Podcast

The Media Odyssey

Hosted by Evan Shapiro & Marion Ranchet · EN

Each week, two of media’s most influential thinkers, Evan Shapiro & Marion Ranchet, take on the hottest media topics with their hottest takes, helping their audience chart a course through the maelstrom that is today’s Media Odyssey.

Based in the US, Evan Shapiro is the Media Industry’s official Cartographer, known for his well-researched and provocative analysis of the entertainment ecosystem in his must read treatises on Media’s latest trends and trajectories.

Marion Ranchet, French expat based in Amsterdam, has become the industry’s go-to expert in all things streaming, building a following for turning even the most complex problems into easily digestible and actionable insights.

Ranchet and Shapiro are known for their sharp-yet-accessible content on Media consumption, audience trends, and the shifting fundamentals of the business itself. Even during the toughest of topics, they each make talking about Media fun. Together every week, these two will offer entertaining, often humorous, and always educational content on today’s Media Odyssey.

42episodes

Episodes

Newest firstAll episodes

REGIFTED: WHO WILL WIN 2026?

3d ago00:51:18Summary readyHappy Summer Break from The Media Odyssey podcast! The media industry isn’t heading for a clean recovery but bracing for another year of pressure, recalibration, and structural change.Welcome back to The Media Odyssey Podcast with a special thanks to Spectrum Reach! In this first part of their 2026 predictions, Evan Shapiro and Marion Ranchet lay out what the coming year will likely bring for media, technology, and entertainment. They cover ongoing layoffs, fragile ad markets, the rise of global distribution strategies, and a new phase of AI-driven discovery. 2026 will test which companies have truly adapted and which are still relying on outdated assumptions.2026 is not a breakout year, but a proving ground, where survival depends on cost discipline, platform fluency, and the ability to monetize audiences directly rather than through legacy intermediaries.Key Takeaways:1. 2026 Will Be Another Brutal Year for Media EconomicsEvan predicts that advertising markets will remain soft, public service media will continue to face funding pressure, and layoffs will persist across the industry. There will be no broad recovery, only isolated winners and many organizations forced to do more with less.2. Discovery Will Matter More Than Content VolumeMarion predicts that success in 2026 will be defined by distribution and discoverability, not by how much content companies produce. Media organizations that don’t adapt to YouTube, FAST, social, and AI-driven discovery will struggle to reach audiences at all.3. The AI Bubble Will PopBoth predict that generative AI and large language models will reshape discovery, navigation, and search long before they meaningfully change creative workflows. The biggest short-term impact of AI will be invisible but existential for traffic-driven media, but the hype and direct-to-consumer models are unsustainable. 4. GEO Will Undermine Traditional SEO-Based Media ModelsEvan predicts that Generative Engine Optimization will replace classic SEO as search engines move from links to answers. Media companies built on referral traffic will see declining reach unless they rethink how their content surfaces in AI-driven environments.5. FAST Will Become More Crowded and Less ForgivingMarion predicts continued FAST channel proliferation without equivalent ad growth. The result: more fragmentation, lower yields, and fewer viable players with success limited to brands with strong IP, live content, or true differentiation.6. Media Companies Will Be Forced to Think Globally by DefaultGrowth will increasingly come from international audiences, not domestic ones. Both predict that companies without global distribution strategies will hit growth ceilings faster in 2026.7. Experimentation Will Be a Core Survival RequirementThe final prediction is cultural: organizations that don’t test formats, platforms, and monetization aggressively will fall behind. In 2026, waiting for clarity will be a losing strategy.Thank you to Spectrum Reach! https://www.linkedin.com/company/spectrum-reach/ Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/Marion Ranchet - https://www.linkedin.com/in/marionranchet/The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast (00:00) - Introduction and Hosts (00:57) - First Prediction: AI Bubble Burst (04:03) - Debate on AI's Future (10:01) - Second Prediction: Micro Drama Bubble (14:22) - Third Prediction: Outcome-Based Advertising (17:01) - Fourth Prediction: Midterm Election Advertising (19:19) - Fifth Prediction: Social Media Politicians (21:51) - Sixth Prediction: New Generation of Media CEOs (25:56) - Seventh Prediction: Media Mergers and Acquisitions (27:06) - The Largest Leverage Buyout in Corporate History (27:21) - The Role of Saudis in American Media (27:38) - Mergers and Acquisitions in Advertising (29:00) - Cultural Clashes in Mergers (29:56) - Netflix's Strategic Moves (31:23) - The Future of European Media (31:57) - Predictions for Media Mergers (34:30) - The Rise of YouTube and Social Media (39:09) - The Impact of AI on Media (43:18) - The Extinction of Ad-Free Viewing (49:55) - Final Thoughts and Predictions

