Loading summary

Transcript155 lines

- [00:11]

A

David Schleicher, welcome to Statecraft.

- [00:13]

B

Thanks so much for having me.

- [00:15]

A

I want to talk to you today about pensions, about federal bailouts of states, and I want to give you some context here. I think most listeners to this podcast, I think, are Gen X or younger. I think we've got some boomer listeners, God bless them, God bless you guys, and some Gen Xers. But I think, oh, I'm so the.

- [00:34]

B

Boomer is far away.

- [00:36]

A

Not you, not you. To be clear to the boomer listeners, I've got no generational warfare in my heart. Just descriptively, I think most listeners are younger than 40 for this podcast and most listeners are not in jobs that have pensions. I would hazard a guess. We don't have, like, an outsized number of firefighters and police officers and school teachers and civil servants. I guess we do have an outsized number of civil servants who listen to this podcast, but still certainly not a majority. So most of the people listening to this podcast, most weeks have zero personal experience dealing with pensions, rarely think about them, and they don't expect to. This is just my mental model of you, the listener. So I'm going to ask you, David, to really help us, people like me, more or less understand what's going on with state and local pensions and, frankly, why we should care. So let me start there. Like, why does it matter to somebody who's not a future pensioner how states and local governments run their pension systems?

- [01:38]

B

It's a form of government spending on labor, and therefore, to the extent that they spend a lot on it, they're not spending money on other things. And then further, to the extent that their pension systems are indebted, I'll get into what that means. That means that you're paying for services you received in the past. When we say a pension system is indebted, what it means is that people who paid for teachers in 1970 didn't save the money or pay them enough at the time, and that today we're paying not only for our school system today, but for our older school system. That means that we can invest less in today's school system because we still have to pay off the money we effectively borrowed when we employed people in the 70s and didn't save for their pensions. And so the question is just, it has an effect on budgets and it limits what jurisdictions can otherwise buy.

- [02:25]

A

Sure.

- [02:25]

B

So let me explain what a pension is. Right? So maybe that's the first place to start and a little bit of the history of state and local pensions. So a pension is just a form of deferred compensation. That is to say, when you work for the government or, or work for any employer, they can pay you your salary and then they can pay you something for retirement. And people who are used to a 401k or 401k match understand that they put some of their money in the company, might match your 401 and help you with retirement. Well, seeing local pensions are traditionally not contribution, but defined benefit. And that is to say that if you work for a certain amount of time, you get some kind of annuity that begins when you retire. And so you get a certain amount of money every year when you retire. And the idea is that either the employer or the employer and the employee, depending on the system, will save money while you work, and then they'll invest it and do some stuff with it, and then they'll have enough money when you retire to pay for this annuity every year for your retirement, to make something a defined benefit pension. Governments have always offered some kind of dependence. There are civil war pensions, there are all sorts of pensions. But the modern system of state and local pensions really takes off in the 1950s and 60s through the 70s. And a couple of things happen to make it different and notable. The first one is you see the rise of public employee unions who are asking for pensions, and that is a demand they make in negotiations. And so you start seeing bigger pensions offered. Second thing you see is a legal change. And so prior to this period, different by state, pensions were called in the law a mere gratuity the government offered them, but then could just not pay them if they wanted to. It was just. It was not a requirement to pay. And then states, through either constitutional amendments or through judicial decisions, gave pensions the status of either contract or property, but mostly contract. And what this meant was that they couldn't not pay them, that they had the same legal status as debt, and they were in fact protected by the state constitutions and the federal Constitution's contract clause. So they were not merely a choice to pay pensions, but. But it was a legal requirement going forward. And some states went further than this and adopted something called the California rule. The California rule says that not only is the part of pension you've already earned guaranteed by law, but any potential future earnings you have under your current pension policy are also guaranteed by law and can't be changed unless there's an offsetting benefit. So in a California rural state, which includes, unsurprisingly California, but also New York and Illinois and a bunch of other states, if you start Working as a teacher at, you know, age 24, your pension policy can't be changed until your retirement unless it's made better or there's some offsetting benefit. And what this meant was the combination of these two things meant that in effect, if you do not save money when someone's working, you've incurred debt. That to say that you have a legal requirement to pay in the future, but you didn't save the money in advance, and so you have some obligation to be turned. Just like borrowing. But the big difference in it and traditional borrowing is that normally when government, just like a person, borrows money, they're borrowing money to get an asset. You borrow money to buy a house. Well, governments usually borrow money to build a bridge or to whatever, something. And traditional debt is limited by debt limits. So state constitutions all have in them, they work slightly differently, but have limits or rules governing when debt is issued. Many people have voted in a debt election where they say there's a bond on the ballot, do we want to borrow $10 million to build a swimming pool or something like that? Pension debt, that is, say, if workers worked and you didn't save the money for the retirement, that you are legally required to pay for them isn't covered by these debt limits. And so one thing that happens for some jurisdictions, not all jurisdictions, but some jurisdictions is that it is a particularly attractive place to hide deficits. If you can't balance your budget this year, and you're legally required to balance your budget and you have legal requirements on debt, but you can't do it or don't want to do it, underfunding your pension system in one way or another is a way to bury your fiscal imbalances by borrowing effectively but not borrowing that is limited or regulated through debt limits.

- [06:38]

A

Let me just make sure I have that right. So I'm just a governor, my state legislature slashed taxes this year, or we promise some big new benefit for the state. And I'm having trouble making the math work, but kind of by default, the first place I go to try and fudge the numbers, make the accounting work, is typically the pensions.

- [06:58]

B

Yeah, you underfund your pensions and you can do it in all sorts of ways. The biggest way that jurisdictions have done this is they in their pension accounting say they're going to get a big return every year. We're going to get 8% returns every year. And they might, but they also might not.

- [07:13]

A

New York just did like 10 and a half percent.

- [07:17]

B

Sometimes it's good sometimes. But by guaranteeing that, because you're legally required to pay. What an economist would say is that you should assume the risk free rate of return. That is say like if you have an absolute legal obligation to pay something, you can't take risk that it's not going to be there. And so what you're supposed to account for is, is only those returns that you'd get if you invested in treasury bills or.

- [07:40]

A

The safest, right?

- [07:41]

B

Yeah, the safest. But that's not how any jurisdiction really works. So that is one way to hide things. But there are other things you can do too, to hide how indebted you are or just not sure, just get yourself more indebted.

- [07:52]

A

And then let's say that my state, you know, let's take Illinois because we're going to talk a lot about Illinois today.

- [07:58]

B

If we're going to pick on them, we could say New Jersey for now. They're also pretty bad. Sure.

- [08:01]

A

Okay, let's look at New Jersey, which is also has really poor, poorly funded pensions. Let's say it comes to the point where I just can't pay my debts, I don't have the money. What is the mechanical next step? Like I'm supposed to pay teachers who've just retired start paying their pensions and I just. That money does not exist. What literally, mechanically, practically happens next.

- [08:23]

B

So it's a great question. It's a little complicated though. Your example, you're a state, but for teachers, it will often be that you're a city or school district who's incurred that. Right. So it's sometimes the states assume the pensions. So we haven't had a state default since the 1930s, so it doesn't come up very often. And this is because states have extraordinary taxing powers, right. So they can raise the income taxes to very, very, very high rates if they want to. And that'll cause some exit and cause some problems. But what it means to not be able to pay is in fact a interesting question even for a big city like, so take Detroit. States can't file for bankruptcy. Cities can file for bankruptcy. Detroit did file for bankruptcy.

- [09:00]

A

Chapter nine.

- [09:01]

B

Under chapter nine.

- [09:01]

A

Yeah.

