Loading summary

Transcript98 lines

- [00:00]

A

48% of Gen Z say they search for 30 minutes looking for streaming content. And 56% of Gen Z in the UK this is an existential crisis, I think, in the ecosystem.

- [00:30]

B

Welcome back to the Media Odyssey Podcast.

- [00:33]

A

That is Evan Chaparro and that is Marion Renshett.

- [00:37]

B

Today we are dinging into a report that just got dropped during Stream TV Europe, Lisbon. And we jumped on it. We actually, as always, you know, had a little bit of a preview and were able to dig into the latest report from Bengo called subscription signals 2026. Ivan, did you have time to take a look at it?

- [01:00]

A

Well, you know, we did get it before Stream TV thanks to our friends Bango, and we did the same report with them last year. So it'll be interesting to watch what happened year on year. If you don't know, Bango is a subscription bundler. So a lot of the bundles like hbo Max and Netflix or Verizon, plus those two that you may be subscribing to, is actually powered on the back end by a provider like Bango in that specific case. And so they allow these different platforms to bundle and create economies of scale for the consumer, but they don't have to go through all the rigmarole and mechanics of wiring it together on the back end. Van Gogh does that as a white label service. So this report is a comprehensive look at attitudes towards and actions around subscriptions in the US and the uk. They do this report every year. They give us an advanced look. I did have a chance to look at it before Stream TV in Lisbon, which was unfucking amazing. Thank you for such a good time, Lisbon. Thank you, Marian, for being there and being such a. A great contributor. Your event prior was amazing. So anyway, we're going to be doing Stream TV in Denver this summer in June, and if you use my code, SHAPIRO10, you get a 10% discount for that conference. It's June 16th through 19th in Denver, just before Cannes Lion. So I'm flying to Denver and then from Denver to Cannes to see you, Marianne, in France, where you're from. But let's dig into this. Let's dig into this report. It's full of fascinating facts. I'm going to let you drive this. What was the thing that most stood out to you about this study that Van Gogh did?

- [02:46]

B

Honestly, there's so much data in there, it's very hard to make a decision. I have to say I'm always keen to see how many subscription per person you have because I do feel that, you know, we're Nearing more and more. That glass ceiling where people are like, I have too many, you know, I gotta cut. And I do it myself regularly. I actually, you know, some subscription come and go. We, we've spoken about this, it's the serial churner. But so that data, fascinating to see that, you know, looking at the US versus the uk, the UK has more. The UK has more subscription. So for those of us, you know, joining us on audio platform 5.7 subscription per person in the UK versus 5.2 in the US and then, you know, knowing that one has more than the other, I understand why the UK is spending on average so 68 pounds, but, you know, $90 versus the US 69. But where I don't completely get it is that historically a lot of the tiers in the US were more expensive than they were in the uk. So this got me puzzled. But perhaps you have an insight on this.

- [04:06]

A

Well, so, yes. So if you are listening, we'll walk you through it. But this is a good episode to watch on YouTube because it has a lot of visuals with charts and graphs that we created to represent the data. And you're right, 5.2 subscriptions on average in the US, 5.7 in the UK, $90 a month in the UK versus less than $70 in the US. And I think there's a couple of different reasons for this. Most notably, you know, sky, which is really the only. There are others, but it's the biggest pay TV provider in the uk, doesn't have as much of share of the market as the pay TV providers here in the us. The pay TV providers here in the US bundle up a bunch of different stuff and that looks like one subscription to the home. Right. And I think it creates economies of scale that, that you can't necessarily find in the uk. And remember, the other thing is these subscriptions aren't just for television either. These are for other things as we'll see a little bit later. So it's, it's, you know, maybe pay TV and SVAD or premium streaming, but it could also be things like news or food. There's a, there's a category that's goods, physical goods shipped on a monthly basis. So I do think there's a number of different contributing factors. And we're going to have, have Giles from Bango on a little bit later in the pod, and I think we can dig into this with him, but I think we can also ask him maybe in the next study to ask, you know, what comprises this in the average home? What, what, what is the suite of services. It's a complicated, that's not a non linear question to ask. So I can also appreciate how hard that would be to survey. But this was surprising to both of us. I mean it's a, it's a, it's a, It's a like 25% increase in the UK versus the US per home. Really interesting about. Also I would say, I would say another thing, the US is a much larger country and so there is a just a wider diversity of economic strata in the US to a certain extent because of the size of the geography and the population. I think it's six times larger by population. So I also think that's a, that's a contributing factor as well.