Summary

REGIFTED: FRONTLINE PUTS PBS ON YOUTUBE

1w ago00:48:50Summary readyHappy Summer Break from The Media Odyssey podcast! Public service media isn’t outdated, instead, it’s fighting for relevance, trust, and survival in a fractured global information ecosystem.Welcome back to The Media Odyssey Podcast. In this episode, Evan Shapiro and Marion Ranchet sit down with Raney Aronson-Rath, Executive Producer of Frontline and Editor-in-Chief of Documentaries at GBH, for a conversation on the future of public media. From political pressure and funding cuts to platform expansion and audience trust, the discussion explores why public broadcasters must be everywhere audiences are without sacrificing journalistic integrity.Through Frontline’s transformation into a broadcast-plus-streaming powerhouse, the episode examines how YouTube, social video, theatrical releases, and global distribution have become essential tools for sustaining factual storytelling in an era of misinformation and declining institutional trust.Key Takeaways: 1. Public Media’s Survival Depends on Platform Expansion, Not RetrenchmentPublic broadcasters can no longer rely solely on linear TV. To stay relevant and trusted, they must meet audiences on YouTube, social platforms, streaming, and in theaters. They need to be wherever public conversation is happening.2. YouTube Is Additive, Not Cannibalistic for Public Service MediaFrontline’s experience shows that YouTube doesn’t replace broadcast audiences. In fact, YouTube extends reach over time, attracts younger viewers, and builds long-tail viewership that linear TV alone cannot sustain.3. Streaming Requires a Long-Term Mindset ShiftUnlike broadcast’s appointment viewing, streaming rewards longevity. Frontline films often grow for years, accumulating millions of views with high watch time, forcing teams to think beyond premiere-night metrics.4. Community and Trust Are the Core Competitive AdvantagesPublic media’s strength isn’t scale but credibility. Building engaged, thoughtful communities around factual content is essential in a media ecosystem flooded with misinformation.5. Short-Form Is Editorial, Not Promotional To reach younger audiences, Frontline treats social video and shorts as a serious journalistic format with its own language instead of marketing cutdowns of long-form work.6. Global Distribution Is Both a Mission and a StrategyWith one-third of Frontline’s audience outside the U.S., platforms like YouTube enable public media to reach global audiences including countries where traditional broadcasters refuse to air critical journalism, but where audiences need to see it most.7. Public Media Must Be Everywhere Both In Person and OnlineFrom YouTube to theaters to festivals, Frontline Features reflects a belief that storytelling is more powerful when audiences can experience it both collectively and individually.8. The Cost of Absence Is Being Replaced by Worse InformationIf trusted public media doesn’t fill digital spaces, misinformation will. The choice isn’t whether to engage platforms like YouTube, it’s whether to leave them to actors with lower standards.Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/Marion Ranchet - https://www.linkedin.com/in/marionranchet/The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcastThank you, Raney Aronson-Rath for joining the pod!Raney Aronson-Rath: https://www.linkedin.com/in/raney-aronson-0343aa8/Frontline: https://www.linkedin.com/company/frontline-pbs/Headshot credit: Michael Buckner/Deadline (00:00) - Introduction to the Media Odyssey Podcast (00:09) - Public Media Under Pressure (00:55) - BBC Controversy and Public Trust (02:58) - Challenges Faced by Public Broadcasters (04:02) - Public Media Funding Issues (04:47) - The Role of Public Media in Democracy (05:59) - Public Broadcasting in the US (07:25) - Embracing Digital Platforms (09:13) - Introducing Raney Aronson from Frontline (11:16) - Frontline's Digital Transformation (15:43) - Impact of YouTube on Frontline's Reach (23:56) - Simultaneous Broadcast and Streaming Strategy (26:22) - The Evolution of PBS Viewership (27:10) - Leadership and Digital Expansion (28:08) - Global Reach and YouTube Strategy (29:05) - Commitment to Journalistic Standards (31:14) - Frontline Features and Theatrical Impact (34:18) - Challenges in Documentary Distribution (39:42) - International Co-Productions and Self-Distribution (43:44) - The Importance of Public Media