- [09:02]

B

But Detroit at the moment it filed for bankruptcy wasn't in fact enabled to make its next payment. Or at least it probably could have if it sold City hall and sold, you know, it just would have meant that it couldn't make its future payments. And so the legal requirement for bankruptcy is insolvency, and which is understood to mean not making your payments and not able to make future payments. But what that means requires like A it's not obvious. Courts. In the case of Detroit, this is actually a really interesting and really, like, weird idea created an idea called service delivery insolvency. And what this meant in the context of the trade they were first created for. Case in Stockton, California, was a rule that said, like, if your services get too bad, then we're not going to make you pay on your debts. And what too bad meant in this context is not clear because so, like, they note in the case, like, it takes an ambulance an hour to get to, you know, something like that. Right. Really bad. But like, if you're in the Upper Peninsula of Michigan and not inside the local government, who knows how long it takes an ambulance to get to. It might take three months, I don't know. It takes a long time.

- [10:06]

A

It's actually pretty hard to think of one metric that you could apply across every government jurisdiction and say, this is the number, this is the measure.

- [10:13]

B

And there's no positive rights in the state constitution. Education's a little different, but there's no positive right to level of policing services or something. And so courts are kind of figuring, and I've got a whole theory about what they're doing with that, which we can talk about in a minute. But what happens if you can't pay? Differs by jurisdiction quite a lot. So states have sovereign immunity, and that is to say you can't sue them in their own courts or federal courts unless they allow you to. They can't make them pay, but it could mean that there's limits in their ability to issue future debt. Or what happens when a state defaults. There are a number of historical examples, but mostly nothing except that they can't borrow going forward or they have trouble borrowing going forward for a long time with cities, they could be forced to pay, but then what happens? The state can authorize them to file for bankruptcy if they want to.

- [11:03]

A

Right. Just as an aside, I feel like in the last few interviews I've done, there have been all these phrases that come up where I realize that only people in the world that you and I both inhabit actually use them. So, like, service delivery is one that I hear all the time in policy wonk worlds to just mean things the government does, services the government provides. But it's a phrase that I've never heard service delivery in any other context.

- [11:27]

B

It's really good. No, it's true. But also service delivery, insolvency, it was a word a court just created out of cold cloth in the mid 2010s. It was just like it's not in the law. The law says insolvency, but in order to understand what insolvency means, they insert this wonk speak, which is not in the statute, just kind of made up. I think it serves a purpose, but it just kind of made up. There's a reason they did it, but it's. There's a wonk to law channel going through the judicial opinion.

- [11:53]

A

Yeah, it's funny because as you say, I hadn't thought about this until you mentioned it, but insolvency is really hard to define here. Like, you could sell off, you know, New York, let's say New York has some catastrophic financial crisis, can sell off huge amounts of property. It could, you know, reduce the number of cars on the streets by like 95%, is still, you know, doing policing, quote, unquote. But there's all these things, these toggles that you could just turn down and turn down and turn down because the city is hugely illiquid. It could kind of get rid of all these not really liquid assets before it actually ran out of things.

- [12:28]

B

And so this problem emerges in these cases and the courts are struggling with it and it's not obvious how to handle them. And we'll talk about my book in a bit. But what I think they're doing when they're doing this is like not best understood as like applying a legal test. They're saying, like, when are things so bad that we're going to allow you to use bankruptcy?

- [12:49]

A

Well, let's talk about your book. I just finished it before this conversation. In a bad state, responding to state and local budget crises. And for a book about state and local budget crises, it's remarkably engaging, as other people have said. I want to ask you to flesh out the. Basically, the introduction or the first chapter is this story that you tell of a world a couple years from now where Illinois and Chicago leadership, the governor and the mayor call this joint press conference and they say, everybody, we're bankrupt. We need the feds to step in and bail us out. The pensions are completely underfunded, teachers aren't getting paid, police aren't getting paid, municipal and civil servants aren't getting paid unless the feds step in. Draw out for me what would happen next.

- [13:38]

B

Well, so what would happen next is a great question. Hopefully it's a great question. It's the first chapter, first page of the book.

- [13:44]

A

It better be a good question.

- [13:45]

B

Before I answer the question, I'll tell you a quick, funny story, which is I was presenting the ideas in the book at Brookings Institution. And famously, it's very difficult to short municipal bonds, that is to say, to bet against municipal bonds. And my interviewer said, David Schleicher has achieved something amazing, which is that he has shorted municipal bonds. People said, how? Well, the books talks about Chicago's potential Chicago bankruptcy. If Chicago goes bankrupt, David's book sales will go up. And so it's a short of the music. So anyway, I thought it was funny. I thought it was funny.

- [14:14]

A

Anyway, I'm buying 50 copies.

- [14:16]

B

There you go. There you go. I love it. I love it. So the thing brings yet three possible federal responses. One, as you noted, is bailout. That is to say, and we've done it a number of times over the course of American history, where a jurisdiction is on the edge of bankruptcy and the federal government, or with respect to city of state government offers them a bunch of money. And this is probably the most famous single fiscal crisis in American history was the first major one that led to the assumption of state debts. Alexander Hamilton's assumption of state debts. For you musical theater fans, this shows up, but that was the states were on the edge of bankruptcy and the federal government assumed their debts, which was a form of bail. Another thing that could happen is the federal government could not bail them out, but either provide a legal mechanism or otherwise facilitate the people who've lent the money to eat the loss. So that is, say they could come up. This is bankruptcy. But there are other tools that do this as well. Well, that make it hard for people to recover against governments that they've led to.

- [15:17]

A

And the losers would just be the poor saps who thought it was a good idea to buy what to buy.

- [15:24]

B

Illinois bonds, or alternately to work for the state of Illinois and pay so that anyone who's a creditor in one way or another, and there are a lot of ways to make them the losers. And the third thing to do is to inflict, enforce those contracts very aggressively and also not offer bailouts. And the loser then would be the people. This jurisdiction would have to raise taxes and cut spending and sell everything. And maybe that won't be enough in the case of some small local governments, but Illinois has extraordinary taxing authority. But this would be very costly. So these things always happen during economic declines. And it would be a huge spending cut during a decline. In a decline, people have greater need for social welfare services, and you'd be cutting those. And so these three choices, bailout, austerity, or creditor loss are the three big options. And the federal government and state governments with respect to cities, have kind of toggled between them over the course of American history.

- [16:20]

A

And just to finish that set of three difficult choices, what's the problem with bailouts? Why can't we say, yep, we're going to bail you guys out every time?

- [16:29]

B

Ragged. The problem with bailouts is the problem of moral hazard. And so what is moral hazard? Well, the idea of moral hazard is that if we offer bailouts, everyone will get themselves into trouble so that they get bailouts. And this can operate through two channels. One channel, the traditional idea is that like governors will look around or legislature will look around and say, aha, they're getting a bailout. We should also be sid thrifts and not get a bailout. Now, the degree to which that channel happens is debated in the literature because it's like you're making predictions across time. So like, does anyone say, ah, you know, 40 years ago, New York state city got a bailout, therefore 40 years later I will get a license. But the other channel through which it works is through bond markets. So lenders can say, you know what, when push comes to shove, they always get a bailout. It doesn't require governors looking, it requires the lenders to do so. And there's a good bit of evidence that that channel actually works quite a lot. So one example I'll give is a bunch of states got into a lot of fiscal trouble in the 1830s and, and the lenders, in fact, Nicholas Biddle, who for you American history buffs, was the head of the second bank after the end of the second bank, goes to England, he's still the head of the U.S. bank of Pennsylvania and goes to London and says, look, you don't have to worry about your Pennsylvania bonds. The federal government always bails out states. And then they didn't, but, you know, oops, oops. But this problem, moral hazard works through this credit market quite a lot.

- [17:55]

A

Let me just go back to something you mentioned earlier, which is that it's really hard famously to short municipal bonds. Can you just dumb that down for me? Why can't I say, look, Chicago or Illinois, they're not going to pay these back eventually. Like, why can't I make money on that?