- [06:23]

B

Yeah, you said something about sky and I think whether that's sky or other, you know, telcos in the uk, but in Europe at large, historically they were very keen on bundling, you know, mobile, Internet, TV and then lately asvod. But it was done in such a way that you could kind of build your bundle. Right. So those were add ons and the thing is that a lot of subscribers and will come to that afterwards, people actually want to save money. And so what sky has been doing, they just launched a couple of weeks ago a master bundle that is like £24 per month, something like ridiculously cheap. And you have Disney, HBO, Netflix, etc. You have five, six different services in there. So your point about, you know, plus your mobile, right? Yeah, I think, I'm not sure actually. I don't know if you have the Internet for sure, but we can ask jail. I'm not sure if mobile is included, but that's like a massive pay TV SVOD bundle and I think they understand that they need to do a bit more of those hard bundles versus you just do add ons. Exactly to that point. Right. To make sure that people feel like they're not spending as much, but they have a lot to chew on.

- [07:45]

A

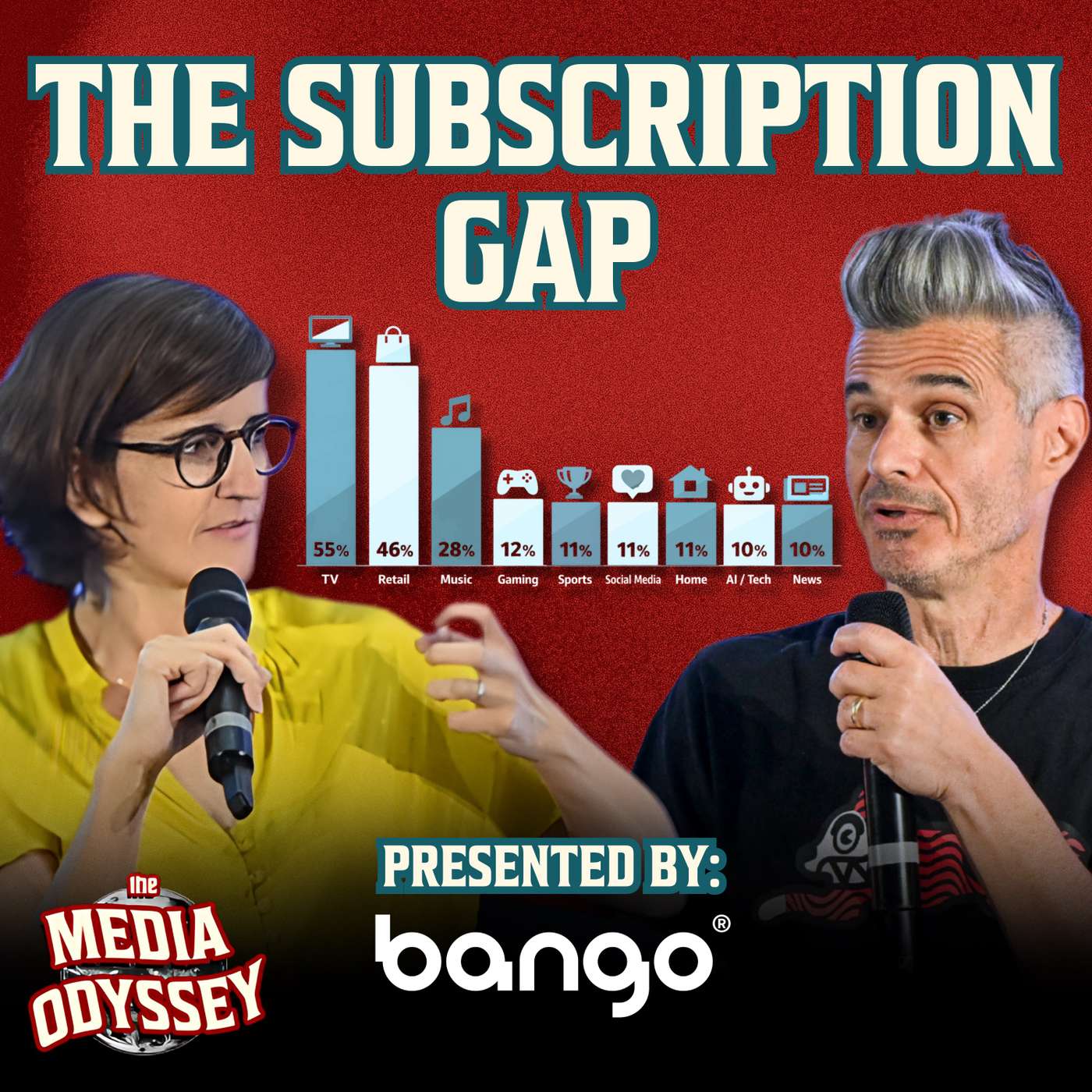

And that's more of a de rigueur again French here in the US where you know, typically if you're getting broadband and pay tv, they're bundled together and very often phone, not just landline, which is going away, but mobile is bundled in there as well. So Charter does that and has been doing that for a while. Comcast does that and has been doing that for a while. A lot of smaller providers also do that. But to your point, the new thing is now Disney plus and ESPN and other things are being bundled into the pay tv. So I do think you're going to see this price go down. There's telling data here, we'll get to that in a second. Around, people believe they're paying too much and I think that's one of the major reasons why the price will be forced to come down. But here are the rankings of subscriptions. So these are the subscriptions people say they have rankings ranked by the share of people, and this is across UK and us, the share of, of each, the share of the population that has each subscription. And SVOD is number one by a lot, which is, I think, kind of remarkable given, you know, in the grand scheme of things. Premium streaming is a relatively new product. Right. Compared to, let's say, mobile phones or pay TV or even newspapers and things like that. And yet it is dominant. It is by far and away number one. Number two, and this was true last year, but this is still surprising to a lot of people. After premium streaming, the number two, and again, there's a huge distance between second place and third place is retail. So this would be Amazon, but other types of retail subscriptions. Tesco has one, Walmart has one. And it's just, I find it kind of remarkable that, that it's almost 20%, almost 50% higher. Almost. I'm sorry, almost 100% higher than music subscriptions. You know, we all have, I thought we all have Spotify or Apple Music or some kind of music subscription, but in reality, far almost twice as many people have a retail subscription as have a music subscription.

- [09:49]

B