Summary

H1 2026 PART 2: BUBBLES, BALLS, & BIG AGGREGATION

2w ago00:28:03Summary readyTwo-thirds of the world watches more video on their phone than on TV, TikTok is beating Netflix in most markets under 55, and traditional media is ignoring 60% of its own audience's attention. It’s The Media Odyssey’s season two finale!Evan and Marion zoom out on the biggest trends of the year so far they haven’t covered yet: the AI investment bubble, the creator economy's growing pains, the state of kids' content, and the measurement crisis at the heart of the streaming and social media landscape. It's one of their most data-rich, openly argumentative episodes of the season.Part 2 goes deep on Evan's brand-new ESHAP Cross-Screen Attention Index, the first attempt to measure total video attention across screens in eight global markets, and what it reveals about where audiences are actually spending their time in 2025.Key Takeaways:1. The ESHAP Cross-Screen Attention IndexLaunched at index.eshap.tv, this is the first publicly available tool to measure total video attention across screens in eight global markets (US, UK, Germany, France, Italy, Spain, Brazil, Mexico), cross-collateralizing TV measurement data (Nielsen, Barb, AGF, Kantar), handset data (Sensor Tower, Comscore), and consumer diaries (GWI) to de-duplicate simultaneous screen usage. Key finding: 81% of the global population is under 55 and for that group, the phone, not the TV, is the center of gravity for video consumption.2. TikTok Is Bigger Than You ThinkIn almost every market studied, TikTok ranks #2 in total attention among consumers under 55. This means TikTok beats Netflix, Disney, Paramount, NBCU, and Warner Bros. Discovery. In several markets, it beats YouTube among viewers under 34. When TikTok gains share in a market, it takes it from streamers. When YouTube gains share, it takes it from traditional media. These two dynamics are running simultaneously and are why every major streaming platform is now rushing to launch a vertical feed.3. The Phone, the TV, and the Whole ConsumerEvan and Marion's core debate: Evan argues traditional media is failing because it's treating TV and phone as separate businesses rather than a single consumer continuum. The evidence: Obsession and Backrooms were both discovered on social media and are both crushing it at the box office. Saturday Night Live's audience is now on YouTube the next day. France Télévisions opened its entire annual conference by declaring the murder of traditional television. But Marion pushes back, pointing to Channel 4, France Télévisions, and TF1 as examples of European broadcasters already making the move. She argues the platforms, not the broadcasters, are the ones failing to support the transition commercially.Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8 Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/ Marion Ranchet - https://www.linkedin.com/in/marionranchet/ The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast (00:00) - Season Finale Setup (00:44) - Why Measurement Breaks (01:34) - Launching The Index (02:06) - Deduplicating Multiscreen Time (04:32) - Under 55 Shifts Everything (06:17) - Interactive Share Scenarios (07:18) - Living Room Vs Real Life (10:20) - Quality Of Attention Debate (12:05) - Social Drives Culture (13:26) - Continuum Not A Binary (17:36) - Legacy Media On Platforms (20:13) - Monetizing Social Video (23:36) - Platform Frustrations (25:58) - Check The Methodology (26:22) - Built With LLMs (27:02) - Season Wrap And Goodbye

Summary

H1 2026 PART 1: BUBBLES, BALLS, & BIG AGGREGATION

2w ago00:32:43Summary readyAI infrastructure is now two-thirds of US GDP with 90% of companies investing in it reporting almost no ROI, and the media industry is frozen in place waiting for a merger that may never close. Happy H1.This is the Season 2 finale of the Media Odyssey Podcast (split across two parts) with a deep dive into H1 2026. Evan and Marion zoom out on the biggest trends of the year so far they haven’t covered yet: the AI investment bubble, the creator economy's growing pains, the state of kids' content, and the measurement crisis at the heart of the streaming and social media landscape. It's one of their most data-rich, openly argumentative episodes of the season. Part 1 covers the macro forces reshaping media and the creator economy. Key Takeaways:1. The AI BubbleAI infrastructure investment in the US has reached two-thirds of GDP, driven almost entirely by demand from two unprofitable companies: OpenAI (which lost $38 billion last year) and Anthropic. SpaceX's post-IPO valuation dropped 34%, and a subsequent $25 billion bond offering collapsed shortly after launch. 90% of companies that have made significant AI investments report negligible productivity gains, with costs far outweighing benefits. A correction is coming in the next six months, and it will ripple through the entire media industry.2. Creators vs. Brands: A Broken PartnershipCreators were the dominant conversation at Cannes Lions. Unilever even committed to having a creator in every zip code. But the economics remain broken: brands consistently undervalue and underpay creators, creator posts are declining in efficacy, and agencies are buying creator platforms (Whalar, Influential) without truly understanding how to use them. The emerging model to watch: brands acting like creators like the Kit Kat Heist and companies hiring creators in-house rather than as contractors.3. Kids' Content: Despair With Green ShootsStreamer commissions for kids' content are down significantly from their peak, YouTube has gutted the economics of kids' content monetization due to regulatory fears, and public broadcasters now fund over 50% of kids' content worldwide. But bright spots are emerging: ToonStar just signed with Fox; Disney partnered with Lumi/Animage on a new JV; and Super Awesome has been handed advertising rights for the under-13 segment on Roblox. BBC Studios' Bluey model (owned IP, fandom-first, multi-platform) remains the clearest template.Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8 Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/ Marion Ranchet - https://www.linkedin.com/in/marionranchet/ The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast (00:00) - Welcome and H1 Trends Setup (02:21) - AI Bubble Warning (05:48) - Media Deals Fallout (09:13) - Europe and AI Power (13:12) - GenAI SEO Shift (15:42) - Attribution and Hiring (18:19) - IBC Live Show Plug (20:31) - Creators Take Over (26:11) - Kids Media Crossroads (28:18) - Streamers vs YouTube (32:21) - Wrap and Part Two