- [18:10]

B

So it's a great question. So there are what are called credit default swaps on some municipal bonds, state entity bonds, they're generally pretty thinly traded. And so you have credit default swaps on sovereign bonds. But an actual short. There are a lot of technical reasons why it doesn't work. I don't know how Detailed. You want me to go into. But broadly speaking, it has to do with the reason people like to hold municipal bonds, which is the tax exemption. So interest on municipal bonds is tax exempt, and that's the reason you hold them. And the changing hands would change who gained the income from them. And so it means that shorting is.

- [18:43]

A

Quite difficult because I'd pay a premium to short, basically.

- [18:46]

B

Yeah. Right. But the holder gets the. Who's getting the interest, gets the tax. That's the broad story. But, like, it's just not. Not a thing.

- [18:53]

A

Yeah.

- [18:53]

B

And so there's no mechanism. There are credit default swaps on some. They're generally pretty thinly traded. Also, also, I should say that the default rate in municipal bonds is extraordinarily low. And this is because there have been many historical instances where that's not true. So in the Great Depression, there was a huge number of defaults of municipal bonds. In the 1860s through 1890s, you just saw in what's called the railroad bond crisis, municipal bonds were defaulting left and right. The default rate is quite low on municipal bonds. It's in the 1%. The big spike involved Puerto Rican municipal bonds, but it's quite low. And so another reason these markets don't develop is because it seems pretty unlikely.

- [19:33]

A

Sure. Well, let me drill down a little bit on the Illinois and the Chicago example. This has been in the news recently, or at least it's been in headlines for those of us who have paying attention to Chicago pension fights.

- [19:47]

B

Yeah. So I would say this is a famous case. And I go. I don't mean it's Taylor Swift famous. You know, it's famous.

- [19:53]

A

Right. There are degrees.

- [19:54]

B

Yeah.

- [19:55]

A

But four stories about pension funds and funding ratios. This one is up. Exactly. Yeah, yeah. What are you doing if you're not paying attention? It's the Taylor and Travis news of the pension World. Let me just throw out some background facts here and then ask you to explain what's going on. So Chicago has four separate pension funds, and all of them are in variously dire shapes. So the Chicago Municipal, the regular civil servant pension system is one of the worst funded in the country. The Chicago Public Schools operate one of the most underfunded teacher pension plans. Cook county, the county Chicago is in, that pension system is terribly underfunded. And then Illinois, the state, has the worst funded state pension system in the country. No major US City has a worse credit rating than Chicago. It's got more pension debt than. This is crazy to me. It's got more pension debt than 43 US states. And just to kind of put all that in context, seven of the ten worst funded local pension systems in the nation are in Illinois. Like, let me just back up and ask you as a really broad question, how does something like that happen? How do you get into a state like that?

- [21:08]

B

It's a very hard question to answer, but it's a great question. So I'll take you back. But I'm going to take you back pretty far. So if you go Back to the 1970s, the big question was, why was Chicago so well run as a fiscal matter? So there's a wonderful book by a political scientist named Esther Fuchs called Mayors and Money. And the question is like, why did New York go bankrupt when Chicago didn't? And the answer she gives is that in New York, the political machine died. And the result was kind of no centralizing function in New York politics, just that they kind of gave money to everybody. Whereas in Chicago, the Daily Machine played the role because people were either for or against the Daily Machine. The Daily Machine had incentive not to go get in a lot of fiscal trouble, because if it did, it would be punished politically. Whereas in New York, you could pay off every little group, but there's no collective to punish. So that's Fuchs's basic story about why Chicago didn't want to use Daley. One of the ironies is that Chicago's fiscal troubles really get a lot worse when Daley's son is the mayor, but he's a much weaker political figure in a lot of ways and ends up spending more than they have across any number of dimensions. And pension debt is the biggest form of debt, but it's not the only form of debt. I mean, so famous. One of the other famous things that they did was that Daly sold off parking meter revenues to balance the budget.

- [22:29]

A

Infamously.

- [22:30]

B

Infamously. Yes, again, infamously. Taylor Swift. And I don't know. I don't know what the right thing is. It's like one of the variety of Taylor Swift rivals. Kim Kardashian, Kanye West. Right. I don't know.

- [22:41]

A

Of municipal deals.

- [22:42]

B

Of municipal deals. And that was just another selling off future revenues. It's not debt, but it's like debt in that. Right. You got the idea. And so Chicago has for many years, just not saved enough. Again, all it takes to have a pension crisis is to have budget deficits forever.

- [23:01]

A

Right. You don't need a crazy storm of events. You just don't pay as much in as you take out every year.

- [23:07]

B

In Chicago's case, they also offer rich Pensions. But to have a pension decreases, you don't need to have particularly expensive pensions. You just need to not save money for them. Right. And so the people think of pension debt and they think it's exclusively like a problem of the size of pensions. But some jurisdictions have very, very, very expensive pensions. New York State that has pretty well funded pension system because they have very high taxes and they pay for them every year. What Chicago did is it's basically not saved enough. If you run a deficit forever, you have a lot of debt. And unlike the federal government, they can't print money to solve their problems. And they don't have the taxing power. People can leave Chicago many. And so that's what makes it a real problem.

- [23:49]

A

So what is the problem for Chicago right now? Let's leave Illinois aside for a second right now. You know, Chicago is paying its teachers and its police and its civil servants their pensions. It actually just juiced the amount it's paying out to pensions. Chicago politicians proposed it and the state unanimously, the state General assembly unanimously said, sure, go ahead. But is this a problem now for Chicago? Describe the shape of the problem, because in some sense it's like it's not right now they pay out.

- [24:18]

B

Well, it is. Well, they pay out the teachers every year, but the increasing amount they have to or should pay on their pension squeezes, what they can pay on everything else. Right. So the harm to Chicago is that the amount of money they can pay for other things shrinks and shrinks every year. Now they can also just not pay that money, but eventually the piper has to get paid.

- [24:41]

A

And yeah, my understanding is that no other big city in America burns as big of a chunk of its budget on debt and pensions every year. That's around 40% of all the money that the city of Chicago spends every year is debt and pensions. And so you tighten and tighten the amount you can spend on everything else that the city may want to spend.

- [24:59]

B

And that's what it actually pays. Never mind what it should pay. Right. So what it should pay, if it's paying, what it should be to amortize the debt over time, it should be paying a lot more.

- [25:08]

A

Right.

- [25:08]

B

And so like you're really talking about all of the money, you know, in Chicago, in theory, they could, they could raise taxes, the state could authorize them to raise taxes. There are real limits at some point. Chicago already has quite high property taxes and sales taxes. And so Chicago voters turned down a. I thought it was pretty poorly conceived or poorly constructed property transfer tax recently that was designed to pay for an additional set of programs. But like there's just limits to how much people will pay in tax. And again you can make them, the state legislature can authorize it. But at some level you start to see real exit and you just start to see economic pain.

- [25:45]

A

And you have seen that in Chicago, especially compared to other really big cities that have contemplated raising taxes. You know, I tend to think, you know, flight from New York is more of a media thing than a reality. When you look at the data, you know, I think LA, CA, there is some, some exit. But Chicago has had real outflows of very rich people to all kinds of other places, been well documented.

- [26:09]

B

So I mean the studies on flight are really interesting. The studies in flight are about, usually about top end tax increases and personal tax increases. And the evidence is that there's very little bit of flight in response to respond. Now part of the challenge is that all these studies are pre Covid presume and like whether that changes things is a little unclear. And also one thing that's a little more complicated, this is like an aside from Chicago is the like social meaning. So like one thing is the tax rate going up 2%, another thing is like people you're not wanted. And those are two different types of stories. And I don't, again, I don't know what's going to happen with exit. The evidence on taxes and exit suggests it's not such a big deal. Corporate taxes can be different from that, by the way, but personal income is not a very big deal. But one of the challenges that emerges for these jurisdictions is first of all there's a lack of entry, which is a real problem.