Yeah, absolutely. Yeah. The retail piece is surprising to me still because, I mean, aside from Amazon. Well, I'm saying that. And I had a retail bundle a while back with the local supermarket chain here in the Netherlands. So I guess that's that. Right. And I think they're underplaying that they're not offering enough. You know, historically they've just focused on, you know, you pay X and then you get. It's not actually free delivery for most of the time. And like Amazon, it's like reduced, you know, delivery fees, but they should capitalize on the fact that they have that relationship and that they could build, you know, on top of that. And that's what Walmart did. I do have a suspicion that this bundle with Paramount and Peacock is going to go away, at least Paramount, because I've heard, you know, we were looking at the, the, the Paramount investor deck and they said something about a bundle that would go away. Perhaps that's this one, and it would be a biggie for, for Paramount.

- [10:53]

A

Yeah, I think if, if Walmart drops Paramount as a Bundling that, that. I think you're right. That will really hurt Paramount plus probably disproportionately over it hurting Walmart. Because if you think about who would buy that bundle, that's a, that's a pretty large group of humans and I understand that it was a, was one of the most successful bundles out there. I also think. Do you, do you have an Amazon prime subscription?

- [11:17]

B

Uh, I do not actually.

- [11:19]

A

You don't.

- [11:20]

B

My husband, my husband does, but ever since I've moved here to the Netherlands.

- [11:25]

A

Your home does?

- [11:26]

B

Yeah, well so yeah, my, my home does, but I thought we didn't have it and because let, let me say we've been in the Netherlands for eight years and prime in the Netherlands is kind of tiny because the historical player is called ball.com and it's like the Walmart of, you know, of here.

- [11:43]

A

Got it.

- [11:44]

B

And so yeah, I, I really don't use Amazon and buy, you know, as little as possible from those platforms anyway.

- [11:53]

A

So I, yeah, same, but so you, you, you hinted at this. Amazon is I think probably one of the largest subscribe subscriptions on the planet Earth. I think it's, you know, it's probably closing in on 300 million total users in some form or fashion. And when I ask audiences, when I'm in front of them live, I say who here has an Amazon subscription? The whole room raises their hand. Amazon Prime's membership. They all raise their hand. And then I say, has anyone thought about canceling? Despite the fact that the price keeps going up and no one raises their hand. But because Jeff Bezos is a human dick, I decided look at him, he just looks like one. His rocket looks like one. Everything about the symbol for the Amazon looks like a penis. He is penis obsessed and he is going through the greatest, largest midlife public crisis other than Elon Musk on the planet Yachts. I mean yeah, there's debate. Not just a yacht, but a yacht so big it gets stuck in a canal. The largest yacht in the history of mankind and you know, just the, the marries the, the tradest of trad wives anyway so. But because he also is destroying the Washington Post and is just a, just an all around bad person. I broke my subscription to Amazon to see if we would notice and that that's been over seven months and we do not notice. Here's the thing about Amazon. You're paying for shipping. You're not paying distinct on each ship but you are absolutely paying for shipping. And you're also shopping more because you think you get free shipping and so my channel, I believe that there's going to come a time and there's data in this survey that I think that that, that supports this, that people realize that this is a ripoff and that they're going to start canceling Amazon because it's so, so expensive and they're not going to notice a difference in their lives and that's going to be a bad moment for Amazon. But what's interesting here is so AI social people. More people are paying for social media, more people are subscribing for pay to social media than do AI and news, by the way, that's amazing, don't you think?

