth, right? Like, you know, once you. You set the risk score function up, the insurance company manipulates you, discover what they're doing to manipulate, then you close that loophole, and then they find another approach to manipulate and this goes back and forth. And what we need to do is we need to constantly play that game or we need to reduce the incentives of the insurance company to engage in that sort of behavior and that manipulation of risk. Course, sure. Okay, so those, those are the two approaches that you can take and those are kind of the changes that we'd like to see have happen going forward. But again, this gets back to again what we talked about at the very beginning of our conversation about capacity. You need to be able to do that quickly even though you've got this large entity that's managing many different programs and has some bureaucratic components to it. And so that's the challenge with risk adjustment. And you don't want to go too far by the way, because if you undercompensate insurance companies, like if you're too aggressive, you're going to get cream skin. So that's the balance that you need to play.

- [51:08]

Santi Ruiz

Well, let me ask one more question on this. This admin has finalized some rule changes and there's was working the Biden admin on this. There's been work in the Trump admin on this to try and tighten those rules so that risk adjustment is a little bit more locked down and that you don't get the same kinds of incentives for fraud on the margin that you might have now. At the same time, this admin is going to pay much higher reimbursement rates for Medicare Advantage to these private insurance companies than what the Biden admin proposed. So by one account, and again, I'll link all these in the show notes that should result in more than $25 billion in additional payments going to Medicare Advantage plans in 2026. Help me square that circle. We want to reimburse these private insurers more at the same time as we're cracking down on potential fraud in the system. How does that whole balance net out?

- [52:03]

Anoop Malani

Yeah, great question. Also gets at the complexity of the program. So let's answer this in parts. How do you address risk adjustment gaming even as you're increasing spending? And the way to kind of square that circle is to understand that it is possible that the composition of risk in the program in MA is increasing. @ the same time there's also inaccuracy in estimation of that risk. So imagine if, and I'm not saying this is true, I'm just going to give you a kind of a proof by counter example. But that illustrates how this could work. Okay, let's suppose that you're spending a dollar this year on average per person. And you know that the composition of the population is going to change such that the actual cost of that population is going to be $1.10. Okay? New people coming into the program from traditional Medicare. It could be new people coming into the program because they're aging into the program. It could be just underlying changes in the population, whatever it happens to be. Let's suppose that's the truth, okay? And now that's, on average, some people are going to cost a dollar, some people are going to cost $1.20. Some people are going to be in between. And the problem we face is not merely that the cost is rising. That's something that we just have to acknowledge and we have to pay for. But at the same time, it could be the case that some individuals who might cost A$5, their costs are exaggerated to $1.10 by the insurance company, okay? Through manipulation of claims so as to exaggerate their risk adjustment score. So what we want to do is we want to say, look, on the one hand, we definitely want to account for changes in actual costs for the program, but at the same time, we want to cut back on fake costs, exaggeration of risk scores. And so you can have both things happen at the same time. You just have to be careful about it. And I think that's what we're trying to do now. Can I use this as an opportunity to provide another lesson that's important?

- [54:03]

Santi Ruiz

Why not?

- [54:04]

Anoop Malani

So we already talked about one margin just a second ago, which is the program is not static. The population in the program is not static. That's changes. And one place where it changes is people going from traditional Medicare to Medicare Advantage. Medicare Advantage has a number of interesting properties, useful properties that make it an attractive program. So one thing that makes a very attractive program is that it allows for allocation of financial risk to both insurance companies and to providers, and to do that in a way that makes sure that both insurance companies and providers are giving patients the best care at appropriate prices. So in traditional Medicare, you do that through what's called accountable care organizations. I mentioned that earlier. You shift the risk just to providers, but you can imagine that there's going to be some times where you want to shift the risk to the insurer because the insurer knows a little bit more information. And sometimes you want to shift it to the provider. You can't do that in traditional Medicare, but you can do that in Medicare Advantage. You can shift it to the private insurance company who can then take a portion of that risk and shift it to provider and optimally allocate it in such a way to get the best deal for the patient and for the federal government. Okay, so that's one reason why you might prefer Medicare Advantage. Another reason that patients really like is that Medicare Advantage actually provides more coverage than traditional Medicare. So, for example, traditional Medicare is hospitals, physicians, drugs. But maybe you're going to get some additional care through a MA plan. Additional care benefits like vision and dental and things like that that patients value. Okay, so that might be another reason why you like Medicare Advantage. Anyway, there are a range of regions. One of the things that you might want to do is pull people into the MA plan if you think it's better for patients. Better quality, lower cost, both. So that's one thing that's important. And to keep in mind when we think about that cost estimate, that's an economic point. But here's an accounting point that's also very important. When you hear this number. So when you hear a number, something like we spend, we, meaning the federal government, spends a dollar ten. I'm going to make up that number because there's that dispute about what the right number are. But let's suppose that somebody asserts the government spends a. For every dollar spent on a traditional Medicare patient, the government spends A$10 on a Medicare Advantage. I'm not going to deny that that's actually true, but I want to put that in context so you understand that that doesn't necessarily imply that MA is inefficient or that it's not providing quality. And the reason is, I was going.