- [26:58]

A

Oh, just no mega rich people are moving to Chicago. Right.

- [27:01]

B

I'm thinking about New York.

- [27:02]

A

We can lay off Chicago for one second.

- [27:04]

B

Yeah, but the like New York City's share of the richest 1% or something has declined over time. And a little bit of that is exit, but some of it is the absence of entrance. The second thing is that as we see greater income inequality, it means that like losing one person can be a really big deal. So there's a famous story involving a very rich person named David Tepper. He owns the Charlotte football, the Carolina Panthers. He left New Jersey and the legislature went into special session because his lost tax revenue was such a big deal. Interestingly enough, he moved back at some point during COVID which is kind of a fun, fun little detail. Anyway, all of this is to say that there's some level at which taxes cause exit and Chicago's seen a Lot of exit on the bottom end. New York, the issue is much more about housing costs than it is about taxes. Maybe about both.

- [27:51]

A

Sure.

- [27:51]

B

And in addition to the exit questions, it's just economically punishing to have higher taxes and worse services. Right. So like the result of if you actually try to pay back your pensions as opposed to getting a bailout or stiffing the investors, is a depressing politics for a long time where you're spending less and you are taxing more. And so, for instance, Connecticut was one of the worst, most underfunded pension Systems, but since the late 2010s has been extraordinarily responsible. And so the story is a much more complicated story about some budget controls that were put in and some bond covenants. And it's a very complicated. But they've saved a lot of money. But the result of this is like they're neither cutting taxes. They cut taxes a little bit last session, but not this session, and they're not raising spending. It's just kind of a downer. Another way of saying this is like you started thinking about generations. Like, it's the boomers that did it. So, like, why is politics so depressing in Connecticut? Well, the boomers did it. They spent all the money and were paying off their debts in Connecticut. And so that's the broad story. But Chicago might be much worse than that. It's more than just being like that. Something can be solved by making your politics a little bit of a downer for a couple of years.

- [28:53]

A

Well, I want to wail on Chicago some more, but before I do, just maybe give me like a, like a quick background or what other big cities or states are in a kind of comparable range. You mentioned New Jersey's got really underfunded pensions. Kentucky's got underfunded pensions. Like, what should we think of when we think big pension problems in American government?

- [29:16]

B

To start off with, pensions were much worse. They're in much better shape now as a general whole than they were 10 years ago. We've been discussing the pension crisis for a long time, and the last number of years have been quite good for state budgets. So they've been good for state.

- [29:31]

A

How much of that is Covid?

- [29:33]

B

So a good bit of it. So the state got a huge amount of money from the federal government, and while they spent a lot of it, they were not supposed to spend any of it saving for pensions. But they made their pension payments even most of the most spent their fronts. You saw the New Jersey would issue like press releases, like, we made our pension payment this month, which is this year, which is like press release, I paid my credit card. You're supposed to.

- [29:53]

A

Good for you.

- [29:53]

B

Yeah, good for you. Right. But state budgets are in pretty good health overall. And they were in bad shape before, but they're not getting worse in most places because state budgets have been in fine shape. So the desire to hide budget deficits has gone down. But in terms of the jurisdictions that are worthwhile, Illinois and Chicago are much, much worse than all other jobs jurisdictions. It's just much, much worse. There are ways bottom of the barrel. There are measurements you could use that you could see that Connecticut and New Jersey, there are measures that have them in bad shape. But the difference is that Connecticut and New Jersey are remarkably rich places. They're basically the richest places in the history of Christendom. And so their ability to bear the debt is a lot better. Illinois is a diverse state, a big diverse state. And Chicago, as you noted, the real problem, Chicago itself, the city of Chicago, has these unbelievably indebted pennies. Pension systems, like 18% funded, you know, pension system look really, really, really bad. But then they've got the school district and the complex relationship between those two entities in who's borrowing to help who is a real subject of a huge fight right now between the city and the head of the school system. But the overlaying the city, the school district, the parks district, the county, the transit district, the state leads to this kind of nesting dolls of Datsun. And from the perspective of a taxpayer, you have to pay out all of it. And this is something people don't often realize about jurisdictions, but like, especially if you're like a New Yorker or from San Francisco or something, most people, when they pay their property taxes, are paying to multiple jurisdictions at the same time. It's like an itemized list. In Illinois, you're frequently paying, people will pay taxes to 13 separate jurisdictions that are overlapping in complex ways.

- [31:31]

A

Right. To get more specific on Chicago situation, I'm still really curious about how something like this happens. So for kind of immediate context, there was a bill that just passed the Illinois General Assembly. Governor Pritzker just signed it a few Fridays ago. That boosts benefits for the city's first responders. And there's some complicated fights about getting them up to the same level as other people in the pension system. That was part of the motivation for this boost. But the cost is about $11 billion in pension liabilities. It deepens next year's projected deficit by more than $1 billion. It'll probably receive another credit rating downgrade for the city of Chicago. And it passed the Illinois State assembly unanimously. So I guess there's like a political question that I have for you, which is how does it happen that something that every, every accountant looks at and says, this is horrifying. This is just, you know, nobody, nobody's willing to stand up and say, like, yeah, I can see an argument for this fiscally. How does that pass unanimously? How do you get, like, everybody on board for that?

- [32:35]

B

Really good. So first of all, like, a little bit more detail on what actually happened might be interesting for your listeners. So the basic thing is that Illinois or in Chicago has what are called tiers of pensions. And this is driven by the fact that they can't change pensions policy for current workers at all when they want to cut pension spending going forward. And there's a great Supreme Court case where they tried to do, Illinois Supreme Court, where they tried to do this in the Illinois Supreme Court, said you can't, you can't change things for current workers at all. So they create these second tiers for workers. So now of tier 2, tier 3, tier 4. And the idea is that those workers will, who are doing the same job as previously hired workers will be earning pensions according to a different policy. And what this did was change the policy for one of those tiers of worker more like the other tiers of workers. What it did, we can talk about more, but if you're interested, but it made it sweeter. But remember, this is happening for police officers and firefighters. So the one side of this argument are scolds saying, this is going to.

- [33:29]

A

Cause people like me and.

- [33:31]

B

Yeah, right, right, exactly. This is going to be a problem in the future when you do this. You got to put your whole dinner. This is going to be a problem.

- [33:36]

A

In the scold voice on the future.

- [33:37]

B

You know, my bow tie is out of whack. And the other side of this argument is the extremely powerful moral claims of police officers and firefighters who've been putting their bodies at risk for you, the citizenry, the current level, current officials who. The problem which is accruing over time, but probably won't come to a head this year or next year or maybe not for 5 or 10 years or 15 years, face incentives where it's like, should I help out the firefighter today or should I think about the fiscal health of the state 10 years or 20 years from now and that.

- [34:14]

A

But when you put it that way, it's pretty obvious what I should do as a politician.

- [34:17]

B

Exactly right. And this Dynamic is exactly what the central problem. And one of the really interesting things about Illinois, there are millions of things about Illinois in this is that the Illinois legislature, when they were creating their California rule like constitution and they created the constitutional protection, had a debate about whether this exact dynamic would happen, whether jurisdictions would have incentive to under save. And what they said was, we're not going to put in a mandatory savings rule. What we're gonna do is make it legally protected and the legislature will never take risks if they have a legal requirement to pay in the future.

- [34:52]

A

Okay?