- [13:56]

B

Yeah, yeah, but we were surprised last year. But I guess, you know, I'm an old one, so I'm the oldest millennial, so I'm like social media. A subscription ad free. Show me, I did not even know that existed. And I think it's things like Snap, Snap has one, but, but you also

- [14:14]

A

pay for other super user benefits that you don't get without paying. So I, I, that hasn't really grown all that much. But neither has AI with all the AI hype that's out there. Right. I don't think that the individual subscriptions to AI is on a growth cycle. In fact, if anything, with the canceling of the destruction of Sora, which we heard about last month, I think the era of trying to sell distinct AI subscriptions to individual human beings, I think we're coming end of that era and that it's going to be much more a bundle that you're going to get your AI in. Think about this. Do you pay for Gmail or email at all? Do you pay for search? No, you get it inside a suite of services which incorporate advertising or some other set of economics. And I think that's the way that AI is going to go. What I also found surprising. So I think we're coming to the end of the individual D2C AI other than super users, but also like news, 10%, only 10% of consumers pay. Do you subscribe to news at all?

- [15:21]

B

Yeah, I actually have one subscription. Yeah, it's more, it's less news. News, it's, it's a, you know, it's a, it's a publisher, it's a magazine. It's not Le Monde or the New York Times, but I do have one. Yeah.

- [15:33]

A

And I have several. And yet there, you know, 90% of the public between UK and US don't. I found that interesting as well. All right, let's move on to this. This is the one where I think the indication of churn is going to increase and also that, that you're going to see kind of a culling of subscriptions. To your point from earlier, this question is I spend more than I can afford on subscriptions. And not surprisingly, UK was higher than the us Almost a third of people in the uk. And I imagine that the younger you get, we can ask Giles whether or not there's a cut on this for Gen Z, but the younger you get, the more true this is. And almost a quarter of US folks think that they're paying too much for subscriptions. I think there's a churnpocalypse acceleration that's going to happen across subscription because of this data right here.

- [16:26]

B

Yeah, actually the data says that in the US it's almost double that. So 41% of Gen Z in the US think that they're overspending. And so what's interesting though is that people still feel like that and we're what, two, three years into ad supported tiers. The data also digs into the, the ad tolerance. Right. Are people, you know, ready to actually get ads, you know, on paid tiers, etc. And in 2024, Bengo said it was 78% were against it, strongly objected to that. And now 36% of American would double their ad load for lower price points. I found that crazy. I have to admit that, you know, I'm not, I'm not spot on there because I really don't like ads. So I'm ready to pay more, but I'm ready to then cut someone else's subscription. So I cut, I'm not going to say who, but I cut someone just recently just to keep, you know, the, the rest without any ads.

- [17:30]

A

And then when you look at the younger demographics, it's, it's half, Half of millennials in uk, almost half in the us half of Gen Z in the US almost half in the UK say they would have, they would take twice as many ads if they could lower the price of their subscriptions. And there, there are certain services like Netflix where I pay the higher price to avoid ads, but there are services I would not subscribe to if they didn't have a lower tier with ads. Peacock being the most, the biggest example of that. I would just not watch Peacock ever if they didn't have a lower price ad tier. I suffer through an incredible ad load of the same ad over and over. Same thing with Hulu over and over and over. But because I don't want to pay for 25 premium ad free tiers. You know, I do this and I think this is the calculus, this is the algebra that all consumers are in the midst of doing in their home right now. But I think it's especially true of Millennials and Gen Z, who are, I think, more cost conscious than, let's say, Gen Xers like you and me.

- [18:41]

B

Yeah, absolutely. Fascinating to see also some data on sharing passwords. So 20% of Americans say that they still do that. Right. 19% say they have no idea who's using. And in the UK it's even higher. I have to say I shouldn't. But, you know, I, yeah, I, I, I, I do share that. It's funny, there's one that I share with my dad. It's not my dad sharing it with me, I'm sharing it with my dad.

- [19:14]

A

Well, that's what happens. You reverse trend, you become.

- [19:17]

B

Exactly. And every time I travel there, it's like, can you put it off me for the next 30 days? And then he hopes I'm going to come back within 30 days to benefit from it. So people have been, you know, able to circumvent it.

- [19:30]

A

And I mean, but it's, I think this number is a lot lower than it used to be of password sharing because Netflix really cracked down and then now Disney's cracking down and so you log on to your service and you can't get in because someone else is using it. Right. So I think that number is going to continue to creep down because it's becoming physically impossible to password share.

- [19:53]

B

Yeah.

- [19:54]

A

This one I found not surprising, but I think it's a really neat data point that's incredibly telling, which is 60%. So almost two out of every three consumers in the US and the UK, 59% in the US, 60% in the UK are much more loyal to an individual show than they are the platform that delivers it. And this goes to your point of Serial Churners. Earlier, whenever I'm in front of an audience, I always ask, who here has signed up for a premium streaming service, watched the fuck out of a show, binged it, and then canceled before the next billing cycle. Almost everybody in the room raises their hand. So the serial churner is now basically the norm for, I think, everything other than Amazon and Netflix. To be blunt, I think everybody else basically serial churns based on what's on that service per, you know, per month or not everyone but most. And I think that's going to only increase over time, which to me speaks to the need for a free version of every service. If you truly want to keep that consumer around and sell advertising to them, it's crucial that they never break up with you. Even if they stop paying you, keep them in for a free service so that you can sell ads to them. That'll help you reduce churn overall. But also I think it'll help you drive up your average revenue per user on a monthly basis.