- [56:31]

Santi Ruiz

To ask you about this, so I'm glad you're bringing it up.

- [56:34]

Anoop Malani

Great. Yeah. Because, you know, it connects to this point that it looks like the government is spending more on ma. So when we think about how much is spent on the patient, we should think about all possible spending, meaning you should think about total costs of treating the patient in traditional Medicare and the total cost of treating the patient in Medicare Advantage. For simple comparisons. The problem is that the coverage of those costs varies. In traditional Medicare versus Medicare Advantage. In traditional Medicare, the government pays for part of the insurance. But there's a substantial amount of cost sharing that's involved in traditional Medicare. In Medicare Advantage, there's very little cost sharing. And it kind of maps onto, if you study health insurance, it kind of maps on this idea that, like when you have a fee for service program where you're going to pay for anything you want to, you could go to any physician, et cetera, usually to avoid excessive spending, you have a high coinsurance high deductible, high co pays, etc. To make sure that the patient at least sees part of that cost. And when you do some sort of managed care, whether it's a PPO or an HMO like what you might see in Medicare Advantage, you don't have very much cost sharing. Instead you have the provider that determines whether you can go or the plan determine can you go out of network, or you have the provider that has to get approval for, you know, give approval to go to a specialized physician, things like that. So those are the two different ways to control costs. But what that means is that in traditional Medicare, if you take total cost of a dollar, a higher percentage of it is paid by the patient and a smaller percentage is paid by the government. When you go to Medicare Advantage, higher percentage is paid by the federal government, a smaller percentage is paid by the patient. And so if you just compare the total dollar amounts, it could look bigger in Medicare Advantage simply because the government's accounting for a higher share. And that's why it's a bit of an apples to oranges comparison. You really need to think about which of these two programs are appropriate for each patient and then determine first whether or not we're spending that cost appropriately overall, regardless of who's actually paying the bill, and then second, filter that down to the actual dollars being sent out of the treasury to providers.

- [58:45]

Santi Ruiz

That makes sense. So we spent some time talking about tackling waste, fraud and abuse. I think like you, I agree there's a lot to be done there. But as you point out, a lot of the real meat or the real savings in healthcare comes from just bending the cost curve and just being able to deliver good healthcare for less. Can you talk a little bit about how tweaking what we reimburse and how we design those incentives can bend the cost curve? I know that's been a focus of yours.

- [59:16]

Anoop Malani

Yeah. So let's talk about the term bending the cost curve. That is roughly, I think broadly. People should think of that as if we hold the quantity and quality of care to patients constant, how can we make that care less costly? That's bending the cost curve. And bending the cost curve usually falls into two buckets. One is what economists might call a static bucket. Let's take the existing technologies that we have, treatments and therapies that we have, and just make sure we use them to bend the cost curve. Okay? Not invent anything new, not make any changes in how healthcare is provided from an innovation perspective. And then there's the dynamic bending of the cost curve, which is, how do we make sure that in a few years we have technologies that allow us to provide the same quality and quantity, but with lower cost. So when we talk about reimbursement policy, we're talking about existing technologies. So we're really talking about the static question, how do we reduce cost, holding quantity and quality constant? And there, I think what we're looking for is opportunities where a provider to take care of a patient is providing, you know, a particular therapy or diagnostic or other broadly categorized treatment that is more costly than another one that would be equally as good. Sometimes this goes under value based care, which is, are we paying for care that is paying an amount that's more than the value from that care? An example of this might be a rule that we recently had on site neutrality, which is a rule that says, currently it is the case that for certain procedures, the amount that we pay for it varies depending on where that procedure was done. We might pay more in a hospital setting than in a more outpatient setting. Things like that.