Summary

THE ART OF THE CAREER PIVOT

3w ago00:51:06Summary readyWe’re back with another Media Odyssey LIVE! In this episode, Evan and Marion are joined by former media executives Tony Goncalves and Ami Angelowicz to discuss how to pivot your career after corporate media. The panel shares their personal stories of navigating layoffs, “misalignment burnout”, and finding satisfying careers completely in their own control. The conversation dives into building personal intellectual property, actionable daily habits for transition, and why taking a leap of faith on yourself is the best investment you can make.Key Takeaways:1. Misalignment BurnoutAmi Angelowicz breaks down "misalignment burnout"—the disconnect between your daily professional activities and your innermost values. She shares how moving into upper management often pulls creatives away from making things, leading to deep dissatisfaction, and why her layoff ultimately served as a turning point to start running her own agenda.2. Optimizing for FreedomTony Goncalves discusses his departure from Warner Brothers Discovery and the crucial realization that he needed to separate his personal identity from his corporate title. He emphasizes the importance of explicitly defining what you are optimizing for in your next move: title, money, or freedom.3. The Creator Pivot & Personal IPEvan highlights the trap of subverting your personal brand for a corporate one. He advises professionals to start building their personal brand before they actually need it by "shipping value to the universe for free," which eventually attracts organic opportunities.4. Treating Yourself Like a StartupMarion shares her strategy for launching her consulting business by viewing herself as a startup. By identifying a specific industry problem—US companies trying to launch in Europe—and creating specific content pillars around it, she positioned herself as the solution and bypassed traditional business development.5. Daily Habits for GrowthThe panel shares actionable strategies for staying sharp during a career transition. Recommendations include waking up curious to research daily, becoming a voracious consumer of new platforms to understand algorithms, and leveraging introspection to maintain momentum and avoid isolation.Chapters00:00 Introduction and Welcome to Media Odyssey Live01:13 Marion and Evan’s Journeys Out of Corporate Media03:51 Ami on Misalignment Burnout and Launching Laid Off Life10:05 Tony on Surviving Mergers and Defining Personal Purpose15:43 Rebuilding Your System and Establishing Personal Branding19:44 Finding Your Authentic Voice and Editorial Filter23:18 Marion's Strategy for Building an IP-Based Consulting Business28:38 Daily Habits to Stay Ahead of the Industry Curve35:32 The Importance of Introspection, Therapy, and Small Goals45:21 Final Takeaways: Optimize for Freedom and Invest in YourselfInterested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/Marion Ranchet - https://www.linkedin.com/in/marionranchet/The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast

Summary

MEDIA SHARK WEEK

3w ago00:38:45Summary readyComcast is splitting in three, Fox just bought Roku for $22 billion, and the Paramount-Warner merger still hasn't closed. Welcome to Media Shark Week.This episode of the Media Odyssey Podcast is Evan Shapiro and Marion Ranchet's deep-dive into the wave of media mergers reshaping the streaming and broadcasting landscape in real time. Recorded in early July, it covers four major deals in rapid succession: the Comcast-NBCUniversal split, the Sky acquisition of ITV, the Fox-Roku deal, and the stalled Paramount-Warner Bros. Discovery merger. Without guests (or filters), Marion and Evan are comparing notes, disagreeing openly, and calling their shots on what each deal actually means for the future of streaming media, cord-cutting, digital advertising, and the balance of power between legacy media and big tech.The throughline: vertical integration in media has repeatedly failed not because the theory is wrong, but because the execution never happens. Comcast never integrated NBCUniversal just like AT&T never integrated Warner. The companies that are winning (Fox in particular) are the ones building digital content and advertising flywheels while everyone else is digging holes and filling them back up.Key Takeaways:1. The Comcast Three-Way SplitComcast is splitting into three companies: a connectivity/broadband entity, a spun-off NBCUniversal/Sky entertainment group, and the already-separated Versant. One read: this is a prelude to selling NBCUniversal, with Netflix and Apple as the most likely buyers. The combined Charter-Cox-Comcast broadband entity would control 70–75 million US homes, effectively controlling how most Americans access all streaming content.2. The Sky-ITV DealSky acquired ITV's broadcast network for £1.6 billion, leaving ITV Studios as a standalone content producer through 2032 under an existing supply deal. The combined Sky-ITV package could solve Netflix's ad sales weakness in its two biggest markets (US and UK) in one move. ITV Studios could also be a potential acquisition target for Banijay or others hungry for English-language IP, including Love Island, which had its biggest year in Season 12.3. Fox Buys Roku for $22 BillionRoku (once valued at $50 billion) sold to Fox at roughly a third off peak valuation. Evan calls Lachlan Murdoch the sharpest traditional media CEO in the US: Fox sold assets to Disney at the top of the market, invested in Tubi, Red Sea Ventures, Holywater, and Whaler, and now controls roughly 50% of US TV screens through Roku. Combined, Tubi and The Roku Channel are larger than Disney streaming. Marion's concern: Fox is too US-focused, Roku needed an international partner, and merging a tech culture with a programming culture almost never works cleanly.4. The Paramount-Warner Merger StallThe Ellisons targeted a July close and it isn’t going to happen. The UK Culture Minister has intervened, and the attorneys general of California, New York, and other states have filed suit to block the merger of CNN and CBS News. The AGs are playing a long game, and there's no realistic path to closing before the US midterms, which was the Ellisons' primary motivation for the deal in the first place.5. Integration Is the Only Thing That MattersEvery failed deal in this episode (AT&T-Warner, Comcast-NBCUniversal, WBD) failed for the same reason: the companies never actually integrated. Comcast didn't even unify its ad sales departments across NBCUniversal. The Fox-Roku deal has real upside, but only if Fox does the hard work. The pot of gold at the end of the M&A rainbow is real, but only for the companies willing to integrate.Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8 Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/ Marion Ranchet - https://www.linkedin.com/in/marionranchet/ The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast (00:00) - Welcome and Shark Week (00:44) - Comcast Splits NBCU (03:19) - Why Integration Failed (05:44) - Who Buys NBCU (07:03) - Charter Comcast Mega Merge (12:02) - Sky Buys ITV (17:27) - ITV Studios Next Moves (20:15) - Fox Buys Roku (23:23) - Roku Risks and Upside (32:47) - Paramount Warner Deal Trouble (36:15) - Wrap Up and Live Show