- [21:17]

B

Yeah, I think Fubo in the US Virtual MVPD did that right. A couple of years ago. They build a front porch Canon. Please.

- [21:25]

A

Directv. Directv has one. Dish has one. Sling has one as well.

- [21:30]

B

Yeah, but streamers don't want to do that. And actually I think Crunchyroll used to have one. They've stopped it. Streamers historically, they've never launched like that, having that front porch. So let's see what happens. I think that there's a lot of pressure coming from people consuming content on Tubi, you know, the Roku Channel, Pluto. Maybe that will push the pace to go one step further. And, and also let's be clear, all of these guys still have minuscular advertising businesses within. You know, the bigger, the bigger company,

- [22:04]

A

I think the pressure to.

- [22:05]

B

Yeah, it's 5%, right? Less. Even less than that. So I think it's an opportunity to bring a bit more scale. And what's fascinating though is, you know, what I read here and it's less about the bundle discussion that we're having now, but it does mean that, you know, you need to have a very IP led strategy, whatever you do, because, you know, what's the point? People do. Not really. Except like you said, Netflix and Pride. People are not loyal to your service, they're loyal to your content. Then this is where you put your effort. Yes, you need to work and make sure, you know, that you get some sort of attribution. But again, people reading, diving into the report will see that people are incapable of saying, you know, who has what. We know because we're in the nitty gritty of this. But like only 20% of UK respondents put Star wars on Disney plus, you know, 13.

- [23:04]

A

Yeah. What's the severance?

- [23:06]

B

Apple TV, et cetera. Same for Game of Thrones.

- [23:08]

A

Only 13% of the people who watch Severance know it's on Apple tv. Yeah, well, it's mind boggling, true.

- [23:16]

B

But even like Game of Thrones, that's huge, right? So I know it's HBO. I thought everyone else knew. And only 18% said it was HBO. Most people said it was Netflix. So yeah, quite fascinating.

- [23:31]

A

And Netflix, it seems like Netflix gets over Attribution. Most people said that they could identify the shows that's on Netflix, but I think that's also because they're attributing too many shows to Netflix. I think they think they watch more shows on Netflix than they actually do.

- [23:45]

B

But there's one thing is that lately Netflix has, you know, made a major push in licensing third party content and it's.

- [23:53]

A

Right.

- [23:54]

B

Especially shows. And it's kind of crazy because actually everything I'm seeing right now I feel like I'm, you know, 10, 20 years back. So you have er, lately front end center on Netflix. Yeah, person of interest, like a lot of kind of old shows that were.

- [24:11]

A

But that's because, yeah, so that's, you know, the suits phenomenon I think convinced them that they need to do that. But then they're also. We talked to Jordan Schwarzenberger about this, you know, who works with the sidemen. He showed that the sidemen being on Netflix didn't add new viewers to sidemen, but it added new viewers to Netflix. So the people are following not just their favorite IP but their favorite talent. Ms. Rachel, Mr. Beast, on Amazon, you're seeing the talent basically move around from platform to platform and consumers following them. This is to me though, probably one of the greatest issues facing content right now, the content business right now. And we've talked about this a lot. In the US, 30% and in the UK, over 40%, 41% say they search for 30 minutes or more on streaming looking for content. And when you go to gen Z, it's 48% of gen Z say they search for 30 minutes looking for streaming content. And 30, 56% of gen Z in the UK say they spend 30 minutes or more searching for content on streaming. This is an existential crisis. I think in, in the ecosystem we

- [25:29]

B

suck at fixing this. And I'm, you know, I mean, I'm thinking no one wants to. So actually where was I a few weeks ago where someone CTV platform was, you know, saying, oh, it's so great, people come X time per day on our own page and the play was very much, you know, we're selling against that, you know, real estate, da da da. But what they don't realize is that, you know, we are wasting time on that homepage.

- [25:59]

A

Right.

- [26:00]

B

So great, you're monetizing it. But I'm sorry, you're going to lose long term, you're going to lose on the new acquisition, the retention and the time spent. So I think people do not want to fix this problem.