- [61:06]

Santi Ruiz

And real quick, why is that the status quo? Like what? In layman's terms, why is it that Medicare says, yeah, we'll pay you more for the exact same service because you perform the service in a inpatient or in a hospital or an outpatient facility.

- [61:21]

Anoop Malani

So there are sometimes legitimate arguments for why you want to pay more in a certain setting. So, for example, take an emergency department. An emergency department often costs more because it is a very capital intensive department. It allows for a lot of contingencies. If something in that procedure goes wrong, the emergency department has the equipment and personnel right there to immediately take care of it. Okay? So for example, if you go in and you have a gunshot wound, makes sense to do an emergency department, because who knows what's going on inside your body that could have been affected by the gunshot wound. But if you've got a toothache and you go to the emergency department, that doesn't make a lot of sense. So we've got to extract a wisdom tooth or something like you don't need all that extra equipment. It's a very, you know, straightforward procedure. Not that it's painless, but it's a straightforward procedure. We know what we need. There's not a lot of contingencies. So it wouldn't be appropriate to pay more to do it at the emergency room and then pay more for it. And so what ends up happening is that there are going to be some situations where we do want to pay more because we'd rather have the procedure done in a, in an environment where it is more costly to do. But there's going to be a lot of things for which we don't need that and we need to move for those procedures. We need to move reimbursements to encourage, for example, the wisdom teeth extraction to be done on an outpatient basis. And obviously I'm giving very peculiar examples, but that's for purposes of illustration.

- [62:38]

Santi Ruiz

Sure.

- [62:38]

Anoop Malani

And so site neutrality rules basically says for a given procedure you're going to pay the same amount regardless of where it is conducted. And you do that for procedures where it should be done, especially for procedures where it should be done in a more low intensity setting. And that then encourages the provider to do it at the low intensity setting where it's appropriate, something like that. And that's the purpose of those rules. So there's a good reason for why you would do it in some procedures, pay more for certain sites, but for others you don't. And for those others you want to have a kind of a site neutrality rule to encourage the provision of that care in a more efficient setting. And by the way, just as good for the patient. And so that's the basic idea. But again, more broadly, if we step back, we're saying, okay, we want to bend the cost curve in a static sense. Given existing technologies, are we using those technologies in the best possible way? What I mean by that is, for a given level of quality and quantity, are you able to provide that care at a lower cost?

- [63:41]

Santi Ruiz

Sure. Let me ask you about another example of trying to bend the cost curve and don't want to make you spend too much time on it. But I'm thinking about all these prescription drug price pushes in American politics. And you've seen them from this administration, we've seen them all across the board. Everybody wants prescription drugs to cost less. There's like a bipartisan interest in bringing down drug prices. Counterpoint, of course, is that if you reduce drug prices mechanically, you reduce the revenues of the companies that develop those drugs. And in the future, maybe you get fewer of those drugs because companies are less incentivized to develop them. So you get cheaper prices today for drugs and maybe fewer really valuable medical innovations tomorrow. This admin has talked about trying to reduce prescription drug prices. Are there ways, other ways to incentivize biotech companies to invest in R and D if you do bring down those prices? If you do say like, hey, we're going to pay a lot less for.

- [64:41]

Anoop Malani

Ozempic, say, yeah, I think you highlighted the kind of trade Offs that are involved. But I want to add two complications that make it so that it's not always the case that when you lower drug prices, that is to say, the amount the payer pays drug companies for prices, that you get less innovation.

- [65:00]

Santi Ruiz

As a side note, this is the problem with you economists is you're always introducing complications to my toy models. And that question, it's very frustrating.

- [65:07]

Anoop Malani

Well, my retort is that it's reality that does the complications. All we're doing is providing a map to this reality.

- [65:13]

Santi Ruiz

Just explicating. Okay?

- [65:16]

Anoop Malani

Just explicating. That's it. We're. We're just neutral bystanders. So let me offer two. Two complications. The first complication is a really simple one, which is that the modern drug market is not like your traditional drug market, which fits that model that you have in your head. The modern drug market has intermediaries involved. And intermediaries can be PBMs, they can be wholesalers, et cetera, PBMs, pharmacy benefit managers.

- [65:42]

Santi Ruiz

Right, very. Okay. As I understand, just middlemen in this process.