- [34:53]

B

But they were wrong. And that's what happened. You know, so they thought about it, they considered it, and they're like, ah, nah. And when this case came before, there were a whole bunch of pension cuts in the mid 2010s, both at the state and city level. And they tried to change the pension policies, the cost of living adjustments, and all these things for current workers and for retirees. And the court just said, the Constitution just says he can't do that. They had this debate and once you read the debate, it's like it seems 100% correct. Right? They thought about it, they imposed this constitutional limit and they said, legislature, you're going to have to follow the rules because you're going to have this outsized problem in the future if you don't. And then well, well and well. Right. And they'll.

- [35:37]

A

So this partially answered my question, but I still have this kind of maybe naive confusion. Like I get that it's hard to go against in this case the firefighters and the police and their unions, and it looks really bad, especially at a municipal level. If you're in Chicago itself, they're breathing down your necks. But if you're a state assemblyman from way out in some rural part of Illinois, I guess my question is like, why isn't there more incentive for you to be the brave truth teller saying, Chicago has been putting off its responsibilities for too long and I'm not going to put up with anymore, like, why is it unanimous? Is my question.

- [36:12]

B

It's a good question why it's unanimous. I think part of it is that you regularly see with respect to local legislation, we're called universal loggers, that if you're from Springfield, you don't want to get in the way of what Chicago wants, because if you do that, the Chicago representatives will get in the way of what you want for Springfield. When you want the change of policy, that state requires state approval. And that same dynamic also helps explain the budget problems at the city level. So, like why is it that the city officials who know that they're going to want money for a new park or a new whatever know that this is going to crowd out their ability to borrow in the future, you know, or spend money in the future. But the go along to get along politics and the particularly in the absence of sharp partisan competition can result in these universal log roles. This is kind of a point where Barry Guest famously made in the political science literature. But it's just the logic of the pork barrel, but applied to lots of different things. And that dynamic is pretty powerful in the state legislature. And it's what you saw. I mean, there's an interesting question why the governor who understood the problem, was quoted understanding the problem, didn't veto the bill? Like, if anyone's in a position to be the voice of reason here, it's the governor.

- [37:20]

A

But you know, again, he's got national political aspirations, too. He's gonna have to defend this.

- [37:25]

B

He's gonna have to defend it, but he'll have to defend it. But that goes both ways because he'd have to defend vetoing it if he'd done that to the teachers and firefighters.

- [37:33]

A

Right. Well, let me close the Chicago specific portion of this and I'll just say for listeners, I'll put this in the show notes, but there's a lot of folks who have done really good coverage of the Chicago specific side of this. If you want to know more. The Chicago Tribune has covered it very well. There's a newsletter called the City that Works that I like a lot on this topic. Austin Berg has done good work on it. So I'll link a bunch of resources if you're interested in, specifically in Illinois House Bill 3657, if you want the title of the particular bill that is Jacking up the Pension Deficit. But let me go back to your book In a Bad State about what the federal government should do if something like this Chicago crisis eventually comes to a head and and the federal government is asked to bail out Chicago and Illinois in some combination. You sketched out this trilemma that kind of no matter what you do, somebody is holding the bag at the end. What principles should our, you know, Our President in 2030 use to think about this problem when he or she goes.

- [38:34]

B

To tackle it really good. So the first thing is, again, we're just so clear. There are three downsides. All the choices are bad. There's austerity, usually in a recession, there's default, which limits your ability to borrow in the future. And maybe other jurisdictions ability to borrow in the future. And there's bailout, which creates moral hazard. So all three bad. Right. And so the question is, what should you pick? And again, the US has picked all three at different times. You can go through different fiscal crises. If you want to read a wonderful book on this, you should try In a Bad State, which kind of tells the history of all of our federal responses to state and local budget crises.

- [39:05]

A

I hope it's not an insult to you say I was surprised by what a fun history it was.

- [39:09]

B

There you go.

- [39:09]

A

I picked it up expecting it to be more policy oriented and not as historically grounded. It totally is.

- [39:15]