- [26:15]

A

Yeah, I don't know That I agree with that 100%. We, we talked about this at the beginning of the year. I'd made a prediction that along with Roku, had put this prediction out there and I, yes, anded it, which is that the ad free viewer is going to go completely away, that there won't be anything, there won't be anything like an ad free viewer anymore. Because most televisions in the world now have a home screen ad that is sellable. And so you're going to see an ad before you get to whatever it is. Even if you're going to an ad free service, even if you're going to gaming, when you turn on your television, you're going to see an ad. And then to your point, the search process, which is getting longer and longer, is actually going to be rife with ads. You're going to see ads all over the place. They'll be contextual. And so I think they'll be a little less annoying than let's say social media ads, but they're still going to be omnipresent during your search, unless you're in Netflix or you're in some other service. If you're on a Roku TV and you're searching for something to watch, they have all this inventory. If you're on a Samsung television, if you're on an LG television, you're gonna see all of these. If you're on YouTube, while you're searching for content on YouTube, you're gonna see ads. So I do think you're right. This is intentional on behalf of the industry. But I don't think they understand the friction it does create for the consumer themselves, I think.

- [27:40]

B

I don't think so either. Yeah, absolutely.

- [27:42]

A

So now let's, let's look at, you know, bundles so this data and we'll bring Giles on to, to talk about this. Because this is, Bundling is really his expertise is his survey, but this is also his expertise. This is who consumers in the UK and the US say they expect to get subscription bundles from. And it's not the TV provider, even though SVOD is the number one subscription by far that everybody uses the people, the people expect and look to mobile providers and retailers for their bundle. Way ahead, at least 10 points ahead of the TV provider. And then social media is almost right on the heels of the TV provider. So I found this incredibly interesting. And then there's this other data. And then let's bring Giles in to talk about this stuff. In the US, over a third of people who subscribe to anything subscribe through third party bundles. So, you know, 63% still subscribe directly to the Netflixes or the chat GPT of the world. But a growing segment of the population is now bundling for economies of scale and it's even higher in the uk, which again I found interesting because it doesn't have as big a tradition around pay TV. 39%, well over a third of people in the UK say they prefer and get their bundles of services through third parties like banks and telcos rather than subscribing direct. Now still 60% subscribe direct, but that number is going down year on year. I found, I found this number growing at the pace that it is to be relatively surprising.

- [29:26]

B

Yeah, I think there's a few things I will say in the uk I'm not surprised but because as a whole in Europe we are, you know, in the habit of using our mobile operator, broadband provider, etc. To you know, bring on. So it can be paid tv, but it's been a lot of svad, it's been a lot of music, etc. Telcos in the regions are trying, not very successfully yet, but you know, to have a role in gaming subscriptions as well. But you know, at the end of the day, the reason behind this, yes there's money, but it's also ease of use and management convenience. You had only a couple of subscriptions, it was fine to manage this directly. We set it at the top almost six subscription per person in the UK and in the us. It's crazy. And so the value, and I see this very strongly and it's fascinating. I launched Netflix at orange like 12 years ago. I did that deal and at the time Netflix only wanted to allow credit card subscription because they wanted to control the relationship and be direct. And we had to say, guys, our billing component is very strong. People like having stuff on their bill and they just pay one bill. And so they ended doing, they ended up doing it and they actually saw that the subscribers who were using the operator billing was actually more engaged in terms of the number of hours they were watching per month than, you know, some of their direct customers. So I think this is a trend that can only grow provided that those people, those third party bundlers still make it easy. I don't want to have someone in the way of all of this if it's not making my life cheaper and easier.

- [31:17]

A

I completely agree cost is going to be increasingly important, especially as the world is on fire and the price of everything goes up. But then secondarily, you're right, I Don't want to deal with 12,000 different middling little credit card bills at the end of every month. Okay, so. So, first of all, I want to point out that you can download this entire report from Bango. The link to download it will be in our show notes. Wherever you're watching or listening to this, look for the link right below the show icon. But I have an embarrassing question to ask you that I think only you can answer. Which is, is it Giles or Giles?

- [31:59]

B

That's a great question.

- [32:00]

A

As someone who pronounces his name Shapiro, I'm very sensitive to this, and I love this guy. I. This is the happiest you're ever going to meet in your life. I love to see him at conferences. It's always, like, heartwarming to see him, but I am embarrassed. There he is. There he is. Giles Gyles. What? How do you pronounce your name? I can't say that.

- [32:24]

B

Damn. I wanted you to be Frenchmen.

- [32:27]

C

That doesn't work. Whatever you like. Evan, you've got my name right about five times today, so don't ruin it.

- [32:32]

A

Okay.

- [32:33]

C

Giles.

- [32:33]

A

So it's Giles. That's what I thought. Okay, it is Giles. I thought so. All right, so Giles tongue is a tongue.

- [32:39]

C

Yeah, that's right. Although people try and avoid that because they think it can't really be canon.

- [32:43]

A

Giles tongue, which is also a great dish at a del. Contestant. Giles tongue. But if you. If you touch. That's a cat's deli joke. If. So, Giles Tong, welcome to the pod. You're a great friend of the pod, even though this is your first time on. Your title is head of marketing of

- [33:04]

C

VP Marketing at Bango. Yeah, I run all the marketing here.