Summary

VERTICAL PREMIUM TV: THE NEXT BILLION DOLLAR IDEA?

Jul 900:45:08Summary readyThe growing vertical video landscape has potential far beyond microdramas. Two TV veterans just built the studio to take vertical premium all the way with true crime, dating reality formats, scripted drama, and a 12-step AI process to get there.This episode of the Media Odyssey Podcast with Evan Shapiro and Marion Ranchet features Guy Hameiri and Lior Friedman, co-founders of RoseBerry, a vertical premium television studio built on the belief that mobile is the new cable. Guy comes from 25 years in traditional TV production (Survivor, X Factor, Shtisel on Netflix). Lior comes from Amagi and the commercial side of streaming media. Together they're building a start-to-end studio producing originals, repurposing legacy TV catalogs for vertical, and distributing through their own first-party app, Epis.The episode covers RoseBerry's full model: deals already signed with Fremantle, Banijay, All3Media, and A&E to repurpose existing catalog IP into vertical short-form; a proprietary 12-step AI-assisted conversion tool called Red Snapper; originals; and EPIS as a test-and-learn platformt. The Neighbors case study (an 18-year-old Fremantle soap reformatted for vertical featuring a young Margot Robbie) is presented live on the pod as proof of concept.Key Takeaways:1. Beyond MicrodramaThe current vertical market is dominated by melodrama tropes with high churn and low retention. RoseBerry is betting on genre expansion including true crime, dating reality, soap, and scripted, to target an underserved audience. Paywall conversion on top-performing shows is already exceeding 50%, with 70% of those converting to subscribers.2. Red SnapperRoseBerry's proprietary 12-step AI-assisted conversion tool takes horizontal long-form TV and reformats it for vertical. It handles frame cropping, pacing, graphics, storyline focus, and music rights. The process started manually with human editors to establish craft standards, then was automated at scale. It's the core IP that makes repurposing 5,000-episode catalogs commercially viable.3. Epis as a Data EngineTheir app Epis exists primarily as a first-party data platform, not just a distribution channel. It lets RoseBerry track user-level behavior across genres, sessions, and geographies. Subscribers on EPIS are now spending over an hour per session on top-performing content.4. The Library OpportunityGuy's "10,000 for 10,000" framework is if a rights holder monetizes 10,000 hours of catalog content at $10,000 per hour per year, that's $100 million in new annual revenue from IP that is otherwise sitting dormant. RoseBerry's pitch to Fremantle, Banijay, All3Media, and A&E is a new monetization window for libraries that traditional streaming cannot fully exploit.5. Mobile as the New CableGuy's biggest claim: mobile will replace what cable was with movies, series, true crime, and reality available on-demand in vertical format. Netflix, Disney, Peacock, and Paramount are all launching vertical feeds, creating a coming demand for premium vertical content that RoseBerry is positioning to supply.Thank you Lior Friedman and Guy Hameiri for joining the pod!Thank you Lior Friedman and Guy Hameiri for joining the pod!Lior Frieman -https://www.linkedin.com/in/lior-friedman-94958939/ Guy Hameiri - https://www.linkedin.com/in/guy-hameiri-/ Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8 Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/ Marion Ranchet - https://www.linkedin.com/in/marionranchet/ The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast (00:00) - Heatwave and Setup (00:42) - Guests Intro and RoseBerry Origin Story (05:13) - Why Vertical Needs Premium (09:22) - EPIS Platform Explained (12:06) - Syndication and Data Flywheel (15:46) - Neighbors Vertical Clip (18:22) - How Verticalizing Works (22:31) - Originals and New Genres (24:22) - Dating Reality Trailer (24:53) - Love Or Money Twist (25:50) - Gamified Tokens Debate (28:14) - Vertical TV Goes Mainstream (31:13) - Mobile As New Cable (32:24) - Proof In The Data (35:02) - Quibi To TikTok Shift (37:36) - Repurposing At Scale (38:46) - Red Snapper Workflow (41:18) - Data Driven Windowing (43:37) - Wrap Up And Predictions