B

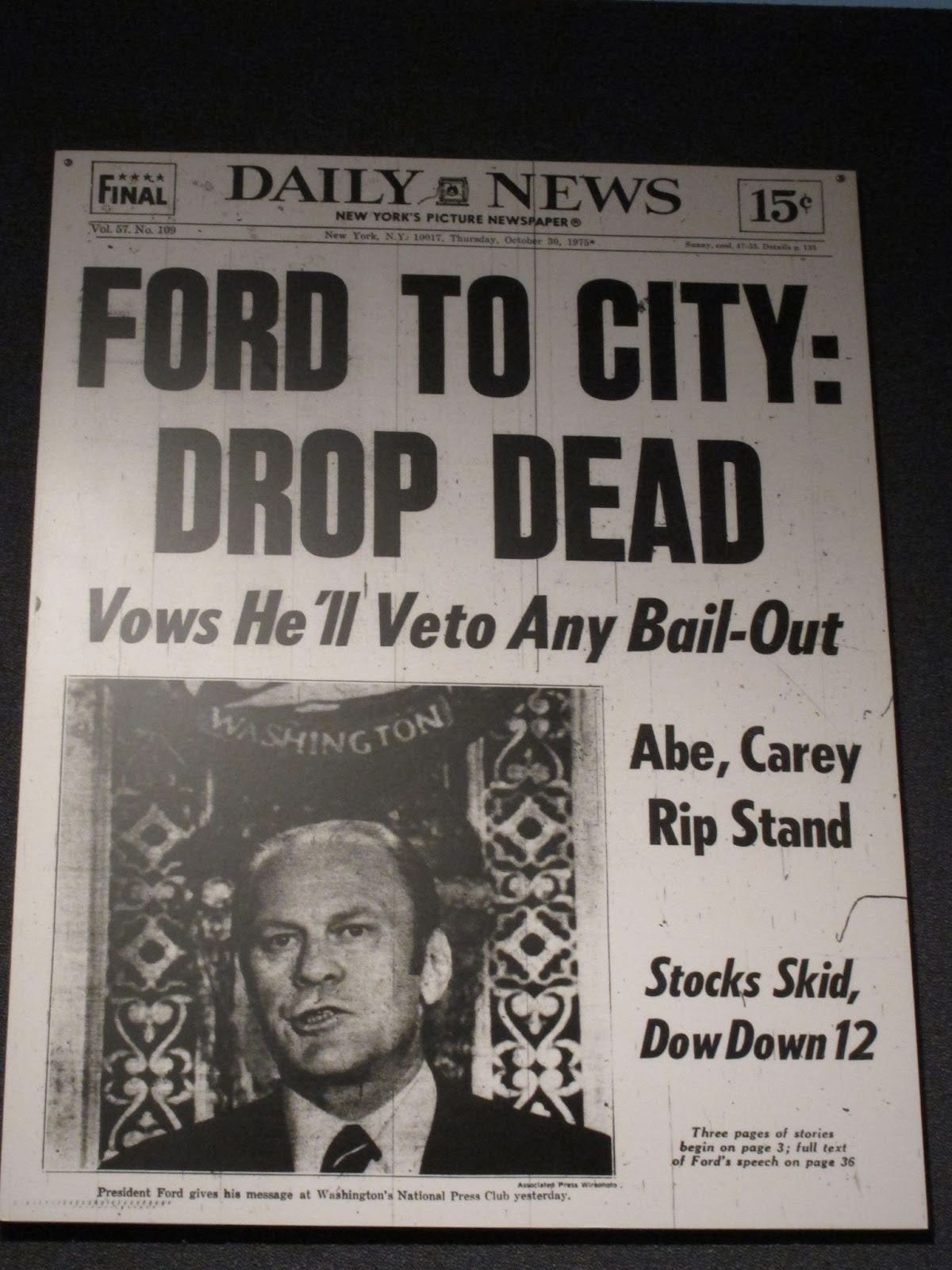

Thank you. So the thing I'd say is that the best responses are not all one or all the other. They mix some elements of bailout, austerity and default. And so an example, for instance, the New York City fiscal crisis, I don't know if it was optimally responsive. Famously there's a headline for the city drop dead where the President Ford is saying I won't bail out New York, but federal government ends up after the city effectively quasi defaults and after engages in a lot of austerity and has created a new governance structure for running it. The federal government offers emergency loans through the Seasonal Financing Act. And this combination, you basically think of it, there's a marginal increasing cost to all three of them that a really big default will stop you from borrowing for a very, very long time time. But a small default we might be able, especially if it's a technical default or something else, if you have to cut everything that's really bad to cut some things that's less bad and it gets increasingly bad over time, really big moral hazard is much worse than a small degree of bailout. Jurisdictions are getting money from the federal government all the time. So the tools that allow you to engage in a little of all three or a little of two are much more attractive than choosing one or the other. And what would this look like? So for instance, in a bankruptcy, so for jurisdictions that are allowed to file for bankruptcy because of the insolvency requirement, because of a few other things, regularly engage in a good bit of austerity. And once they do, the court will say now you're insolvent, therefore you can start impairing creditors. And interesting, you saw in Detroit after the bankruptcy started, then combination of foundations and the state government offered money to help the city pay off some of its pensions. So it got a bailout, but not on the front end after it already suffered. And that reduced the amount of moral Hazard. Because if you're a politician, you've already taken the hit for going bankrupt. You're living in infamy forever. And then getting the bail letter reduces the harm without creating a moral hazard. So that would be one good metric. It's like, what can we do to do a little bit from all three of these bads rather than doing all or one of all of them? The thing you should be thinking about is taking advantage of these crises to set up rules that work well in the future. So in the wake of the New York City fiscal crisis, one of the things that was imposed upon New York was a requirement to use honest accounting rules going forward that limit your ability to get excessively indebted going forward.

- [41:42]

A

Were they using dishonest accounting rules beforehand?

- [41:44]

B

Oh, 100%.

- [41:45]

A

I don't know what honest accounting rules are.

- [41:47]

B

So. So in general government, Jersey can count on what's called a cash basis. Do you spend as much money as you have as much money coming in, going out? But that doesn't affect whether you accrue debt over time. And so New York City was effectively borrowing money to balance its budget every year.

- [42:03]

A

Got it. You had the same amount of money coming in each year, but you were just racking up this big debt obligation.

- [42:08]

B

And then jurisdictions do all sorts of weird stuff in there, but there are a couple of very funny things they do. If you want me to talk about. I'm happy.

- [42:14]

A

Yeah. What are the most malicious and malign ways to hide the problems with my budget?

- [42:19]

B

The funniest are what are called lease and buyback agreements. So the state of Arizona, to balance its budget one year, sold the state house and then made an agreement to buy it back in the future with payments every year. So they rented it for a number of years and then paid it back. And this looks just like a loan. You make annual payments at the end of year, and you have to make a lump sum payment at the end for a thing they had to buy back, you know, but it didn't count as debt. And so that is a pretty funny one.

- [42:46]

A

Lease and buyback. Wow. What else could I do that for? You can do the state house. You could do, you know, courthouses. You do a whole bunch of things.

- [42:53]

B

Oh, jurisdictions have done. The craziest ones are when they do it for jails. Cause then, you know, that's a pretty funny one. I mean, there are a whole bunch of, like, weirdo tricks that jurisdictions use. Another one is changing. So two other ones that are pre are not paying your suppliers for a long time. So basically, if you don't pay the people, like see governments use a lot of paper, you can pay a premium for paper, but agree or tacitly say, we're not going to pay you for six months. And that turns your, the paper company into effectively a lender. Yeah, exactly. So like Illinois, they've cleaned this up a little bit. But Illinois for a long time had like a very long lag time in paying off ordinary suppliers. But that increases the cost because it's a loan. But like the idea that every, everyone who provides Staples is effectively a bond holder of the state of Illinois is a pretty unusual. They do change with the timing. Budget timing is another funny one, one.

- [43:47]

A

That you mention in a bad state is. This was really fascinating to me. It felt obvious the moment I read it and I never thought of it before, but was the creating a new legal entity, shifting all of your debts onto that legal entity and then saying, yeah, sorry, you can't sue us that we're a city with no debt.

- [44:04]

B

So this is an amazing story. This is a case called Port of Mobile. And what happened was a number of jurisdictions, but Mobile is the one that made it to the Supreme Court. The city of Mobile owed a lot of money and so they created a new city called the Port of Mobile. And the state legislature is allowed to create new cities. And the Port of Mobile contains most of the city of Mobile and the state legislature. Now the power to tax property is given to the Port of Mobile and not to the city of Mobile. They're allowed to change who's allowed to tax things. And by the way, Port of Mobile is going to buy Mobile's assets for like a dollar or something. And the Supreme Court just said, you can't do that. We don't really know why, but you definitely can't do that.

- [44:38]

A

This was a funny part of the book. It's like it's not really obvious why that's, you know, constitutionally illegitimate, but it just. You can't do that. That's crazy.

- [44:46]

B

We've now we explain that as a violation of the contract clause. The contract clause, which states that seats can't impair contracts, that this is understood as a functional impairment of contract. But there's really interesting questions about where the line is drawn there. So this is actually something that comes up in the Chicago context, that Chicago, drawing on an example that New York did and that something also Puerto Rico did, issued what are called sales tax bonds. And what these do, the sales tax generally was supporting the general budget and general obligation bonds, not the Normal bonds. And they said, no, we're going to issue new bonds that are backed with a small special claim to the sales tax revenue. And in the case of a bankruptcy, the holders of these sales tax bonds will have a special claim on the sales tax. The question is, is this impairing the general obligation bonds?

- [45:29]

A

Right, because you just said, hey, all this revenue we're going to carve out and it's going to be harder for you to access.

- [45:34]

B

Right. And so that question is like pretty unresolved. This is a big part of the Puerto Rico bankruptcy which involved what called the Cofina bonds.

- [45:42]

A

I've got a couple more questions about pensions specifically. One is you talked a little bit about the history of public pensions and the kind of relatively modern emergence of these massive ones. But maybe to do a second historical pass, why are public pensions structured so differently from private ones? So like if I'm a private company and I want to offer a pension to my employees, I have to use real actuarial projections. I have to fund the pension every year. I can't do this kind of accounting trick. And then I have to buy pension insurance. If I'm a state or local government, I don't have to do any of those things.

- [46:15]

B

Why not? Yeah. So it used to be that defined benefit pensions were much more common and they were, then they were getting into trouble until Congress passed a law called ERISA that imposed all sorts of obligations upon holders. And now as you noted, none of your, most of your listeners don't have these things because companies have moved away from them towards defined contribution systems and to like kind of 401ks particularly. But Congress didn't apply ERISA to state and local bonds for two reasons. One is that again, state, local governments don't default that much. So it's thought, you know. And then secondly, this would be thought to be a pretty big imposition on the kind of federalism rights of states. And so putting all these restrictions on states might be whether it's unconstitutional or not is an interesting question, but is understood to be a pretty big imposition. So states and cities were very resistant and they're very resistant to lots and any real limitations on their ability to do their own internal budgeting. And so that's the story about how they diverge. But the big story is that the defined benefit pension has kind of fallen out of the private sector but remains in the state and local sector. And so some states have, a few states have experimented with moving to defined contribution systems, but it's a rarity.

- [47:25]

A

Makes Sense. One thing we haven't talked about so far in this conversation is just how you should manage pensions. So some pensions are passively managed. Famously. Again in, in our version of famously, Nevada has fully passively managed pensions. And the guy who manages a pension sits in his office all day and plays, you know, doodle jump on his phone or something and just you, you, you put the money in indexes and every year you just follow the market and it's fine. There was an interesting report that if Chicago's pensions had been passively managed in 2024 instead of spread across, I believe more than 80 management firms, the city would have saved something like $40 million in management fees and returns would have been about 25% better. Now obviously that wouldn't be true for every year. Some years it would be a little bit less. But broadly, the city's pensions would be in a lot better shape if looking back, they had all been passively managed rather than actively managed. But that's not always, my understanding is that's not always best practice. You can't just say everybody should passively manage their pension. So how should laypeople like me think about this?