- [33:07]

A

I call you cmo and I think they should pay you as such. So this is your report. And so, first of all, did I get the description of Bango and what you guys do correct at the top of the show?

- [33:19]

C

Yeah. Perfect. We're enabling subscription bundling for anybody who wants to be bundled. So third party distribution of subscriptions. You could think of it that way.

- [33:28]

B

Nice.

- [33:28]

A

And you're sitting in front of a vending machine for some reason, not because you like M&Ms, but because you have this product that enables bundling. That's really kind of impressive. Can you just describe what your vending machine, your physical analogy of a vending machine means?

- [33:45]

C

So we call it. The product is called the digital vending machine. So it's enabling subscription bundling, which means we're handling all of the complexity around payments entitlement. Management, all the bits and pieces that are required behind the scenes to enable a company like a mobile operator to effectively sell somebody else's product. And then we're joining the dots between those companies so that if you get Netflix free with your mobile plan, you can then quickly go and log on to Netflix and in you guys.

- [34:16]

A

So it's more complex than that. Your vending machine allows the consumer to mix and match at will. Right. So it's not just the mobile says, this is a bundle you can buy to a certain extent, when a partner of yours uses this correctly, the consumer can go on and say, I want a little AI, I want a little social media, I want some tv and all those things. Right. So that, that it's. It creates infinite choice for the consumer.

- [34:38]

C

Yeah. So we're behind the scenes as such. So we're enabling companies to be able to offer whatever they want. So whether that's. So let's touch one of the trends at the moment, which is multiparty bundles. So two companies, two independent companies coming together in a single price point, and that being available like let's say, Netflix and Max, for example, in a single price point, we can enable that very easily. So we're handling all of these complexities behind the scenes, and then it's up to the operator to choose what it is they want to offer. It could be a single bundle or it could be a kind of marketplace situation where there's streaming, gaming, productivity, whatever, and we're enabling all of that to happen.

- [35:17]

B

And so the subtitle of the report was the Great Disconnect. Do you want to, do you want to elaborate on that? What are you seeing?

- [35:25]

C

Yeah, sure. So a lot of the data you already touched on here, we wanted to explore kind of what's around the corner, what's happening now and what's around the corner for subscribers. In previous years, we've talked about subscription fatigue and the multitude of choice and how this is causing problems. People can't remember how and where they've subscribed. What we wanted to do was go a little bit further this time and look at some of the attitudes. Try and understand if some of those questions around ad tiers and password management are still the case or if we've moved on. I think probably one of the more surprising elements in the study for me was the attitude to add tiers. So a few years ago where we all subscribed to subscription services to get rid of ads, now the situation has evolved so much that we are in a mindset of I Want to access all of these services. What's the most efficient way I can do that? So now people, we call them savvy subscribers. When you think of subscribing, you're thinking, where can I get the best deal? Is it through my bank? Is it through my retailer? Is there a discount here? Or at least a trial period. So they're looking at different ways. And the attitude to ads specifically is I can actually access probably more services if I take the ad tier. So it's kind of like a trade offer.

- [36:39]

B

Yeah, absolutely. And so one thing that I've. We didn't touch upon that, but I wanted to have your take because it feels insane. But a lot of the respondents said that they were actually keen to have AI manage their subscription. And to me, that's this big black box. I would never do that. Like, you know, private information, credit card detail. So could you speak to, you know, how much of a trend, and especially I think there was a big, you know, dichotomy between Gen Z and Millennials or older.

- [37:16]

C

Yeah. And that actually you've already observed, that's happened pretty much with every question, the Gen Z Millennial. And the general response has been so very different. I think with AI, we've got a couple of things happening here. We've got the popularity of AI services. Let's just say the subscriptions. But as Evan's already mentioned, you know, how many people are actually paying for the subscription? I think we've seen a lot of people using AI. They're also spending 30 minutes plus for discovering something to watch, which is crazy. Instead, they're looking for recommendations, so they're turning to AI and particularly, you know, voice AI. About quarter of people using voice AI. And there's a great service that was launched by Liberty Group, which is using AI with it's called Supersearch. They developed that to help people with this discovery issue, to say, and there's a great example Google TV give, which is you're sitting there with your partner and you don't even describe who's there. You just say, we want to watch something. And it knows your background, your tastes. I'm into action, they're into drama. And here's some kind of ideal thing that you can watch. The next step from that is that the AI or the agent is then managing the subscription for you. So it's now proposed, oh, you want to watch this particular show. But to do that, you'll need the service and we'll subscribe you to that. So it's part of that Discovery and access continuum.