Summary

BLUEY, LEGO, AND CROSS GENERATIONAL FANDOM

Jul 200:39:27Summary readyTwo nearly century-old brands. One brand-new animated series. And a first-of-its-kind partnership that's never been done before.This special episode of the Media Odyssey Podcast was recorded on the Croisette at Cannes Lions, hosted inside BBC Studios' headquarters, and features three guests across two breaking news announcements. Jasmine Dawson, SVP of Digital at BBC Studios, returns for what's become an annual tradition on the pod to unveil the Affinity advertising network. Affinity is a five-vertical, fandom-first ad sales operation expanding globally with a major push into the US. Dan McGolpin, Director of iPlayer and Channels at BBC, joins to announce a new internal BBC Group partnership that will see BBC Studios' digital sales team represent public service BBC YouTube channels outside the UK for the first time. And Anna Rafferty, SVP Digital Consumer Engagement at the LEGO Group, joins to break the news of a first-of-its-kind Bluey x LEGO co-commissioned content series dropping on YouTube the same day the episode publishes.The throughline across all three conversations is the same: fandom, trust, and the growing conviction that reaching audiences isn't enough, you have to move them.Key Takeaways:1. Affinity's Five VerticalsBBC Studios has launched Affinity, a fandom-first advertising network built across five verticals: Family (anchored by Bluey), Auto (Top Gear), Travel & Food, Entertainment, and Our World (anchored by BBC Earth, built over 10 years across IP including Blue Planet and Big Cats). Each vertical is built around existing trusted BBC IP, with third-party studio IP (Magic Light Pictures' Zog, Acamar's Bing) layered in to deepen the offering. 2. The BBC Group YouTube ExpansionBBC Studios and BBC Public Service are launching 50+ new YouTube channels in 2025, roughly half through BBC Studios, half through public service. Dan McGolpin describes a strategic shift from treating YouTube as a marketing tool to actively building communities, particularly for under-25s in the UK. The approach mirrors what BBC Studios has learned about channel specificity: rather than one BBC Sport account, they've spun off a dedicated BBC Football channel, with more sport-specific channels to follow. 3. The Internal BBC PartnershipThe first piece of breaking news: BBC Studios' Affinity team will now sell advertising outside the UK for selected public service BBC YouTube channels. This will be the first time the two arms of BBC Group have formally unified their commercial digital strategy. Previously BBC Studios' digital ad operation focused exclusively on BBC Studios content. This expansion means the Affinity network now spans both the commercial and public service sides of the BBC, giving advertisers access to the full depth of the BBC content portfolio on YouTube worldwide.4. The Bluey x LEGO Co-CommissionThe second piece of breaking news: a 10-part content series with LEGO brick recreations of fan-favourite Bluey moments, co-commissioned by BBC Studios and the LEGO Group, dropping on YouTube. Anna Rafferty describes it as an editorial co-commission, not just a product partnership: the series was built around the insight that children love to "play their stories," creating a watch-play-build loop designed to deepen engagement across both the Blueyverse and the LEGO universe simultaneously.5. The Fandom Measurement ModelBBC Studios' core KPI is average watch time. Bluey averages nearly 15 minutes of watch time per session, against a portfolio average of 13.3 minutes, both significantly above industry benchmarks. 77% of BBC Studios' viewing happens on CTV — meaning the majority of Bluey and Top Gear consumption is happening on the living room television, with high co-viewing rates that make it especially valuable to advertisers. Thank you Jasmine Dawson, Dan McGolpin, and Anna Rafferty for joining the pod!Jasmine Dawson - https://www.linkedin.com/in/jasminesdawson/Dan McGolpin - https://www.linkedin.com/in/dan-mcgolpin-093268123/ Anna Rafferty - https://www.linkedin.com/in/annarafferty/ Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8 Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/ Marion Ranchet - https://www.linkedin.com/in/marionranchet/ The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast (00:00) - Cannes Lions Kickoff (02:06) - Fandom First Results (03:24) - New KPIs Hours Watched (04:36) - Beyond Bluey Repeatable Playbook (05:58) - Affinity Network Five Verticals (11:25) - Community Led Bluey Examples (17:01) - BBC YouTube Partnership Expansion (21:20) - 50 New Channels Plan (21:51) - World Cup Banter (22:20) - Verticals and Communities (23:28) - Operating Model Explained (25:07) - US Expansion and Global Ads (26:23) - Lego Guest Joins (28:00) - Bluey Lego Series Premiere (36:44) - Release Strategy and Wrap