- [48:33]

B

So it's a really good question. It's something that the literature is actually a little unclear about. So the thought of pensions is that because they're creating a long run obligation, just like a university endowment works this way, that it provides the, with the capacity to invest in things that don't have short term returns that gives them a real advantage. And so they should be able to invest in weirder things that give them greater returns going forward because they're managing in the long run, not the short run. And in fact, pension funds are the classic source of funding for alternative investments. Your private equity firms and hedge funds and what have you, the challenge emerges which is that you have like the, on one side of these negotiations, the world's sharpest financial figures. On the other side you have well meaning civil servants who are a little bit outmanned. And by the way, this has led to all sorts of abuses over time that anyone who followed the disputes around Alan Hevesy, who was the New York City controller, and it also involved Steven Ratner, who you may know from watching Morning Joe, but was a big time investment banker. He manages Michael Bloomberg's money and, and the New York Times is money and a whole variety of other things. Anyway, this like can create all sorts of problems because it creates a lot of incentives because these, they're holding giant sums of money. They're also by the way the biggest players in securities fraud litigation. So a huge percentage of securities for litigation is brought by CalPERS, the California Pension funds. And there's a question like, can they do this? Another question is like some, some jurisdictions around the world basically have turned their pension fund into extremely well paid financial firms. Like the pension fund of Ontario is like, the managers make millions of dollars and it's a pretty fancy operation. And so whether moving to passive would be better or whether there's a good is a, there's like potential gains to be had through this. The question is like, can you pull it off? The other thing is that something we brought up earlier, which is that even if you're earning on your pensions, you shouldn't account for your earnings. Right. So jurisdictions traditionally use their earnings returns or expected earnings return as a target for what they should save going forward. They say like, well, we made 8% for the last couple of years, we should save money now as if we're going to earn the same amount in the future. But that doesn't track because you have to pay regardless of whether the financial firm has a good year or a bad year.

- [50:53]

A

Right. You could have a terrible down year next year. There could be some big crisis out of your control and your obligations are still exactly the same.

- [50:59]

B

And there's another wrinkle. There's a really complicated things about like what the money should go into relative to the jurisdictions. You really would prefer it to be things that are up when your budget is down. But there's political pressure to do the opposite. So some jurisdictions invest their pension funds in affordable housing in their own jurisdiction.

- [51:18]

A

Which is clearly tightly correlated with the success of your own jurisdiction.

- [51:21]

B

Right. On the other hand, there's a lot of political pressure to do that. Right. And so it can be a real challenge.

- [51:27]

A

Can we say though that broadly more pensions should look at passive management for their own returns or is it too unclear to even say that?

- [51:37]

B

It's too unclear. I wouldn't be comfortable saying that. It depends a lot on the jurisdiction and how well managed its pension fund is. The thing is like there are potential gains from active management. The question is like, should you expect your jurisdiction to achieve. And the reason there are gains is again because of this long run nature of the obligation. And there are jurisdictions that are just very well. So like Utah is like they just run everything very well in Utah. I don't know how they do it. It just works out well. It's a beehive state. They work, everything works out. And like, if I were talking to Utah, I'd say. Well, I don't know, you guys are pretty good, you know, like, you do what you want, you can take some risks. I feel like you've got it under control. Other jurisdictions, you're like, ah, I don't know, man.

- [52:17]

A

Do we have any evidence that the places that pay their pension managers a lot more do better at active management like I would imagine? Ontario, if you're getting paid millions to manage that pension plan, odds are you're probably doing a better job.

- [52:30]

B

Yeah, I mean, so it's an interesting question. You have to be doing a better job by more than you're getting paid.

- [52:34]

A

Right. If you give me several million dollars a year, I've got to really perform.

- [52:38]

B

Right? You got to really. And you have a staff and there just aren't a lot of incidents, instances of these. And again, and they're also not random. It's not like we've randomly dropped them on jurisdictions. Right. So one reason you'd move to having a privately run organization that's kind of outside your control is because your jurisdiction is incapable of doing so otherwise. Right. So if someone is a problem person, you might want to put all their money in trust. Right. So it's a similar type dynamic and so it's a little hard to say.

- [53:07]

A

Totally. Well, I'm going to put a pin in the pension and bailouts conversation here. And because you are a modern renaissance man with a wide variety of interests, I'm going to spend our last few minutes with a few rapid fire questions. I'm going to give you about a minute for each of them. I'm not going to tightly constrain you, but you know, honor code, try to hold it together. Okay, Excellent. You've done work on a wide variety of interesting political science questions. I'm going to start with your pitch for building more big infrastructure and building it at the federal level. It's called the priority list. We've got a few minutes here. Sell it to me.

- [53:42]

B

Okay. So widely understood that American infrastructure has a cost problem. That is it costs more to build subways in America than it does in anywhere else in the world. And by huge, huge margins, the cost of building highways is both more than another jurisdiction and increasing over time. Similarly, there's research into what might fix this. Right. So the two big buckets of potential problems are about management of projects that states and cities are overmatched. They plan badly, they plan weirdly, and they also are overmatched by their contractors. That's one bucket. The second one is regulations driving up their Costs. So you guys are state capacity people. The NEPA stuff, CEQA stuff, I'm not going to rank. You get the idea? Love it.

- [54:22]

A

And so listeners, if you're confused, I direct you to everything else we've ever done on state.

- [54:28]

B

So the priority lists an idea of how we might actually enact these reforms. So there's a lot of reforms, everyone knows they're politically really difficult to achieve. So how might we actually do it? And so the idea is that Congress should, when it's approving its general transportation bill, give the Secretary of Transportation the ability to designate 10 or 20 and the number isn't important, super duper important, super popular projects and attach to those the reforms that might improve fresh. And this would involve the sending a crack team of federal experts to help Satan's and jurisdiction's plan, giving them special financing tools and exempting them from a whole variety of regulations for just these projects. And the idea is that Congress, where Congress might not be able to pass NEPA reform, broadly speaking, they could have done some stuff, you've talked about it.

- [55:12]

A

But they, but there's more to do, right?

- [55:13]

B

There's more to do and they can't do reform by America. But for the projects that are the most important, the biggest deal in America projects they could attach these exemptions to and use the popularity of those projects to achieve the political firms they can achieve more broadly. And then those projects would be an.

- [55:30]

A

Example what kinds of projects might fall into that super popular bucket. I'm having trouble picturing what would be overwhelmingly popular.

- [55:37]

B

Think of whatever China's doing and then imagine it on an American scale. So like a new giant, new subway system, big highway, big transmission system, big pipelines. And you can imagine any number of things that fit within these categories that are like. And you'd have to spread them out because it's Congress. But like it's not that hard to imagine if you think about on the scale of the Golden Gate Bridge and the whatever that thing that connects Detroit and Canada, that bridge that are like a really big, big, big deal project. Anything that the President would find it useful to go and do a big ribbon cutting for, for the current President, we could coat it in gold.

- [56:10]

A

Sure. But I guess then I have one more question there, which is when you say transmission systems or big subway systems, all of these have big, you know, widely shared benefits. You could bring down energy prices broadly with better transmission. You could reduce travel times all over a city with a subway system. But famously the costs are really concentrated and they get any of these Big projects would have, you know, a strong lobby of people who hate that project and a lot of people who would stand to benefit a decent amount from it. Like why would this get around the problem of people always hate projects with more ferocity than the people who, who want them built?