- [38:38]

B

On the discovery piece I get it because I started doing that myself and I've actually pushed a lot and that was one of the key trends I had for this year was for streamers and while content providers at large to find a way to have a GEO strategy. Because right now when I say on Friday night, what could I watch and I give a couple of info and then I have ideas, everything stays within a ChatGPT URL's and I think that's a massive loss. Right? We could have a link that then takes me to a Netflix or XYZ to then have me watch that particular piece of content that got recommended. So on that I agree. But then on the subscription management I think that's just, that's just insane. It's like giving the keys to your house. But anyway, again, you know, well the bit.

- [39:24]

A

But I think so Agent. Agentic AI. So agentic services is something that everybody's betting is going to be the future revenue explosion for AI. I think you're right. I think giving access to AI, giving AI access to my bank accounts and my credit card numbers is a little scary. But let me ask you this. Do you have a banking app on your phone?

- [39:48]

B

I do.

- [39:50]

A

Did you read the terms and conditions of that banking app before you installed it on your phone?

- [39:54]

B

No.

- [39:54]

A

Okay, so you say it's not going to happen and yet you do give access to Zelle or whomever it is to all your freaking money on your app without understanding what they're allowed to do with that.

- [40:07]

B

True. But it's a highly regulated environment. The bank and AI is nuts right now. It's just like the world wide West. Right.

- [40:16]

A

So I agree we've been talking about this for a while. Search is a lot of friction in the ecosystem and then there's this great fear that AI is going to replace all these jobs in show business. But the solution to both is AI is probably going to replace, you know, task driven jobs. I don't think it's going to create replace the creative arena, but this is the perfect use of AI which is find me something to hug and watch. And I don't think it's going to be individual AIs that do it. I think to Giles's point, it's going to be wound inside or to your point. Actually the Liberty is a pay TV provider. They are the perfect one. They also have all the data of all IP on the planet Earth that comes across their platform and they have deterministic data of their users. These are credit card Numbers, home addresses, phone numbers, emails. So they can really predict with a tremendous amount more certainty that this consumer is going to want to watch this. Netflix should be introducing this, Disney should be introducing this, they should be building their own models for their own platforms to solve this problem. And then you don't necessarily have to give your bank account to the agent Giles. Is that your takeaway?

- [41:33]

C

Yeah, I think that's the point. And we talked about, you know, who would you trust to provide with your subscription services? Who do you want to get your subscription from? And the mobile operator came out on top. And we have pay TV in there as well somewhere. These are the services who could be providing that agentic solution. And then you're back to just adding to bill, which is why the magic happens. Anyway, with bundling, you have that trusted relationship.

- [41:56]

A

So if there was one big takeaway, I mean, there's a big study, we couldn't cover it all in this one pod. And we encourage people to go to the Show Notes and download the study right now. But if there was one big aha moment for you in this study of all of them, I asked my server last night, if you could have eat only one thing on this menu, what would it be? What's the one big aha moment that you found?

- [42:18]

C

Well, I think I've probably got one for, for each of our audiences, which would be the telco side and then the subscription provider side. On the telco side, we use this line bundle or be bundled. You know, there's a lot of pressure in the market about the role that you're going to have. And this report really is talking about, you know, the relationship you'll have with your customers. And there is a risk here to telcos that they will have that taken away from them if they don't continue to delight their customers with excellent experience. And all these issues here we've talked about are kind of matters that affect their experience. So the threat there is that somebody like the Neobanks who are now starting to offer connectivity, their service will be bundled effectively. The OGs of bundling the mobile operators could end up being somebody else's bundle. Their first party becomes somebody else's third party. So there's the message there for them, you know, bundle or be bundled, it's a real threat. And the on the subscription provider side, the takeaway here is that 40% of subscriptions are already bought through indirect channels. If you are looking at your numbers and you're not seeing 40%, then there's a big opportunity waiting for you.

- [43:30]

A

There.

- [43:31]

C

So, you know, time to jump on board and, you know, come and speak to us and we will jump in the waters. Lovely.

- [43:37]

A

More.

- [43:39]

B

Awesome. Well, thank you so much for coming on the pod, Giles. That was fantastic. Again, we're going to be sharing the link to the the report in the show notes on LinkedIn. It's going to be in our substack, Mediaware and Peace or Evan and Swimming Medic for Myself.

- [43:56]

A

And it's free. The report is absolutely free.

- [44:00]

B

Yeah, yeah. Well, yeah, we're not selling.

- [44:03]

A

It's not bundled.

- [44:05]

B

Yeah, exactly.

- [44:06]

A

Well, it's bundled.

- [44:08]

B

It's bundled with the pods. You know, you get a free report with Bengal.

- [44:12]

A

That's excellent. Great. Wow. That was really nice, Mary. Very good.

- [44:16]

B

Well, thank you again for being on the podcast. And Ivan, that was the Media Odyssey podcast with you, my dear.

- [44:24]

A

And you, Marion Wrenchette. Thank you all for listening yet again. And we'll see you next week. Sam.