Summary

AI SLOP, GATEKEEPERS, AND THE KID'S MEDIA CRISIS

Jun 2500:31:57Summary readyDemand for high-quality kids' content has never been higher, but the supply has never been more broken. And YouTube, the most powerful kids' platform on Earth, is running it like an algorithm, not a network.This live panel episode of the Media Odyssey Podcast, recorded at the Media Universe Summit, features Evan Shapiro and Jamie Shapiro alongside Andy Donner, Head of Partnerships at Common Sense Media, and Sara DeWitt, Senior Vice President & General Manager at PBS Kids. The conversation centers on Evan and Common Sense Media's joint report on the state of the kids' content industry. The picture it paints is stark with millennial and Gen Z parents demanding more high-quality, trusted kids' content than ever, while streaming platforms have cut series orders by 25%, public media is being defunded, and YouTube Kids remains under-monetized and under-curated despite being the most-watched kids' platform in the world. The panel covers co-viewing trends, the collapse of the independent kids' production ecosystem, the rise of AI slop in children's content feeds, and what it would actually take for a major streamer or YouTube to step up and fill the gap.Key Takeaways:1. Supply vs. Demand Demand for quality kids' content has doubled among parents (70% of whom are now millennials or Gen Z) while the number of series orders from streamers has dropped 25% from its 2022 peak. Streamers figured out kids' content reduces churn but doesn't drive new subscribers, and largely stopped commissioning it. Public broadcasters like PBS, BBC, and ABC Australia now produce 54% of kids' content worldwide.2. The YouTube Kids Problem 88% of parents of kids under seven say their children prefer YouTube over any other platform, yet kids' content represents 15% of total YouTube usage and just 2% of its monetization. YouTube Kids has the lowest co-viewing rate of any major platform and AI-generated slop is regularly making it through content filters. The American Academy of Pediatrics warns YouTube is actively harming children's development.3. The Algorithm Gap COPPA enforcement removed an estimated $2 billion from the kids' content marketplace, primarily from YouTube. Streamers that stopped commissioning original kids' content are now inadvertently driving young viewers to YouTube. PBS Kids saw 40% YouTube growth simply by launching content globally and allowing international ads, because global distribution signals demand to the algorithm and lifts domestic reach.4. Co-Viewing Is Back and Underserved Co-viewing has surged since COVID, with the desire to watch content together as a family now ranking as the top thing parents say they don't want to lose from the pandemic period. Research shows kids learn significantly more when a parent or sibling is present. But fragmented subscriptions, too few family-friendly titles, and algorithm-driven autoplay leave a commercial gap for any platform willing to program for the whole family.5. YouTube Needs to Run Kids Like a Network The panel's clearest call to action: YouTube should treat YouTube Kids as a curated network, not an algorithm. That means human curation, better revenue sharing for kids' content creators, global distribution partnerships, and taking its developmental responsibility seriously. YouTube would make more money doing it, and the goodwill from parents and educators would be commercially valuable in its own right.Thank you Andy Donner and Sara DeWitt for joining the pod!Andy Donner - https://www.linkedin.com/in/andydonner/ Sara DeWitt - https://www.linkedin.com/in/saradewitt/Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8 Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/ Marion Ranchet - https://www.linkedin.com/in/marionranchet/ The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast (00:00) - Introduction to Kids' Content Landscape (02:50) - The Supply and Demand Crisis in Kids' Media (09:45) - The Co-Viewing Phenomenon and Its Impact (14:04) - Legacy Brands vs. New Creators in Kids' Content (20:50) - The Role of YouTube and Content Curation (24:01) - Monetization Challenges and Opportunities in Kids' Media