- [56:44]

B

The idea is that these would be like national goals and they'd be the kind of thing that the president and leaders in Congress could brag about at election time. I was able to achieve the new Big Dig or whatever. You just think about them and like while everyone else talks about doing infrastructure, I did it. And here are my 10 examples. And that, that mass politics could defeat the nimbyish politics.

- [57:07]

A

Right? Another easy question. Does zoning matter more or less in an era of remote work?

- [57:14]

B

Great question. So the answer is it matters both more and less. This is going to be a more complicated question.

- [57:18]

A

So boo complicated nuance question. We hate nuance.

- [57:24]

B

So remote work, which again, the broad effects of it we're still feeling. But we've seen a increase in the relative value of suburbs and exurbs to downtowns, both office space and rent space in housing space across cities. And we may have seen some movement across jurisdictions, but again, it's not everyone. Most people are commuting three times a week. But that has the effect of generally making suburban land a little more valuable relative to urban land. And this has the effect of. It may reduce the housing imbalances, driving housing costs in the places where it's reducing demand, but it will have the effect of increasing demand in other areas. Right. And so it might make commutes better. There's more developed land which might reduce housing cost as a problem. Those areas are themselves tightly zoned. And so the ability for the market to match to allow housing to be built in the exurbs of New York City relies on agricultural space being turned into housing or it relies in like. So one of the big areas that have seen huge run ups in value in the post pandemic era was in Connecticut. You saw it in Fairfield county, which an hour developed. But you see one acre lots, two acre lots. By law, these are the richest places ever. You know, Greenwich, Connecticut, Westport, Connecticut, you know, like they're, you know, very rare. And like there's been even greater increases in the value of these things as people are commuting a little less. But you can't build housing there. There's still housing prices in New York City. Even if it has taken a little bit of the edge off it, it's still a huge problem. So it's not like it's become not a problem in those places, by the way, also in zoning can be a problem even in places that are losing population in the Midwest can limit the ability to transition land uses.

- [59:07]

A

Say a little bit more on that. If I'm a city in rural Illinois, let's go back to Illinois. And I'm losing, you know, 3,000 people a year from a city of even less, let's say I'm losing 500 people a year from a city of, you know, like 50,000. I'm just slowly declining. Why should I care about zoning?

- [59:23]

B

Because zoning controls not just the building of new apartment buildings, which is kind of the example that people. But it involves the uses of land. And so what you might want in a jurisdiction like that is to knock down houses and put up a tree farm. I don't know whatever it is you might imagine. But relies anything that's changing, if the law doesn't change to match current demand, then that can create a problem. And so you see real problems in declining jurisdictions related to like the ability to open home based businesses in areas that had been previously all residential. And these jurisdictions need jobs very badly. So the land use problem is about transition. It's like we have a law that fits current uses or sometimes it's lower than current uses. And then the world changes because the world is always changing. Even if demand's going up, demand's going down, and if the law doesn't accommodate that, then we can run into dislocations.

- [60:13]

A

Great last question for you, David. We haven't talked much at all about the New York City Charter Commission, which, you know, relative to the really famous pensions that we talked about is even less famous, I think.

- [60:25]

B

But it's the new hotness, man.

- [60:27]

A

It's the new. We're just early. That's what I'm going to tell myself. We're just early. I'm going to ask you to explain what's going on with the New York City Charter Commission ballot initiatives. And then I want to ask kind of a broader question which is you and I both care a lot about housing supply. It's something we think about a lot. And a lot of your work has been focused on, okay, what are the kind of governance tweaks or the changes to the structures of these systems that can unlock a lot of home supply. And I guess my question is like, what are the limits to that? Theoretically you could change all kinds of ways about how New York is governed and some people would still not want more housing. Some people would Want more housing. There are all these attitudes people have that are just kind of underlying whatever governance system you have. So explain to me why you're optimistic about the big changes that would be introduced by this charter commission. And then like why should I be optimistic?

- [61:17]

B

Well, so let me start with the second question and I'll go back to the first question. So what you're expecting there is like, there's a famous quote from H.L. mencken which is the democracy is the belief that the common man knows what he wants and deserves to get it good and hard. The modern political scientists response to this is democracy can be structured in many different ways and those things will have different outcomes. Now New York City won't become Houston in no matter how you aggregate votes, they're just differing opinions. And there's a lot of work to be done on housing, on convincing people. But internal to these things, whether the mayor will structurally have different opinions in the city council. And that is about the prominence of the mayor and the ability of voters to know who the mayor is and hold them accountable for something. And it's also to do with the method of aggregation that is say like choosing one person versus choosing many people. And the Charter Revision commission is about both of those things or it's really kind of changing the methods of aggregation. So one thing it does that's very simple is it proposes moving election day to an even numbered year. And why is this important? It would mean more people vote. And so there's a lot of evidence that shows that when you hold elections in odd numbered years, fewer people vote. And this is systematic effects of not only how many people vote, but who votes do you have much more turnout among homeowners and much less turnout among renters. And there are other. It's much whiter, it's much richer and so forth an odd number of years. And one idea they have is it's going to require the state legislature to agree with them. But it's to move the election to even number years to increase the turnout in elections which will have effects on the outcomes. Both are democratic. The current system is also democratic. It's just that this system would encourage a different number of people vote which will have different systematic outcomes than housing. The other reforms are to the process of decision making. Again, in one minute I'm going to explain the ulurt processes too much to.

- [62:57]

A

Bear, but the fastest ulurp explanation.

- [63:00]

B

Yeah, so let me just talk about one of them rather than all of them. One of the changes involves for zoning changes that include a degree of affordable housing below market rate, subsidized housing or rent regulated housing. For zoning change right now it needs to go through a process that includes getting voted yes by the city council and yes by the mayor. There are process before that, but those are the two funds final steps. And in a context of a legislature that it doesn't have partisan competition. We generally see something called councilmanic privilege or all demonic privilege in some places, member deference in other places. And the idea here is that when a zoning change is made in the neighborhood, that council person gets to decide with no one else having any input. And it's the exact same dynamic we talked about earlier about universal log roles. What the charter Revision Commission does is change. Even if the city council votes no after it's gotten yes through all the other processes, that decision itself can be vetoed by a combination of the mayor and the borough president. And it does other things too. I don't want to. That's not the only thing it does, but that's one of the things it does. And the idea here is that it creates a degree of check on this neighborhood, gets to veto what happens in its neighborhood and that will have the effect. Basically it's a way of checking like classic NIMBYism in the sense that like I don't care where it goes, just not in my neighborhood. In here the borough president is the county level official. It's like a bigger official. And the mayor is obviously a five county level official. And the idea here is to limit. It's a procedural rule that says again, both rules are democratic. They're just different democratic rules that say that broader elected officials can veto in some levels. This neighborhood level competition that's driven by dynamics in the city council and this should make rezonings easier because systematically not always that mayors and borough presidents are generally speaking more pro growth than individual members, at least about specific projects in specific districts.

- [64:48]

A

That's great, David. It's been a real pleasure. This might be the most interesting conversation I've had on pensions and local government bailouts in a long time.

- [64:56]

B

Oh, thank you. Thank you again. So we got very weedsy, which I thought was like the spirit of the pod and so I kept it.

- [65:01]

A

But you thought correctly. So thank you.

- [65:03]

B

But the book will say it's like there are really dramatic stories here. This is about if you want to know why the south didn't develop infrastructure in the end of the 19th century. It wasn't able to borrow. It has to do with these stories. If you want to know about history of corporate suicides. Like we want to know about what happened in New York in the 1970s. Municipal debt seems boring, but it's actually the history of America.

- [65:27]

A

Love it. I'll leave it at that. David, thank you for joining.

- [65:29]

B

Thank you so much for having me.

- [65:36]

A

Sam.