- [65:45]

Anoop Malani

Right. But let me take a step back for a second. Okay. Because I think that, you know, a lot of time, if I were a listener, I would look at this and say, why is the system so complicated? Like, why can't we do things simple? And the usual answer is, as it turns out, each of these changes addressed an old problem that we've now forgotten about. And so if we just come along without knowing that old problem, it looks like the new system is just like this, you know, ball of. Of yarn that is so knotted up you can't possibly understand why it ever got here. So let's just pause for a second to talk about PBMs, and then talk about the problems with PBMs, and then I'll connect it back to exactly what you said. Okay, so imagine you're a payer and you have to. You. You're going to COVID patients at local hospitals. That's perfectly fine. You negotiate with those local hospitals, your deals, but you also have to cover drugs. Now, the problem is that the drug companies are located around the world. There's a lot of drug companies, and you need to negotiate with them to make sure that your patients, your beneficiaries, get access to a portfolio of drugs that are useful. Right. That a health insurance plan would cover. You can negotiate with them, but, you know, as it turns out, there's a lot of them. In addition, it's the case that other insurance companies also have to negotiate with the same people, same drug Companies to kind of get contracts on coverage. So these entities called pharmacy benefit managers emerge and they both negotiate on behalf of insurers with the many drug companies. But they also then help the drug companies a little bit further and help them figure out, here's the portfolio or formulary of drugs that you ought to cover. And that helps the insurance companies. Okay. By the way, this is not the only type of intermediary that exists like this. Hospitals have these, they're called GPOs. These are organizations, the purchasing organizations that help the hospital find gurneys and sutures and band aids and things like that. Right. They're just intermediaries that buy a bundle of things that you need. So this is a phenomenon that exists in a lot of places.

- [67:39]

Santi Ruiz

Yeah.

- [67:39]

Anoop Malani

Problem is that over time, PBMs, you don't need a lot of them to do the negotiation because the duplicate of negotiations, they ended up being a few small, very large PBMs. And as often happens in that sort of situation, there's a concern that those PBMs generate profits. Okay. Now, I'm not going to make a contention that there's excessive profits or things like that, but there's this concern that exists. And the important thing, for our purposes, that means that those PBMs which had a purpose may now be adding to the overall cost of drugs. And so that if you reduce the spending on drugs, you take a dollar out of that total spending, some of that dollar is going to come from the PBM which doesn't engage in R and D, instead of coming out of the pocket of the drug company which might engage in R and D. And that's the argument made for why it is that you don't. Whenever you cut prices, that doesn't translate immediately into a cut in R and D. That's the first complication that I want to highlight, which is why the simple Econ 101 model isn't exactly right. Good intuition, but a little bit different than reality. And let me provide another one even more important, I think so. What's really interesting with drugs and with many products is that once you do the innovation, you figure out, oh, this small molecule or this large molecule has some medical benefits and a tolerable safety profile. We should use it. You don't need to do that in a bunch of different countries. Once you've done the discovery, you can go sell in a bunch of different countries, sell in the U.S. sell in Europe, sell in Japan. You pick your area. And the prices that those countries pay in some sense is compensating. You for your R and D. So R and D is done in one place, but compensated by all these different countries. Okay, sure. And you could have a situation where the United States pays a very high rate of compensation, say 280% of what's paid elsewhere. And what that means is that the US Is shouldering a much higher share of the total R and D than other countries are other developed countries.

- [69:37]

Santi Ruiz

Sure.

- [69:38]

Anoop Malani

And so you might say, okay, wait, hold on a second. What if I decrease payment in the US By a dollar and increase it by a dollar in other countries? That is not decreasing R and D, it's shifting the R and D burden to the foreign market. And so when we have these discussions about sometimes called most favored nation pricing, sometimes called international reference pricing, it's partly about shifting the cost of that R and D and not so much reducing the R and D. And so now we have a second reason to think, okay, there's not an immediate translation between the changing the price in the United States and the R and D. It either could be because it's coming out of the middleman, or it could be because what we're doing is shifting some of that R and D burden abroad. And when we think about the arguments for and against these policies, we have to consider those alternative impacts.

- [70:28]

Santi Ruiz

Sure. But are there other levers that we can pull to incentivize biotech R and D?

- [70:33]

Anoop Malani

Right.

- [70:33]

Santi Ruiz