Summary

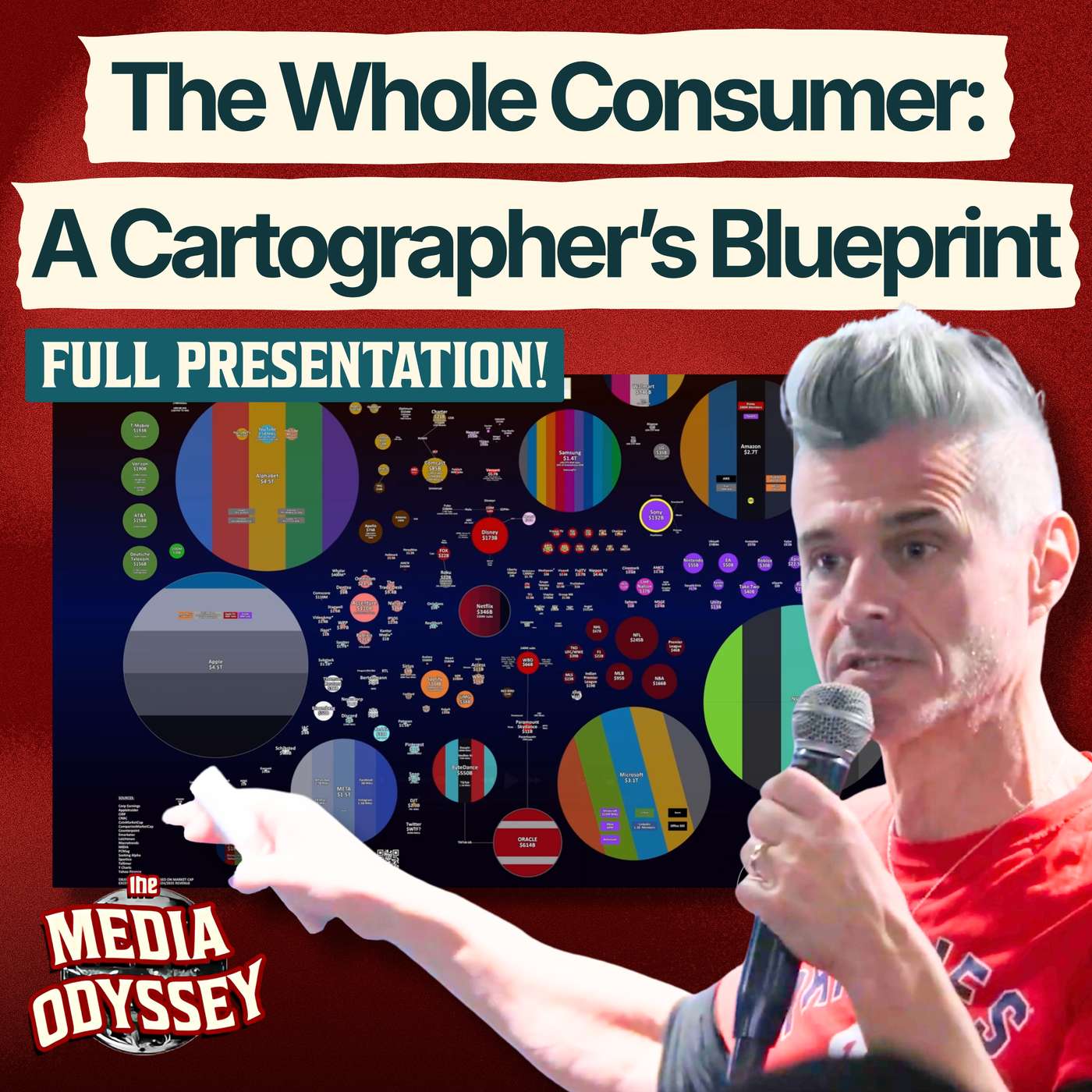

THE WHOLE CONSUMER: A CARTOGRAPHER'S BLUEPRINT

Jun 2200:27:00Summary ready59% of people now watch video on their phone first. If your content strategy doesn't account for that, Evan Shapiro has a message for you: you're already losing.This keynote episode of the Media Odyssey Podcast features Evan Shapiro's live Stream TV Europe presentation. It is a fast, data-driven breakdown of where streaming media, social media, YouTube, and TikTok are headed next. Built on original research from MX8 Labs and Evan's new Cross-Screen Attention Index, the talk argues the media industry is now entirely consumer-driven, and most legacy companies haven't caught up. Through real-world case studies (Duolingo, Kit Kat, PBS, RuPaul's Drag Race, Toonstar) Evan makes the case for what he calls the "affinity economy": brands and creators win by building loyalty and fandom, not chasing scale.Key Takeaways:1. Phone-First Is the Default 59% of consumers age 13+ say their phone is their primary video device — nearly 2x television. For Gen Z, the bathroom ranks third among top video-watching locations.2. YouTube Leads, But Faces PressureYouTube ranks #1 in total attention per Evan's new Cross-Screen Index, but Meta overtakes it when Instagram and Facebook are combined. TikTok ranks #2 among under-55s and is bigger than Netflix, Paramount, NBCU, and Warner Bros. Discovery combined.3. Retention Reveals a Loyalty Gap The average premium streamer has 11% retention, gaining 175 million subscribers last year while losing 156 million. WOW Presents Plus, home to RuPaul's Drag Race has a smaller subscription base, but maintains just 4% churn.4. Fan Engagement Drives Real ROI Coach's UGC campaign drove a 142% rise in company value. Duolingo's mascot stunt drove its first billion-dollar year. PBS's Frontline now averages tens of millions of YouTube views, with donations up 61%. 5. Vertical Video Is a White Space Disney, Netflix, and Paramount are all launching vertical feeds. Evan argues most vertical content is low-quality leaving room for premium creators willing to treat it as real programming, not marketing.Interested in sponsorship? https://forms.gle/2LCWfX2HBNT8mtpx8 Connect with us on Linkedin:Evan Shapiro - https://www.linkedin.com/in/eshap-media-cartographer/ Marion Ranchet - https://www.linkedin.com/in/marionranchet/ The Media Odyssey Podcast - https://www.linkedin.com/company/the-media-odyssey-podcast (00:00) - Scaling Business Without Overhead (03:00) - Understanding the Consumer-Driven Media Landscape (05:45) - The Shift in Video Consumption Trends (08:51) - The Importance of Mobile and Vertical Content (12:03) - Measuring Attention Across Platforms (15:07) - The Rise of the Affinity Economy (18:03) - Empowering Employees as Creators (20:59) - The Future of Content Creation and Distribution

Summary